Will the newfound availability of dollars stabilize currencies against the Dollar?

Outlook:

Yesterday’s US Q4 GDP is the expected 2.1% and so backward-looking as to be irrelevant. Today we get the personal income and spending info, and the deflator, probably 1.7%. Right now central banks have better things to think about than inflation/deflation.

The great uncertainty is GDP in Q1, if we consider March alone could have obliterated growth in Jan and Feb, with Q2 at the super-scary level and maybe off the charts. Wells Fargo sees Q2 at -14.7%, the biggest in the measure’s 73 years.

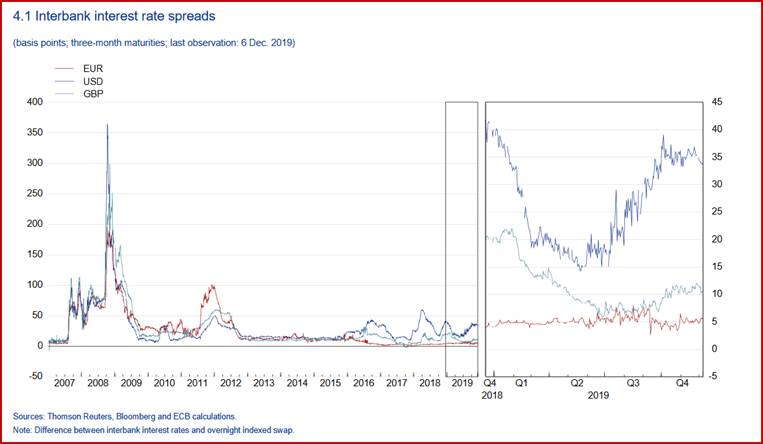

Aside from the attention-grabbing stock market gyrations, we need to consider the Fed and its new supply of dollars to anyone and everyone with a pulse. Some analysts are as sarcastic as we ever see in financial commentary about the Chinese needing dollars more than anyone, and the Fed providing them in the swap lines, whose price has returned to normal. Europeans are big dollar consumers, too. You are welcome to look at the ECB’s data on cross-currency swaps and see if you can figure out what it says. This data ends at year-end. Chandler reports “The three-month cross-currency basis swaps for the euro are now distorted in the opposite direction. Recently, the discount was the largest in several years, around 128 bp. Today the premium reached a record of a little more than 25 bp.” We can’t find a graphic to reflect this shift, but we did find that last week European borrowing under these lines was $211 billion.

The implication is that the newfound availability of dollars—in a shortage that began last fall—should stabilize the euro and other currencies, including maybe the yen, against the dollar. We are not so sure. Granted, a lack of liquidity in key instruments is a tall roadblock, but other factors count, too, including positioning and sentiment. So far it has been impossible to tease out sentiment toward government responses to the pandemic. The US botched and bungled, especially on testing and a coherent message, but so did Europe. One of the stories has it that G7 was unable to come to a combined statement because the US won’t give up the name—Wuhan virus. That’s the least of our troubles now.

Is the dollar/yen the place to look for clues? For much of the week it was putting in dojis and inside days, while refusing to match-and-surpass the previous dollar high from Feb. Then the dam broke and the dollar is falling like a rock. We find it hard to attribute this change to either swap availability or to the urban legend that repatriation always has this effect late in the first quarter, which is the final quarter in the Japanese fiscal year. We did a study a long time ago showing that yen appreciation in this quarter occurs less than half the time.

So, going into the weekend, we have to expect a little dollar recovery just because it’s a weekend coming, plus end of month next week. Next week is harder. If the bear market rally in equities is ending today, does that mean resumption of massive fear and revulsion that favors the dollar even more? Nobody knows, so don’t believe anything you read, no matter how reasonable-seeming. Now is not the time for reason. Shock has no place for reason. We suspect the dollar will not put in another V-shaped recovery, but that’s gut instinct. Monday and Tuesday are going to be a roily mess. Cut positions and wait.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat