Wake Up Wall Street (SPX) (QQQ): Rally back on as Bezos blasts off and Netflix to be watched closely

Here is what you need to know on Tuesday, July 20:

Equity markets took another hammering on Monday as fears over the Delta covid strain hit investors hard. While this has been known for some time, it is only recently that the market appears to have decided to use it as an excuse to sell off. As we have often mentioned here at FXStreet, the market finds the narrative to do exactly what it wants and needs to do. The market wanted to sell off and probably needed to sell off as the gains had become too stretched. Now what needs to be seen is whether the fears over Delta can be put to the back of investors' minds just like fears over inflation were a few months ago. This time there is no Fed to ride to the rescue as Delta does not yet meet their mandate. If the market keeps on dropping, maybe the Fed will get in the vaccine game just like it got in the money printing game. A tad sarcastic, but the Fed balance sheet continues to balloon, and the correlation between this ballooning balance sheet and equity markets remains strong.

JPMorgan takes a different tone this morning with a note increasing their year-end S&P 500 target, saying they think fears of a slowdown are overdone. The latest data on Delta does show it spreading rampantly among the unvaccinated, so perhaps a renewed push on vaccinations will help. Either way winter 2021 may yet prove challenging. Europe remains under attack from Delta with many countries increasing restrictions and most EU states trying to ramp up vaccination programs to combat the spread. The UK is the obvious exception as it ended all restrictions on Monday. This will make for an interesting test case so investors should keep a close eye on infection and hospitalization levels in the UK in the coming weeks.

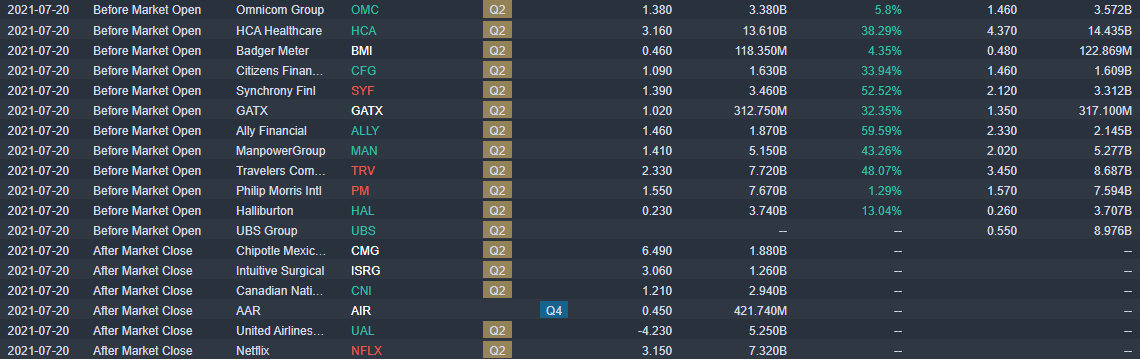

Earnings season continues with NFLX kicking off the tech giants after the close tonight. IBM released some decent numbers, while AMZN sees its former CEO jet off to space later on Tuesday.

Over in the relative calm of currency land, the dollar continues to confound all and continue to strengthen – to 1.1770 now while the even calmer bond market sees yields slump lower. Bitcoin cracks $30,000, but no panic has yet ensued. Watch this space. Oil continues to dump after Monday's OPEC+ announcement, at $66 now.

European markets are slightly higher, FTSE +0.1%, EuroStoxx +0.1% and Dax +0.15%.

US futures are also higher, S&P +0.4%, Nasdaq +0.4% and Dow +0.5%.

Wall Street top news

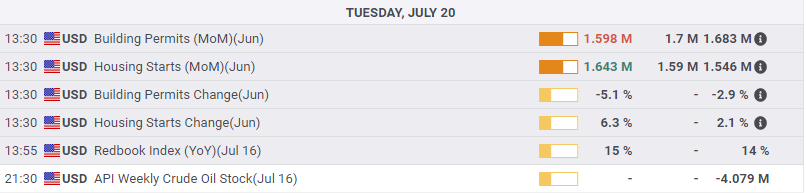

German PPI 8.5% versus 7.2% prior.

US Housing starts rise 6.3% in June versus 1.2% forecast.

US Redbook retail sales rise 15%.

Netflix (NFLX) reports after the close.

United Airlines (UAL) reports after the close.

Healthcare (HCA) up 7% on strong results.

Peloton (PTON) up 5% as the company announced United Healthcare members can access classes.

Rocket Companies (RKT) down 3% as Wedbush downgrades.

UBS up 3% on strong results.

IBM up 3% on strong results after the close on Monday.

Vertex Pharma (VRTX) down 2% as SVB Leerink downgrades.

Haliburton (HAL) up as results beat estimates.

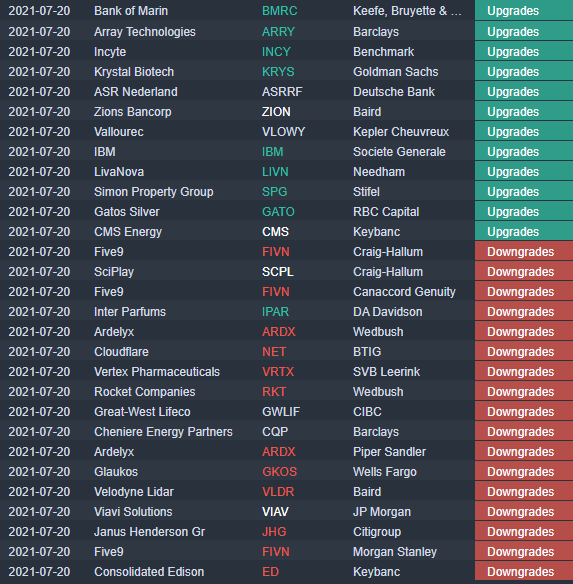

Upgrades, downgrades, earnings and premarket movers

Source: Benzinga Pro

Economic releases

Like this article? Help us with some feedback by answering this survey:

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.