Amazon Q4 earnings: A negative close to 2022

Amazon.com will publish its quarterly earnings on a relatively busy day of tech releases on Wednesday after the market close along with Apple, Alphabet, and Meta. Analysts expect a downbeat finish to 2022, though they believe that the stagnation will be temporary, and the giant e-commerce retailer will become a profit-making company again this year". The consensus recommendation from Refinitiv analysts is “buy”.

2022 headwinds

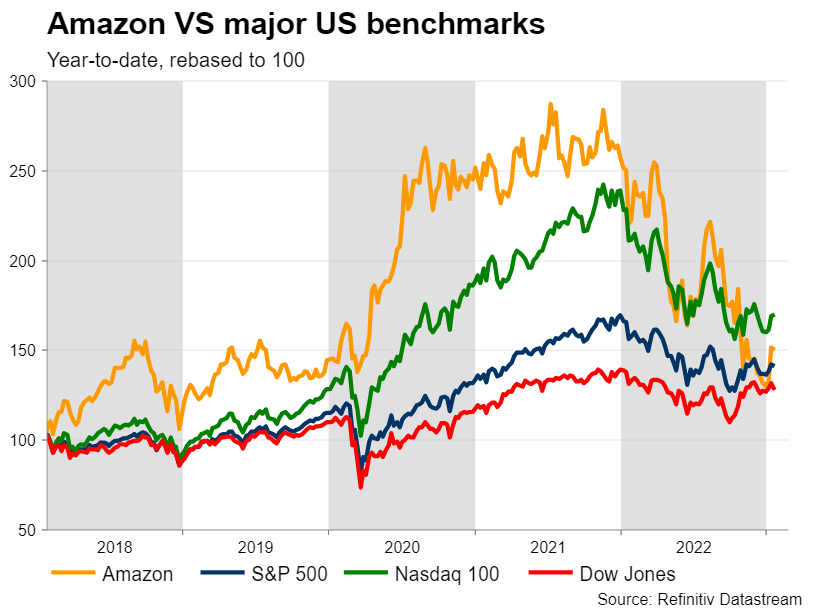

The world’s largest e-retailer by market capitalization saw its pandemic stock rally dwindling over the past year, ending 2022 sharply down by 55% from the all-time high of $187.97 registered in November 2021. While the company emerged as one of the biggest winners of the covid-19 pandemic period, thanks to its unique online nature and its rich capacity which overcame supply chain jitters and served millions of clients remotely, the company could barely find fresh tailwinds during the post-lockdown period.

Digital demand cooled down as consumers spent more time outside and remote work was less intense. According to Amazon’s CFO, the company faced the sting of inflation too, as rising electricity and fuel costs outpaced revenue, especially after a huge facility expansion, with Amazon’s high-margin Web Services (AWS) and its advertising business filling the gap.

Inflation is taking a breather now and the three-year-long probe with EU antitrust regulators has finally reached an end, saving the company from a fine that could cost up to 10% of its global revenues. However, the macroeconomic environment may remain challenging as recession risks keep lingering on the horizon. The latest business survey from S&P Global reported a slight pickup in prices in January for the first time since spring, lifting the odds for higher interest rates as upward wage pressures persisted. Labour strikes and uncertain geopolitical conditions in Europe could be another drag for Amazon.

