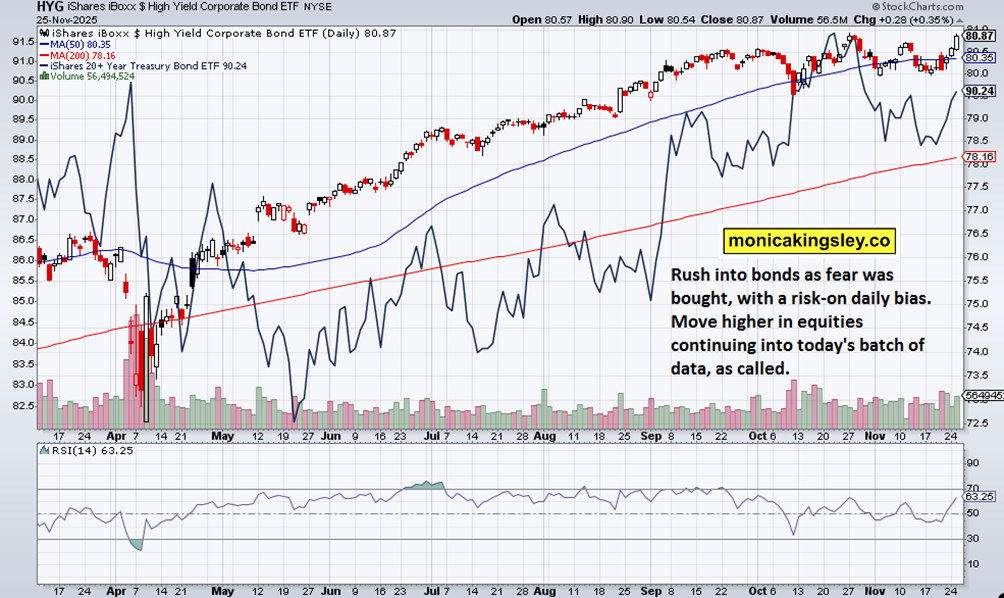

Credible turn not to miss

S&P 500 duly tanked on poor incoming data showing consumer under (spending) stress, and overal not tame PPI inflation – for two hours. Rate cut odds also improved in the end, and what was most important development through the day, was one of not short squeeze characteristic – tech gradually recovered from its panicky selloff leadership, breadth broadened, and consumer discretionaries didn‘t do too badly either.

