Equities report: Mixed signals from US equities

Major US stock market indexes seem to send some mixed signals as the Dow Jones, maintains a clearer upward movement, Nasdaq has substantial difficulty forming a higher peak, as does S&P 500. Today we are to have a more fundamental approach by looking at the intentions of US president-elect Donald Trump and the Fed, while have a closer look at Apple’s challenges. For a rounder view we are to conclude the report with a technical analysis of S&P 500’s daily chart.

Trump’s Treasury pick and tariffs on imports

Trump’s pick for the Treasury Secretary, Scott Bessent, 62, hedge fund manager, may have been the main headline over Trump’s picks in his new Government, in the past week. The nominee seems to be a more mainstream choice, less controversial and Wall Street likes him. He is considered a good ally in Trump’s ideas for further deregulation of the markets and easing corporate taxation, yet it’s also going to be interesting to see his potential influence in Trump’s intentions to slap tariffs on US imports. We note that Bessent was reported to be a supporter of a stronger USD, thus in turn may prove to be also a supporter for tariffs on US imports. Overall we see the case for the pick of Bessent to ease the market’s worries for Trump’s economic policies, thus creating some support for US stock markets on a fundamental level. On the other hand, the announcement by Trump that on the first day in office we will be applying 25% tariffs on imports from Mexico and Canada and charging also additional 10% tariffs on imports from China could renew market worries and thus could weigh on US stock markets as the tariffs could enhance uncertainty.

The Fed’s intentions and financial data due out

On a monetary level, the release of the Fed’s November meeting minutes yesterday, tends to highlight the bank’s cautious approach towards cutting rates further. On the one hand the bank’s policymakers seemed to agree that inflation is easing sustainably towards the bank’s 2% target, yet at the same time also noted that growth remains solid and the US employment market conditions have eased, while there may be also increased uncertainty about the path of the US economy. Overall, we see the case for the document to weigh on US equities, as there is no certainty for extensive further rate cuts to come, but a “gradual” approach. Today in the early American session we note from the US the release of the durable goods orders growth rate for October which is to provide a glimpse at how much confidence US businesses have in actually investing in the US economy, yet the release may be eclipsed by the simultaneous release of the revised GDP rate for Q3. Should the rate verify the growth reported by the preliminary release or even accelerate we may see support for US equities, while a possible slowdown of the rate could weigh. Later on, we get from the US the release of the Fed’s favourite inflation metric for October, namely the PCE rates. The release may be characterised as the last big test for US stock markets before the release of the US employment report for November next week. Should the rates accelerate, or even fail to slow down, implying a persistence of inflationary pressures in the US economy, we may see the release weighing on US equities as the Fed’s hesitation to ease further financial conditions in the US economy, may enhance.

Worries for Apple

Apple’s (#AAPL) share price has been on the rise since the start of the week, yet the company is challenged at various fields. On the ground of the retail field, we note the beginning of a Christmas sales period, starting with Black Friday and Cyber Monday. The market may have high expectations for the company’s retail sales department as the company’s revenue figure is rebounding in Q3, after bottoming out in Q2. The holiday season, is an excellent opportunity for the company to enhance the rebound of the revenue figure and is expected to play a crucial part. Apple's upcoming iOS 18.2 release, which is set to occur in December, may prove to be a critical issue for the substitution of existing iPhone models in next years’ circle. It should be noted that the company may still be struggling to rebound on sales in China a key sector for Apple, as the company is facing stiff competition from local producers such as Huawei. Furthermore, Apple seems to have difficulties in China, in launching its AI models for iPhones as a foreign country. Should also President elect Trump impose additional tariffs on US imports from China, the company’s difficulties could heighten. Tim Cook, Apple’s head, is currently visiting China, yet any substantial positive results are doubtfull. Overall despite a rebound being in motion for the company we still maintain low expectations and necessitate more concrete results.

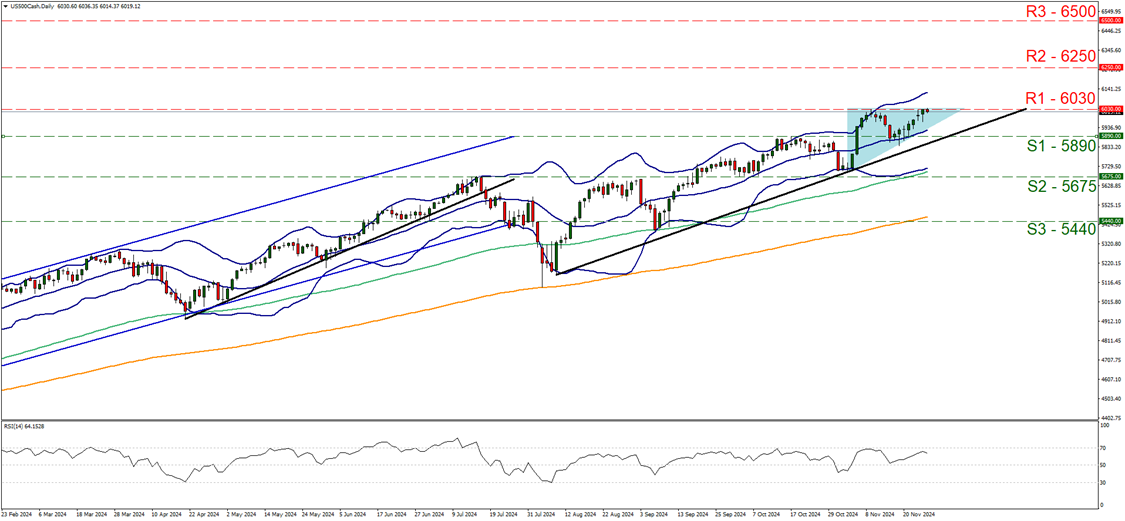

Technical Analysis

US500 daily chart

-

Support: 5890 (S1), 5675 (S2), 5440 (S3).

-

Resistance: 6030 (R1), 6250 (R2), 6500 (R3).

For US equities we note a slight rise with US 500 testing record high levels at the 6030 (R1) resistance line. We maintain our bullish outlook as long as the upward trendline remains intact and given that the RSI indicator is currently near the reading of 70 implying a bullish market sentiment. We also note that the index’s price action finds some difficulty to form a higher high with the 6030 (R1) resistance line at this point acting as a ceiling and should the index fail to break it correcting lower it may start forming a double top formation with the S1 being possibly a neckline. Yet the upward triangle being formed for the time being, by the price action seems to be underscoring the upward motion. Should the bulls maintain control over the index, we may see its price action entering unchartered waters by breaking the R1 and set as the next possible target for the bulls the 6250 (R2) resistance level. For a bearish outlook we would require the index to reverse course by breaking the prementioned upward trendline signalling the end of the upward movement and continue lower by breaking the 5890 (S1) support line and taking aim of the 5675 (S2) level, which was tested as both a resistance and support line. Even lower we note the 5440 (S3) support barrier which has not seen any price action since the 11th of September.

Author

Peter Iosif, ACA, MBA

IronFX

Mr. Iosif joined IronFX in 2017 as part of the sales force. His high level of competence and expertise enabled him to climb up the company ladder quickly and move to the IronFX Strategy team as a Research Analyst. Mr.