Markets on the edge: Why recession warnings signal a major stock market correction ahead

Nasdaq 100, S&P 500, Dow Jones, and tech giants face critical support levels

Concerns about an imminent US recession are casting a shadow over Wall Street, driving the Nasdaq 100 (NDX), S&P 500 (SPX), and Dow Jones Industrial Average (DJI) toward critical support levels. Following four consecutive weeks of losses, investors face heightened uncertainty amid escalating trade tensions, rising inflation forecasts, declining consumer confidence, and weakening leading economic indicators.

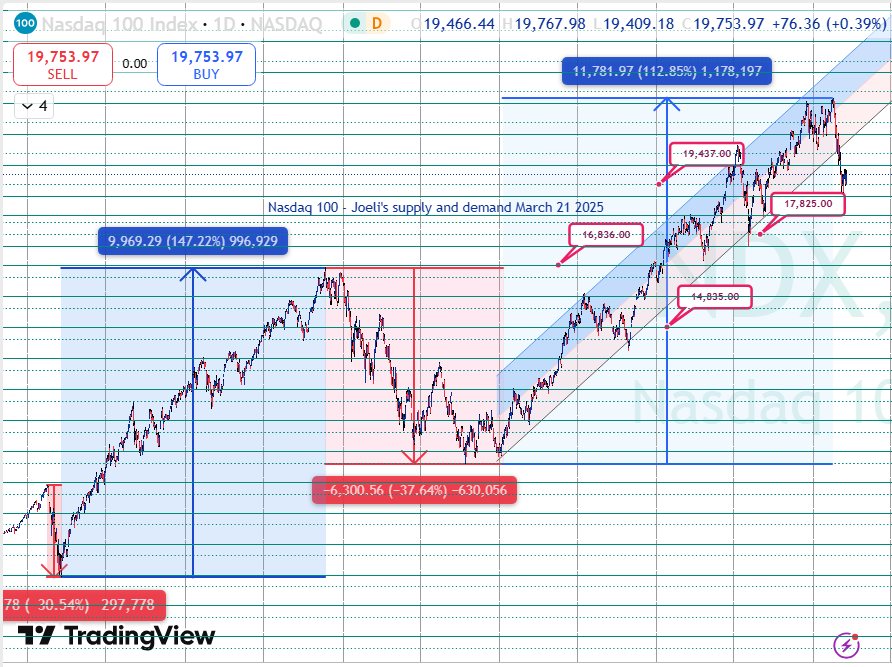

Nasdaq 100: First stage of a major correction

The Nasdaq 100 has plummeted over 11% from its record high of 22,222. With prices now testing key support at 19,437, the index closed slightly higher at 19,753 (+0.39%) on Friday. However, weakness remains evident, indicating the first stage of a potential major correction. Historically, corrections unfold in four stages as part of a healthy market reset.

If support at 19,437 holds, a short-lived rebound could target 19,932, 20,054, 20,433, 20,744, and potentially 21,050. Failure to maintain this level could trigger stage two, aiming for 17,825. Historical patterns suggest a possible four-stage correction of around 33%, targeting approximately 14,835. Technical indicators like RSI and MACD further underscore the bearish momentum.

S&P 500: Bull run reversal underway

The S&P 500 edged higher by just 0.08% to close at 5,667 after a four-week decline. It is now down over 7% from February's peak of 6,147. The index has broken its bullish daily structure, signalling the start of a major correction. Critical support at 5,542 must hold to avoid further downside.

If support holds, a temporary rebound could reach targets of 5,662, 5,737, 5,858, and 5,932. Failure to maintain 5,542 would lead to the second stage, targeting 5,151. Given current economic pressures, a four-stage correction resembling past corrections is plausible, potentially reaching as low as 4,564. Technical analysis indicates weakening momentum, as indicated by bearish crossovers in MACD and declining RSI.

Dow Jones: Double-top signals heightened vulnerability

The Dow Jones closed marginally higher at 41,985 (+0.08%) but remains precariously positioned above critical support at 41,330. A double-top formation at recent highs signals increased vulnerability. If the index breaches this support, it could trigger a deeper correction, targeting 39,062, 36,794, and ultimately 34,526, representing over a 23% decline. Additionally, decreasing trading volumes suggest fading bullish sentiment and increased caution among investors.

