HSBC vs Barclays: Which global bank is better positioned for 2026?

Key takeaways

- HSBC aims $1.5B in savings by 2026 as it exits non-core markets and pivots toward Asia and the Middle East.

- Barclays divested Entercard and German units as part of its core business simplification.

- HSBC's earnings are seen rising 3.3% in 2026, while BCS reflects 21.3% growth, with solid recent stock gains.

HSBC Holdings PLC (HSBC - Free Report) and Barclays PLC (BCS - Free Report) are two global banks based in London that have been restructuring their businesses to improve operating efficiency and focus on core operations.

Both made bold strategic bets this year, whether it's HSBC's Asia-first realignment or Barclays’ emphasis on capital markets and credit growth. As investors plan for 2026 and beyond, the key question is: which of these financial titans offers the stronger growth story? For this, let us evaluate the underlying factors driving each bank’s performance.

The case for HSBC

HSBC has continuously been taking steps to streamline and refocus its global operations. In early 2025, it announced a $1.5-billion cost-saving plan from the organizational simplification efforts (to be achieved by 2026). HSBC is expected to incur $1.8 billion in total severance and other upfront charges by the end of next year to implement these efforts. Also, it announced plans to redeploy an additional $1.5 billion from the strategic reallocation of costs from non-strategic or low-returning activities into its core strategy.

In sync with this, HSBC is winding down several non-core operations in the U.K., Europe and the United States, while maintaining a more focused presence in Asia and the Middle East. It is progressing with divestments in Sri Lanka, Uruguay, Germany, South Africa, Bahrain and France. Apart from these, HSBC completed the sale of its businesses in the United States, Canada, New Zealand, Greece, Russia, Argentina and Armenia, as well as the retail banking operations in France and Mauritius.

As part of its Asia pivot, HSBC has proposed privatizing its Hong Kong unit, Hang Seng Bank, and has expanded wealth operations in China through acquisitions, digital upgrades and lifestyle centers. Additionally, it has accelerated growth in India, securing approval to open 20 new branches. The bank has also strengthened its Indian franchise by launching Global Private Banking, acquiring L&T Investment Management, and expanding Premier Banking to tap the country’s growing wealthy population.

However, HSBC’s revenue generation has been subdued over the past several quarters. While the interest rate environment across the world improved, the financial impact of the challenging macroeconomic backdrop continues to weigh on the company’s top-line growth. Not-so-impressive loan demand and a tough macroeconomic environment in many of its markets remain major headwinds.

The case for Barclays

Barclays has also been striving to simplify operations and focus on core businesses. Aligning with this strategy, in October 2025, the company announced a deal to acquire Best Egg, a leading U.S. digital personal loan platform, for $800 million. This will strengthen the bank’s U.S. consumer finance capabilities and broaden its unsecured lending portfolio. Likewise, in April, it announced a collaboration with Brookfield to transform its payment acceptance business, while last year, the company acquired Tesco’s retail banking business.

Additionally, in August 2025, BCS agreed to sell its stake in Entercard Group to partner Swedbank AB for $273 million, while in February, it divested its Germany-based consumer finance business. Driven by these initiatives, the company’s profitability is expected to improve over time.

Barclays’ structural cost actions have resulted in gross savings of £1 billion in 2024. Moreover, the company achieved its gross efficiency savings target of £0.5 billion for 2025, one quarter earlier than targeted. By the end of next year, management anticipates total gross efficiency savings of £2 billion and the cost-to-income ratio in the high 50s.

However, Barclays’ core operating performance remains unsatisfactory. Its net interest income and net fee, commission and other income have been witnessing a volatile trend over the last several quarters owing to a challenging operating backdrop. Although these metrics rose in 2024 and the first nine months of 2025 on the back of structural hedges and Tesco Bank buyout, the uncertainty about the performance of the capital markets may weigh on the company’s top line.

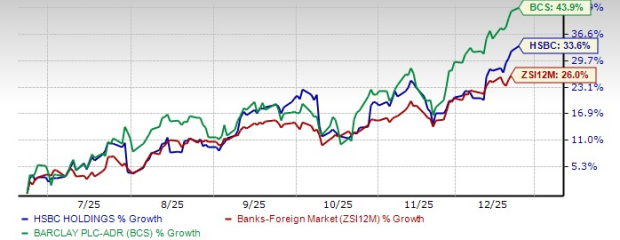

HSBC and Barclays: Price performance and valuation analysis

Over the past six months, Barclays’ shares have performed quite well on the NYSE compared with HSBC. BCS stock has jumped 43.9%, while HSBC gained 33.6%. The industry has rallied 26% in the same time frame.

Six-month price performance

Image Source: Zacks Investment Research

Valuation-wise, HSBC is currently trading at a 12-month trailing price/tangible book (P/TB) of 1.37X. BCS, conversely, has a P/TB TTM of 0.96X currently. Thus, Barclays is relatively inexpensive compared with HSBC.

P/TB TTM

Image Source: Zacks Investment Research

How Do Earnings Estimates Compare for HSBC & BCS?

The Zacks Consensus Estimate for HSBC’s 2025 earnings suggests a year-over-year increase of 14.9%, while the same for 2026 indicates a 3.3% rise. Over the past 60 days, earnings estimates for 2025 and 2026 have been revised upward.

Earnings trend

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for BCS’ 2025 and 2026 earnings indicates 23.9% and 21.3% growth, respectively. Over the past 60 days, earnings estimates for 2025 have moved marginally north while estimates for 2026 have been revised lower.

Earnings trend

Image Source: Zacks Investment Research

HSBC or BCS: Which stock will offer more upside in 2026?

While both HSBC and Barclays have taken meaningful steps to streamline operations and drive growth, HSBC’s focused pivot toward high-growth Asian markets, aggressive cost optimization and strategic redeployment of capital position it more favorably for long-term gains. Despite near-term revenue pressures, its structural transformation appears more comprehensive and future-ready.

On the other hand, Barclays’ earnings outlook is stronger on paper, but its exposure to volatile capital markets and inconsistent core income performance raise concerns. For investors seeking a more stable, strategically aligned global banking play heading into 2026, HSBC emerges as the better-positioned stock.

Want the latest recommendations from Zacks Investment Research? Download 7 Best Stocks for the Next 30 Days. Click to get this free report

Author

Zacks

Zacks Investment Research

Zacks Investment Research provides unbiased investment research and tools to help individuals and institutional investors make confident investing decisions.