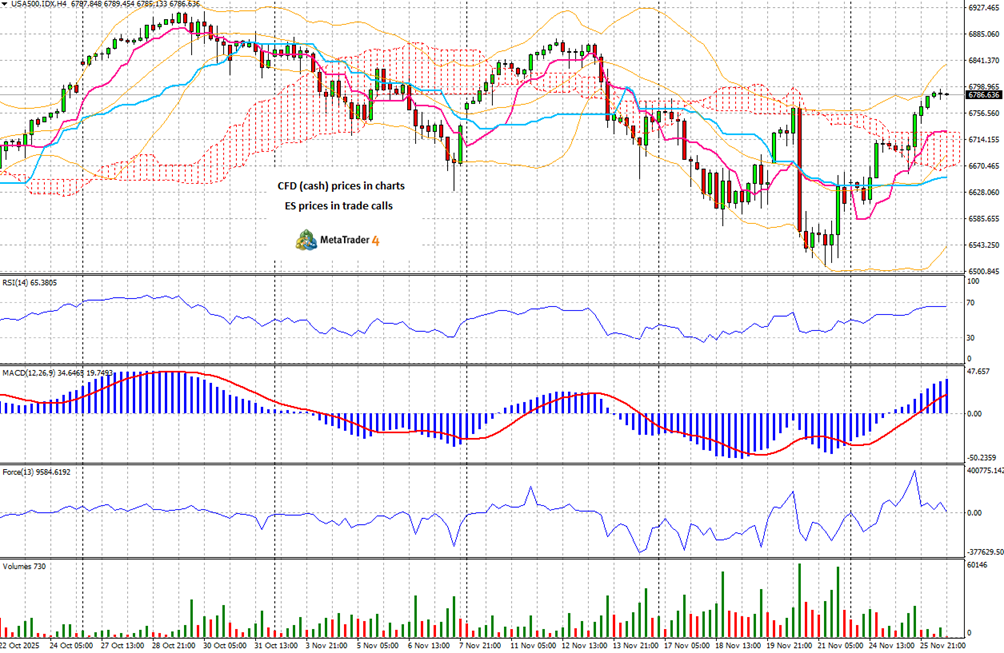

So, we have stocks rising for three days in a row amid other breadth/volatility/bond market and macroeconomic signs – with ES 6,730 – 6,760 (volume profile) resistance being overcome to the upside – and as soon as it was about to become the case, breadth and sectoral characterisrics allowed for increased position sizing on the long side.

Today‘s job market and housing data will provide further rate cutting clues – and the market likes them as much as it did the chatter about who would be the new Fed Chair yesterday.

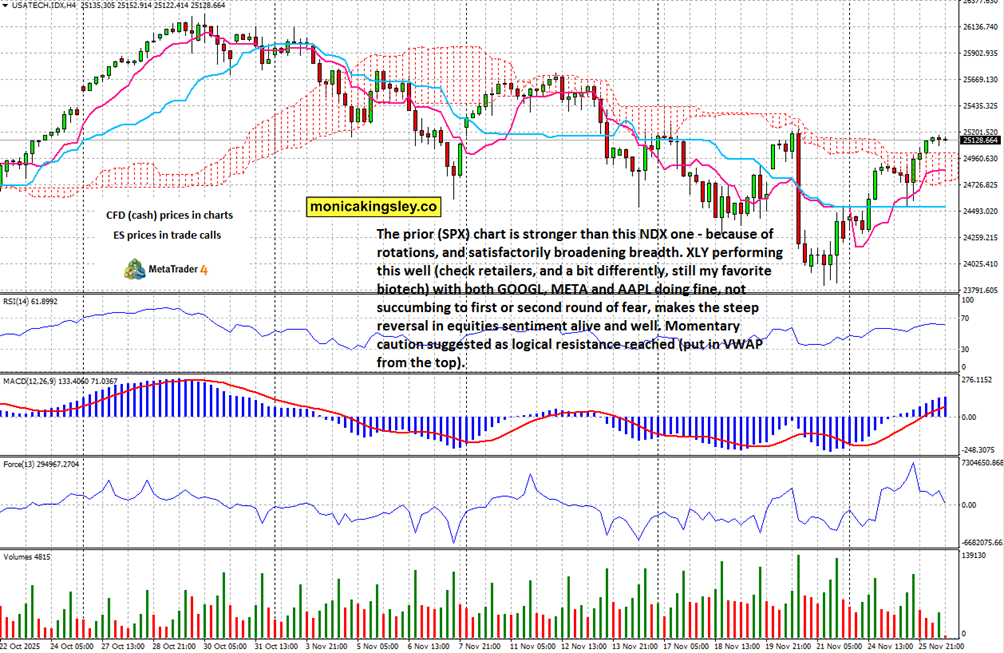

S&P 500 and Nasdaq

Below, you‘ll find premium stock market analysis that Trading Signals (Stock Signals) clients are getting every day – if you join still this month, you‘ll have premium access till the end of the year! Nasdaq isn‘t on the verge of outperforming S&P 500, but that could change next week. For now, those rotations make ES the stronger index, and I favor shaking off today‘s set of data that would provide less of a white knuckle ride than yesterday – bonds on the short end have little doubt about surging in anticipation of rate cuts, which is what would power equities higher – I‘ll comment in your premium equities channel as necessary, first I see trepidation and uncertainty in giving up some premarket gains. AMD took a great beating yesterday as called, and wouldn‘t get too much better today.

Author

Monica Kingsley

Monicakingsley

Monica Kingsley is a trader and financial analyst serving countless investors and traders since Feb 2020.