Wake Up Wall Street (SPDR S&P 500 SPY): Dow down, S&P stumbles and Nasdaq knocked

Here is what you need to know on Thursday, September 8:

The equity market fell for three days straight on Wednesday sending fear into the new batch of traders who have grown accustomed to the market being on Fed steroids that never end. September has kicked off with some hesitation after a summer blockbuster for US indices. The start of a month is statistically less impressive than the end of the month, so let us see how September pans out. Investors and mainstream media are citing Delta, stumbling economic growth and inflation as possible problems, but really there is nothing new here over the last few months. Economies are reopening and recovering, but the graph is not linear and some hiccups will be met along the way. Delta is another problem, but vaccines appear to offer the best way out of this and economies look set to avoid further lockdowns.

The taper is another issue worrying investors. Friday's weak employment report had appeared to put tapering off the Fed agenda, and equities rallied accordingly, but now the ECB has stepped into the taper limelight and has just announced a taper of its own! The PEPP program is to continue at a moderately lower rate. The Fed Beige Book on Wednesday was more hawkish than hoped for with rising inflation and moderate growth mentioned, the double threat!

The dollar though has continued to weaken slightly as the ECB appears to be more hawkish still than the Fed. The dollar is back to 1.1840 now versus the euro, Oil is higher as hurricane season hits Gulf production, and Bitcoin remains mired below $50K at $46,300 now. Gold is sitting pretty at $1,798.

European markets are lower: FTSE -0.8%, Dax -0.3% and EuroStoxx flat.

US futures are flat, the S&P 500 is the biggest mover at -0.05%!

Wall Street SPY news

ECB announces taper of PEPP program.

Japan to be removed from EU safe travel list.

Dr. Fauci says infections in the US are ten times too high.

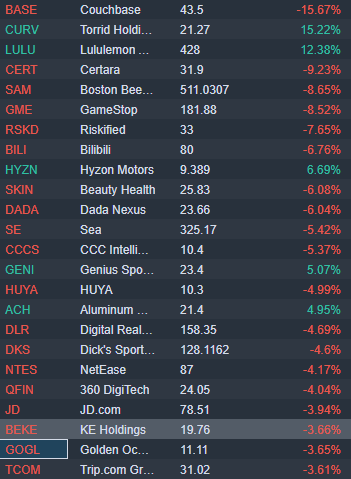

GameStop (GME) falls as EPS misses despite revenue beating estimates. No future details on the conference call or outlook.

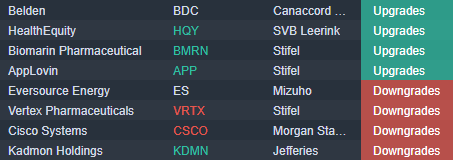

Macy's (M): Cowen & Co upgrades to outperform.

Boston Beer (SAM) falls 9% as it pulls earnings guidance.

Are airline stocks in play? Easyjet (EZJ) says it rejected a takeover offer. DAL, UAL, LUV, AAL JBLU.

United Airlines (UAL): Speaking of airlines, UAL reduces guidance as Delta hits demand.

Lululemon (LULU) surges over 10% on strong earnings.

China is cracking down again as some Chinese tech names in the gaming sector are summoned to meet authorities. Chinese tech names are all getting hit it would seem. BEKE, NTES, BILI, JD, BABA, PDD, TME.

Couchbase (BASE) down heavily in premarket on earnings.

Torrid Holdings (CURV) up 14% on earnings.

Hyzon Motors (HYZN): JP Morgan gives an overweight rating.

Genius Sports (GENI) up 6% on results and partnership with Penn Interactive.

Dada Nexus (DADA) Keybanc lowers price target after results on Wednesday, shares down 6% premarket.

Academy Sports and Outdoors (ASO) beats on revenue and EPS.

AMC announced $25 million advertising campaign with Nicole Kidman. Also CEO teases some form of tie-up with GME.

Lucid Motors (LCID): Citi starts with a Buy rating and $28 price target.

Cicso (CSCO) downgraded by Morgan Stanley.

Upgrades, downgrades and premarket movers

Source: Benzinga Pro

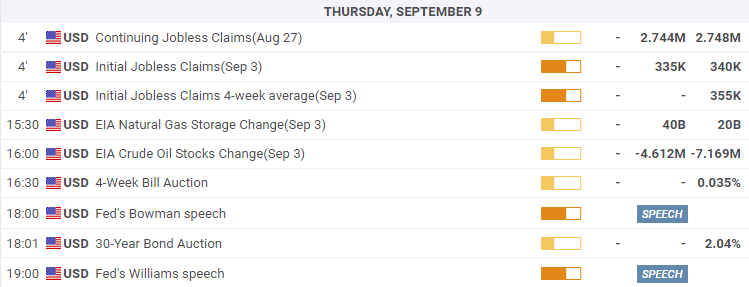

Economic releases

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.