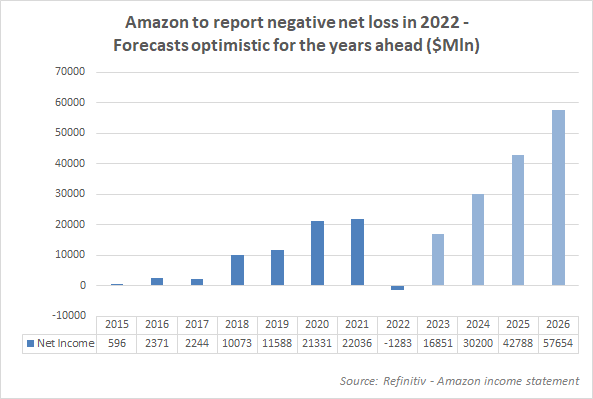

Amazon may finish 2022 with a net loss

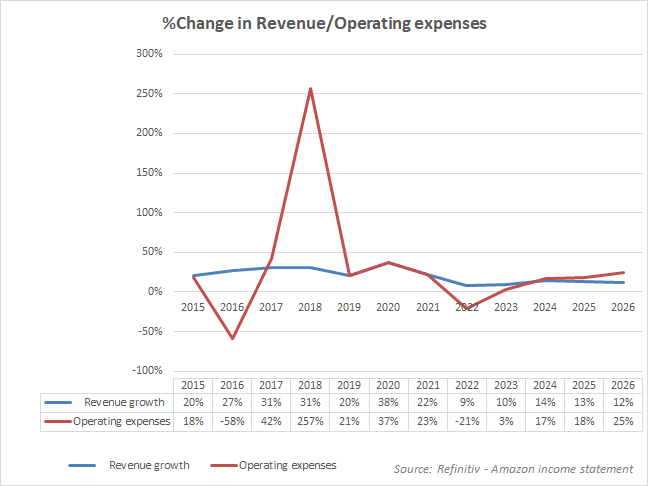

The final earnings for 2022 will probably be bleak in terms of growth. Although analysts expect a higher quarterly revenue of $145bln on the back of October’s surprising Prime Day and Christmas sales, the pace of expansion may have slowed sharply to 5.79% y/y – the softest in several years – compared to the 14.70% expansion registered in Q3 and 9.44% seen in the same period a year ago. Recall that Amazon set its Q4 revenue projections between $140-$148bln, representing year-over-year growth of 2% to 8%.

On segment levels, revenue growth in the leading cloud AWS section is expected to ease to a multi-year low of 24.10%, whereas online stores may finish the year higher by a whopping 905% surge despite a quarterly decline of -0.98%. Subscription services may not show an exciting improvement, likely rising by a relatively muted rate of 10.3% to $35bln.

Net income may come at the centre of attention given forecasts for a net loss of $1.2bln for the first time after more than a decade despite a potential 26% decline in operating expenses. In other profit metrics, the pre-tax profit could narrow by 28%, while the gross profit margin could rise at a softer pace of 1.46% to 43% compared to a 2.46% in 2021.

Earnings per share may further dampen sentiment, likely dropping to a multi-year low of -$0.12.

Amazon may face a disappointing end to 2022 and the year ahead might be choppy, according to analysts. That cannot be ruled out given that small and medium-size companies make up the majority of its user base.

Yet the leading online retailer has proved several times in its 25-year history as a public company that it can ride through the storms - it has already successfully weathered three recessions, including the dotcom bubble. Forecasts point to a growth acceleration from 2024 onwards.

Time for rebalancing

CEO Andy Jessy made markets nervous after announcing 18k layoffs globally at the start of the year in addition to eliminating 10k jobs in November. But that's reasonable after aggressive hiring during the previous two years as global markets normalized and the company sought greater cost efficiency across sectors that can survive through different economic cycles.

For example, Amazon cut its workforce in the cloud game division, where the board’s prospects have been sceptical, while it invested more funds in data centres and healthcare sections.

In valuation metrics, Amazon has a forward price-to-earnings ratio of 60, which is slightly above its historic level of 50 and more than double the one that other tech giant companies such as Netflix, Apple and Tesla hold, which suggests that investors’ growth prospects are relatively high.

