When the going gets tough the dollar will get going

The US threat and then imposition of tariffs on a wide array of Chinese imports and the potential assignment of duties on all mainland goods have sent equity markets around the globe screaming lower.

The reaction of the currency markets has been less than excited.

The dollar has lost 2.6% versus the Japanese Yen since April 24th and 1.9% since the close on May 3th, the last trading session before President Trump announced new tariffs on Chinese imports that went into effect this past Friday, to the finish on Monday the 13th.

The yen is one of the traditional safe-haven currencies for global and specifically Asian risk, sought for the perceived economic and political stability of the islands.

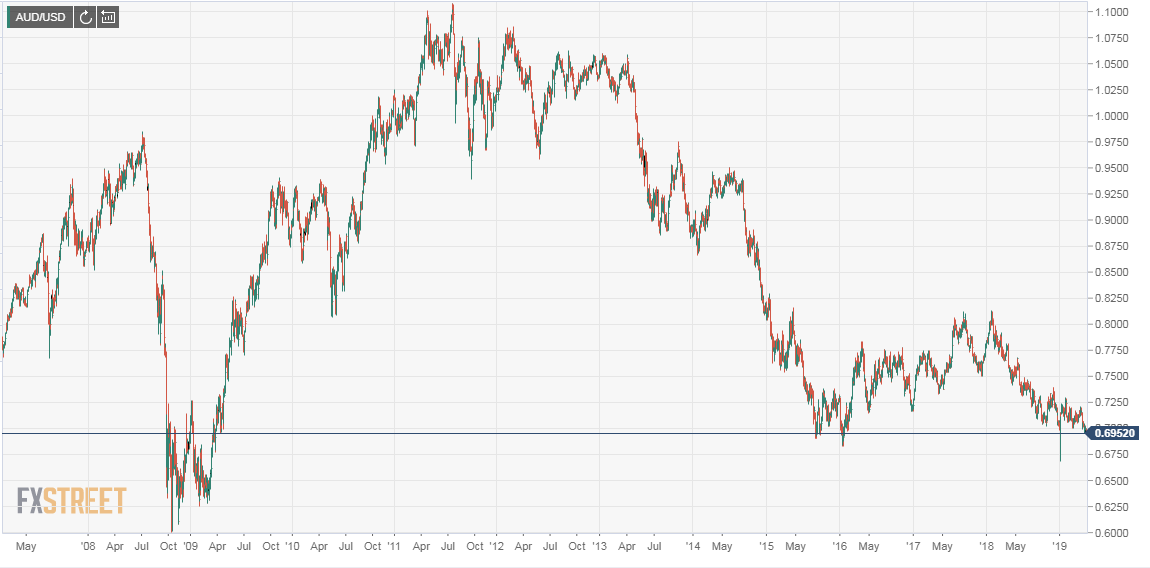

Against the euro the dollar has lost 19 points from the close on Friday May 3rd to the finish on Monday May 13th. Those are pricing points, basis points in another market, in percent it is 0.17%. Much closer to a price than a range. The dollar is higher against the Australian Dollar, New Zealand Dollar and the British Pound.

It is a curiously indecisive and restrained move for an economic conflict that has the ability to diminish growth around the world.

If the trade dispute between the world’s two largest economies is about to go from a skirmish to all-out war the impact will not be limited to China and the United States. One of the reasons the IMF reduced its projection for global GDP this year from 3.7% last October the 3.3% in April was the impact, in abeyance until last week, that a full-fledged trans-Pacific trade war would have on the weakly growing European and Japanese economies.

When the Federal Reserve first moved to a neutral stance in January the FOMC statement called for patience but Chairman Powell was more specific in his news conference. An escalating trade dispute between China and the US was one of the risks requiring insurance.