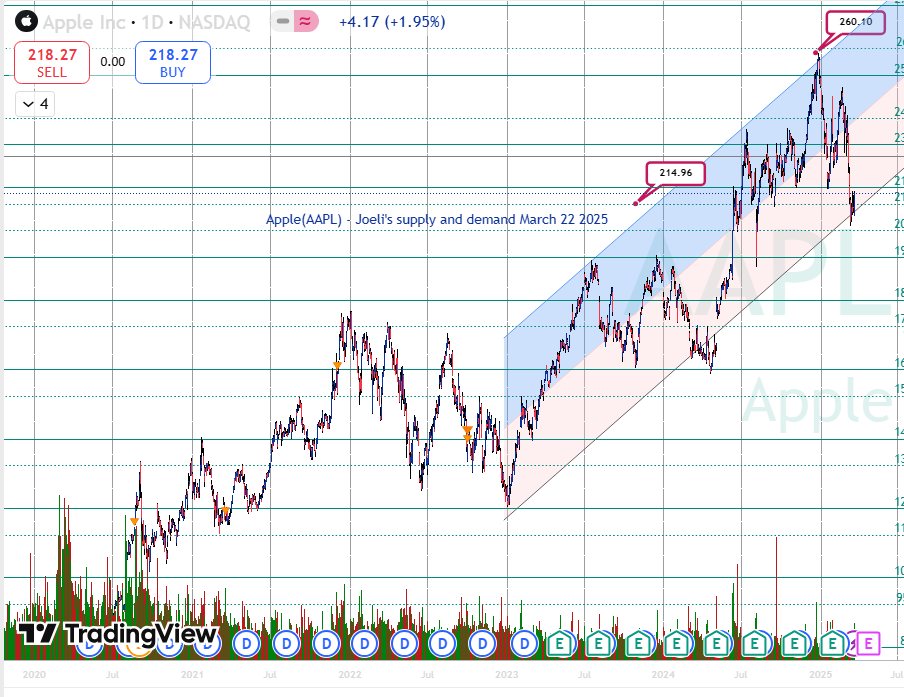

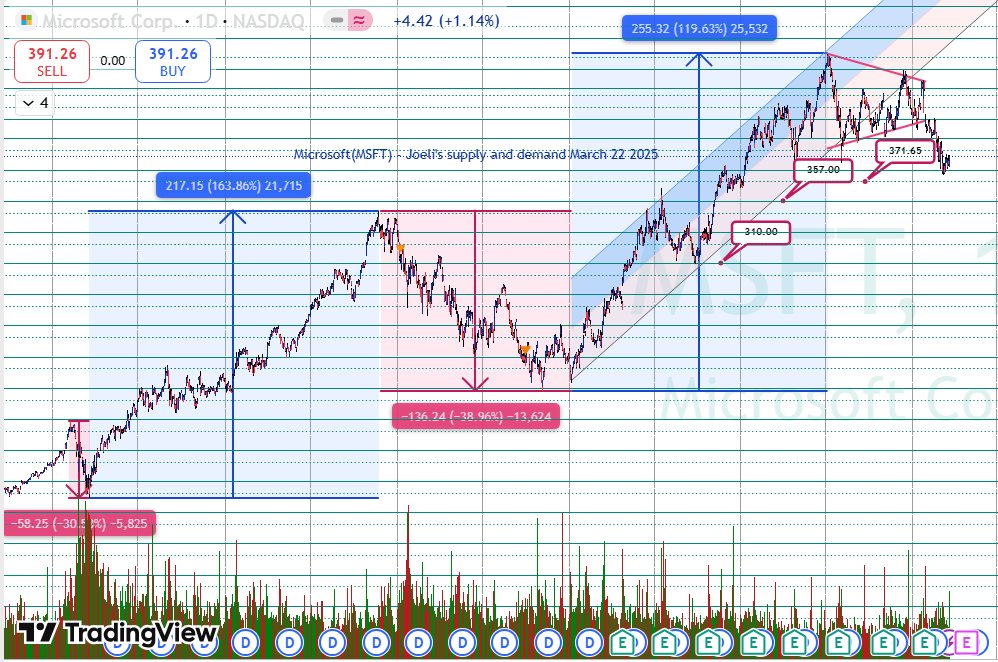

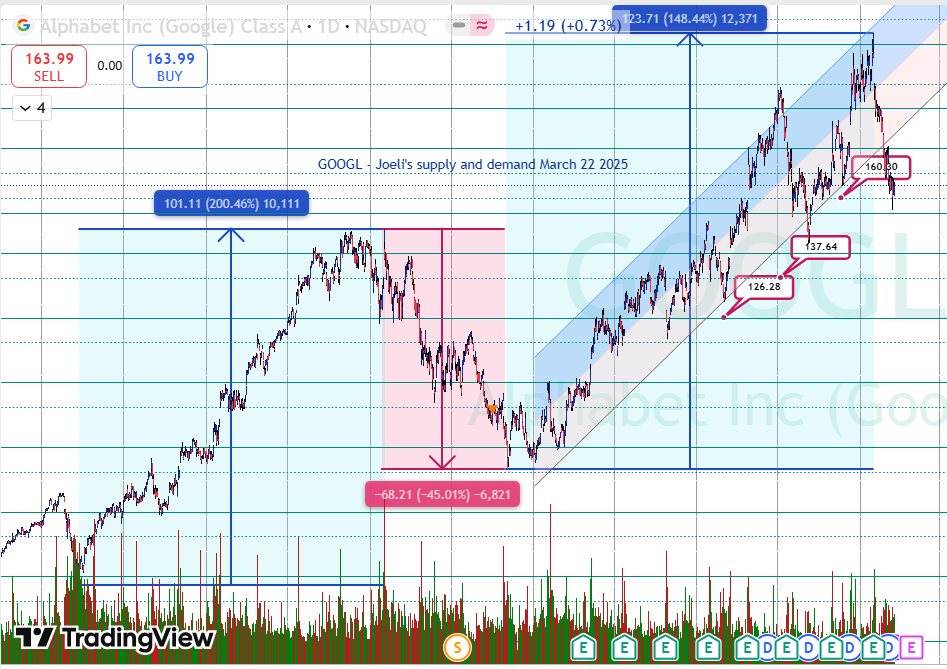

Heavyweight stocks in spotlight: Apple, Microsoft, Alphabet

Apple (AAPL) has fallen 16% from its all-time high (260.10), testing critical monthly support at 232.50 and 219.86. With a Friday close above 214.96, temporary rebounds to 219.86, 224.40, 229.35, and 232.50 are possible. However, a broader market pullback could lower Apple's price to 207, 200, 186, or even 178. Weakness in iPhone sales forecasts and supply chain disruptions could amplify downside pressure.

Microsoft (MSFT) faces a challenging outlook after a 16% drop from its July 2024 peak. The long-term bullish structure has broken, with critical support at 380.65 providing temporary relief. Short-term recovery targets include 395.20, 404.40, 418.70, and 427.70. A major market pullback could drive shares toward 357-348, 333.50-324.50, or even 310.00-300.00, mirroring historical declines of approximately 35%. Ongoing concerns regarding cloud revenue growth and the broader tech slowdown further challenge its recovery prospects.

Alphabet Inc. (GOOGL) has declined by 21% since peaking at 207.05. With its long-term bullish structure compromised, Alphabet could repeat its previous 45% correction. Although closing at 163.99, slightly above the critical 156-160 support zone, any rebound might be capped at 167.35, 174.00, 185.58, and 192.70. A break below support could see shares falling toward 144-137 or even 126-119, marking a 42% correction. Regulatory pressures and declining ad revenue due to economic slowdown could exacerbate declines.

Fundamental factors amplifying risks

Key economic indicators reinforce recession concerns:

