USD Index starts the week on the defensive below 113.00

- The index kickstart the new trading week in an offered tone.

- US yields fade part of the recent rebound on Monday.

- The NY Empire State Manufacturing Index, short-term auctions are due later.

The greenback, in terms of the USD Index (DXY), gives away part of the optimism seen at the end of last week and slips back below the 113.00 neighbourhood on Monday.

USD Index looks to yields, risk trends

The index comes under some moderate downside pressure and probes the sub-113.00 zone at the beginning of the week in a context favourable to the risk complex, while declining yields also accompany the downtick in the buck.

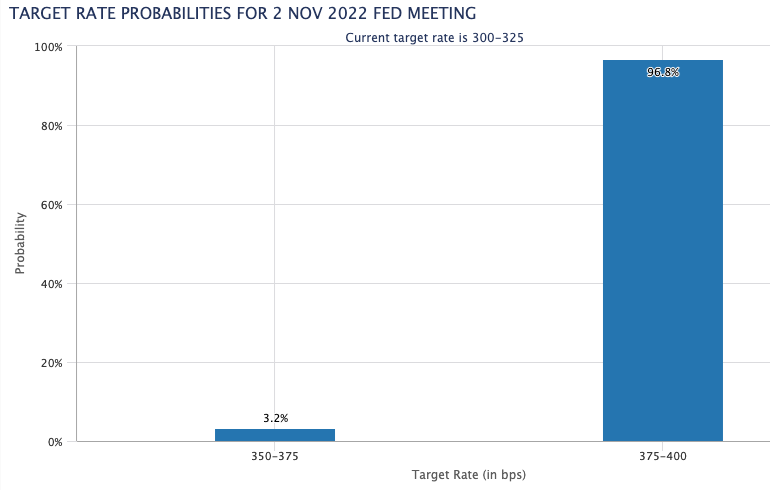

Indeed, investors’ bias towards the riskier assets puts the dollar to the test and triggers the corrective move in the index against an unchanged macro scenario, where expectations of a 75 bps rate hike from the Fed at the November 2 meeting remain well anchored.

On the latter, CME Group’s FedWatch Tool sees the probability of a ¾ point raise at almost 97%.

In the US data space, the NY Empire State Manufacturing gauge and the Monthly Budget Statement will be in the limelight later in the NA session seconded by short-term bill auctions.

What to look for around USD

The dollar surrenders part of Friday’s advance amidst the resurgence of the appetite for the risk-linked galaxy at the beginning of a new trading week.

In the meantime, the firmer conviction of the Federal Reserve to keep hiking rates until inflation looks well under control regardless of a likely slowdown in the economic activity and some loss of momentum in the labour market continues to prop up the underlying positive tone in the index.

Looking at the more macro scenario, the greenback also appears bolstered by the Fed’s divergence vs. most of its G10 peers in combination with bouts of geopolitical effervescence and occasional re-emergence of risk aversion.

Key events in the US this week: NY Empire State Index, Monthly Budget Statement (Monday) – Industrial Production, NAHB Housing Market Index, TIC Flows (Tuesday) – MBA Mortgage Applications, Building Permits, Housing Starts, Fed Beige Book (Wednesday) – Initial Jobless Claims, Philly Fed Index, Existing Home Sales, CB Leading Index (Thursday).

Eminent issues on the back boiler: Hard/soft/softish? landing of the US economy. Prospects for further rate hikes by the Federal Reserve vs. speculation of a recession in the next months. Geopolitical effervescence vs. Russia and China. US-China persistent trade conflict.

USD Index relevant levels

Now, the index is retreating 0.29% at 112.97 and the breakdown of 110.05 (weekly low October 4) would open the door to 109.35 (weekly low September 20) and finally 107.68 (monthly low September 13). On the upside, the immediate hurdle comes at 113.88 (monthly high October 13) followed by 114.76 (2022 high September 28) and then 115.32 (May 2002 high).

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.