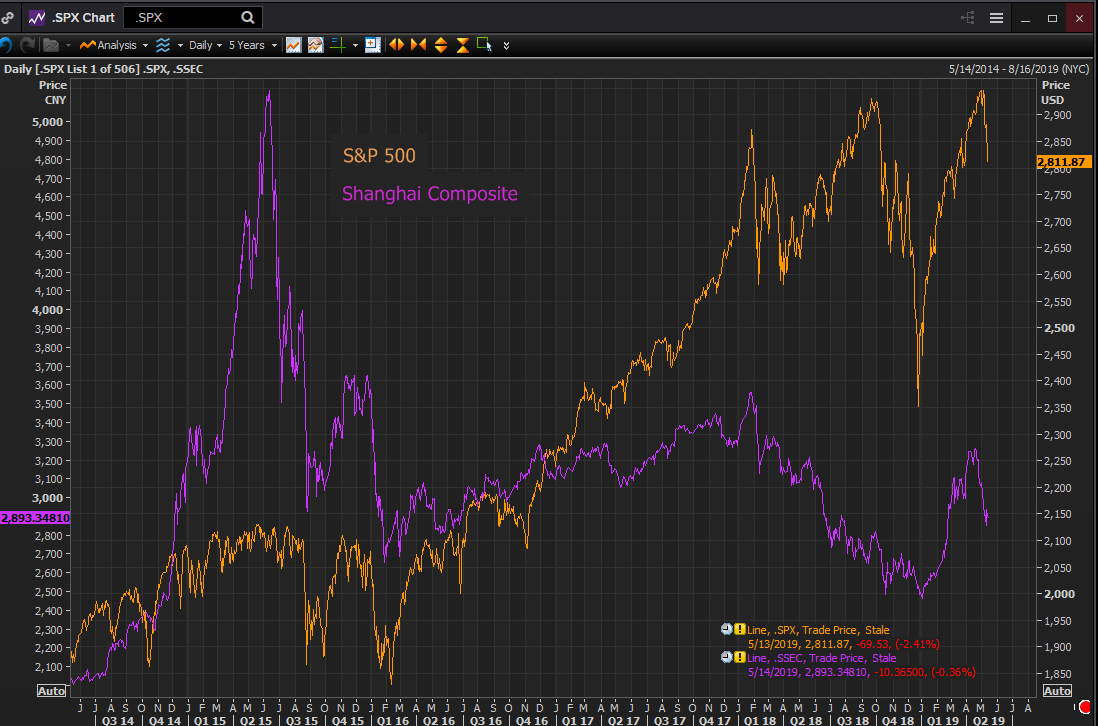

China and the United States are not just the two largest economies they are also the most dynamic and far-reaching. China draws in resources from around the world and acts as work and assembly shop for vast numbers of consumer products. The United States is the largest and wealthiest market and the premier destination for every exporter from high value manufacturers like Mercedes to makers of trinkets for children and everything in-between.

If the growth of these two giants is about to suffer its ramifications will be felt in every corner of the global economy. If China and the United States slow or slip into recession there is no other economic entity on the planet that can take up the slack.

Over the past 30 years the dollar has been the safe-haven currency of choice when markets are truly panicked.

In the months leading to the financial crisis the dollar and dollar assets were in demand everywhere. From July 2008 through November the greenback rose 20.8% against the euro, 26.5% versus the sterling, 21.0% against the Swiss Franc, 23.3% versus the Canadian Dollar and 35% against the Australian Dollar. The one exception was the Japanese Yen which rose 11.2%.

The current situation and the potential is not comparable the financial crisis. Even if the two antagonists placed tariffs on every item that each sells to the other, it might push the global economy to a recession, but it might not.

The trade dispute between the United States and China could develop into a crisis for the global trade regime that has evolved since the Second World War and for China after her entry into the World Trade Organization (WTO) in 2001. It could plunge the world economy into a coordinated slowdown. But there are more reasons to think that it will eventually be settled than to assume ever increasing acrimony and economic dislocation.

Economic and political logic is still on the side of negotiation and agreement. That is one reason for the blasé response of the dollar, the euro and their coevals. Markets have not lost faith in the ultimate deal.

For international companies that have large operations in China the damage from the dispute is real and aimed directly at their bottom line. The collapse in equities assigns lower value to those companies whose prospects are damaged by the dispute.

Reuters

That brings us to the second reason currency markets seem agnostic. It is not clear whose economy would fare best in a protracted trade war or even the end of WTO regulations.

Given past performance, it would probably be the United States rather than China, Europe or Japan. Its large internal market and small dependence on exports leaves its economic growth less beholden to global trends. The Fed’s interest rate policy over the last four years has left it with a much greater ability to stimulate the economy should it become necessary.

If and when the US-China trade negations break down, the dollar will resume its historical safe-haven status and it will be aided by US economic growth.

The dollar is not flying because the circumstances do not, as yet, warrant it.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.