- Trade tensions: Renewed tariffs under the current administration amplify economic uncertainty, disrupting supply chains and negatively affecting corporate earnings.

- Inflation concerns: OECD revised its 2025 US inflation forecast higher to 2.8%, signalling sustained upward pressure on consumer prices, which could curb spending and economic growth.

- Weakening consumer confidence: The University of Michigan Consumer Sentiment Index dropped significantly in March, indicating consumers' heightened fears about future economic stability, employment, and inflation.

- Leading economic indicators: Conference Board's LEI posted substantial declines in consecutive months, highlighting slowing industrial production, weakening retail sales, and declining new home sales, all signalling recession risks.

- Interest rate environment: Persistently high interest rates, driven by Federal Reserve policies aimed at combating inflation, continue to pressure businesses and consumers alike, potentially limiting corporate investments and household spending.

- Global economic slowdown: Economic slowdowns in major economies, including China and Europe, add external pressure to US exports, further deteriorating trade balances and GDP growth projections.

Investment implications

Investors should remain cautious. Although buying dips could present short-term opportunities, upside potential appears limited due to prevailing market weakness and economic uncertainties. Historical trends suggest that prudence and diversification will be crucial during this volatile period.

Author

Denis Joeli Fatiaki

Independent Analyst

Denis Joeli Fatiaki possesses over a decade of extensive experience as a multi-asset trader and Market Strategist.