Technical outlook

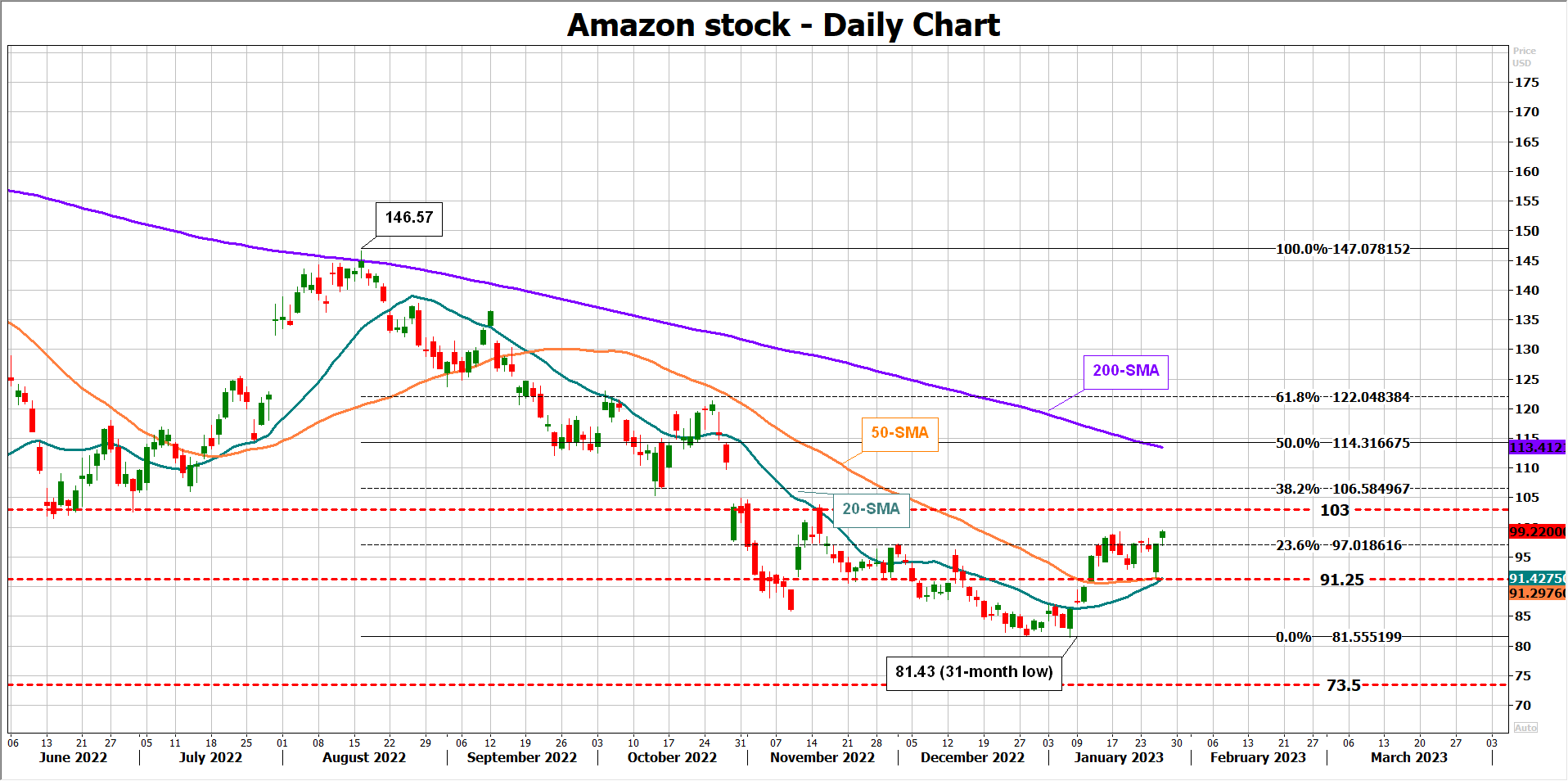

From a technical perspective though, Amazon’s stock keeps facing a dull outlook. Of course, it started the year on the right foot, adding almost 16% to its value after setting a strong foothold near its 2020 low. This is larger than the S&P 500 community’s average pickup of 4.0% but half the gain that some S&P 500 top performers such as Warner Bros and Nvidia have earned.

Traders will be eagerly looking for another close above the nearby resistance of 23.6% Fibonacci retracement of the latest downleg at $97.00 before they target the $103 barrier and then the 38.2% Fibonacci of 106.55. The 200-day simple moving average (SMA) could be more challenging at 113.40.

The earnings season has been kind to stock markets so far, mostly because a significant level of pessimism has been baked into estimates, making the actual weak numbers look encouraging. Amazon’s stock could seek fresh highs for the same reason.

On the downside, the 20- and 50-day SMAs are buffering downside pressures around 91.25. If sellers breach that floor, the spotlight will fall again on the 2020 pandemic low of 81.30, where the downtrend almost halted at the start of January. A move lower could pause somewhere between 74.00 and 73.50.

Author

Christina joined the XM investment research department in May 2017. She holds a master degree in Economics and Business from the Erasmus University Rotterdam with a specialization in International economics.