Qualcomm (QCOM Stock) Q4 earnings preview

American technology giant Qualcomm, a multinational that creates semiconductors and telecommunications equipment, software, and wireless technology services for customers worldwide, is expected to report its earnings and revenue for its fourth quarter and fiscal 2021 results on Wednesday, November 3, 2021, after market close.

All through the year, Qualcomm has had a stellar performance, beating its earnings estimate every single quarter with the last 2 quarters’ estimate beat topping 14%, a similar story since the start of 2018. This performance is expected to continue especially after a busy quarter where Qualcomm announced the launch of the world’s first drone platform and reference design to offer 5G and AI capabilities, entered an agreement with GlobalFoundries to manufacture an advanced 5G multi-gigabit speed RF front end product to meet the increasing demand and its new partnership with Google and Renault Group to create an immersive in-vehicle experience for Renault new Megane E-Tech Electric vehicle.

The $150 billion in market cap Company submitted a bid to acquire Veoneer Inc. which will strengthen its stance in the emerging markets of driver assistance technology which puts an even brighter outlook ahead for the company whose estimated Earnings per share for the full year is expected to come in at $8.25 which is a massive 96.90% growth y/y and tops all yearly earnings since 2015 – by quite a margin as well. Revenue for the full year is expected at $33.04 billion, up from $23.53 billion y/y (40.40%), with the revenue outlook even better for next year.

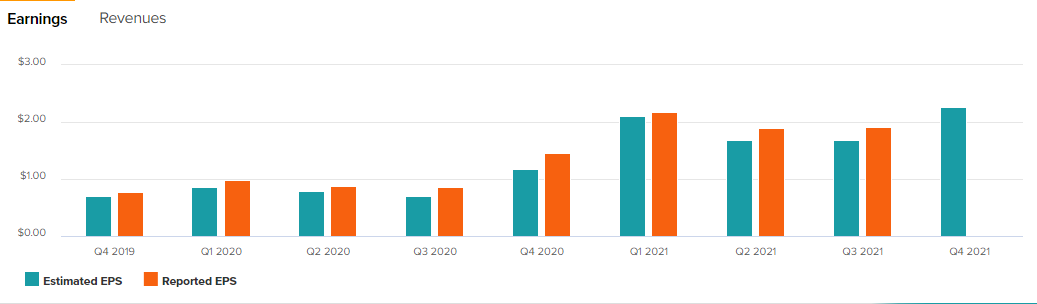

Qualcomm’s EPS History and Forecast

Zack’s Q4 consensus EPS estimate sits at $2.26, up 55.86% y/y from $1.45, and more importantly, beats the previous quarter earnings that printed at $1.92/share. Zacks’ most accurate estimates are a notch higher at $2.27 which shows upward revisions in recent earnings estimates by analysts (the idea is that more recent information could be more accurate and can be a better predictor) as the stock holds a positive ESP of 0.35%. The revenue estimate for the quarter sits at $8.88 billion, up 6.36% from 8.35 billion in the same quarter last year earning it a #3 (Hold) Zacks’ rating.

Considering that Qualcomm has a history of beating estimates and the positive developments from the company in recent months, one can argue that another beat may be on the cards once again. While the consensus estimates are an important gauge of the company’s earnings picture, how much it deviates from the actual number could have an immediate impact on the share price either positively or negatively but the subsequent comments from the company’s management will determine the sustainability of such moves.

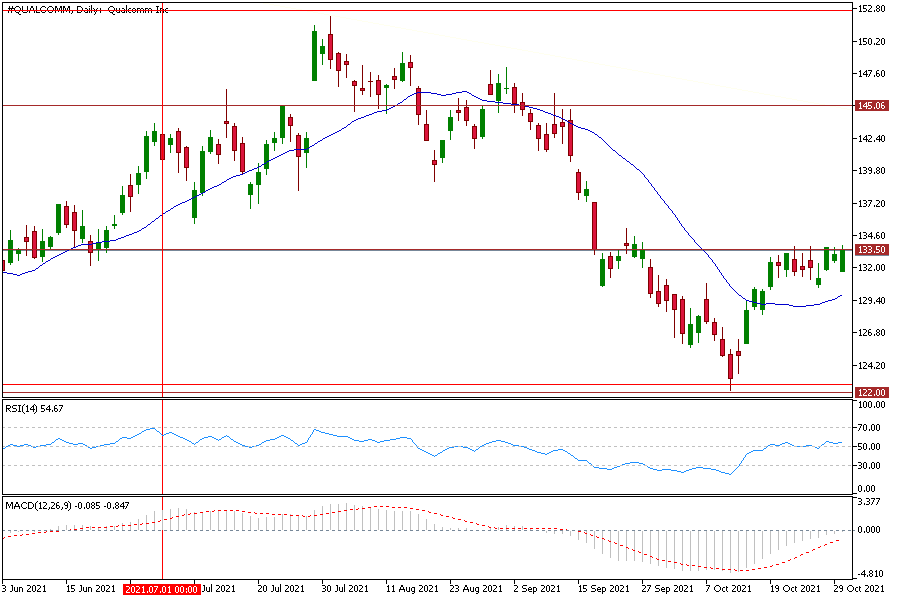

Qualcomm’s share price has maintained a lower trend for most of 2021 but when compared to the upside from early 2020, it is more of a pullback rather than a downtrend. After topping $168.00 in late January, #Qualcomm has fallen about 27% till it found support at $122.00 which was held all through the year, testing in March, May, and October. Currently, it has been struggling at $133.50 for about 2 weeks now as the price needs a major catalyst to break through that level – and what better than a beat in earnings as well as revenue, coupled with solid and positive forward guidance by the Company.

#QUALCOMM, Daily

The MACD is stuck at the midway line although from negative territory is showing a more neutral stance at the moment, in line with the struggle around $133.5, the RSI remains above 50 which puts a more recent positive trend on the table. If we get a beat in revenue and earnings and finally clear out the $133.5 level, the next resistance zone comes in around $139.00 while a miss could see us revisit this year’s low. One key thing to note is that despite the solid earnings we have had in the previous quarters this year, #Qualcomm has not been able to maintain a consistent uptrend and has instead traded sideways for most of the year. So focus will be more on the subsequent comments from the company for sustainability in the moves rather than just on the headline numbers.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.