What market response would shift the Fed?

Outlook

This week the likely big event is US CPI on Thursday. We also have an ECB policy meeting, US trade (tomorrow) and US consumer sentiment (Friday). In between is Japan’s revision of Q1 GDP, German industrial production and ZEW, and the Bank of Canada (Wednesday).

The CAD is not only the strongest currency, but also the most interesting. After the sub-par jobs report (a loss of 68,000 jobs, more than double the forecast), chatter is getting louder about the BoC retreating from its taper stance. We may have to wait for Deputy Gov Lane and his progress report on Thursday. Uncertainty may temper enthusiasm for the CAD, but don’t count on it. Goldman Sachs sees limited risk from the BoC meeting and prefers the CAD because of rising oil prices, a lovely basket of exports, and the real rate not actually overvalued. We are not alone in noting that Canada’s vaccination schedule is better than the US and the UK, and that matters. A lot.

We were surprised at the NFP on Friday when forecasts were as high as one million, just showing that forecasting is a lousy occupation (but somebody has to do it). ADP has egg on its face for a second month. Nevertheless, the economy is roaring back and never forget that payrolls are wildly inaccurate in the first place. Maybe a big chunk of all that roaring is jobs off the grid, aka the gray economy. Meanwhile, wages are set to rise at important places like McDonalds and confidence is high that next time it will be different.

Also surprising was the data-driven knee-jerk reaction in FX, following weeks in which nothing much of the “high-frequency data” was influential and measures of volatility were contracting. The COT and other reports show shorting the dollar is still the popular mode but we wonder what would drive a correction. We thought payrolls would do it, and we continue to worry that CPI later this week can still do it. At the least, the new euro lows on Thursday and Friday indicate the anti-dollar bias is hardly written in stone.

Markets are accepting the Fed narrative that inflation will be transitory, in part because the Big Bank analysts agree with that point of view and have written tomes showing why it’s the best-case scenario. So far we have the current inflation rate at 4.2% (from 2.6%) and core at 3% from 1.6%. The question becomes how much higher does inflation have to go to drive a wedge between the Fed and the Big Banks and the rest of the market? That leads to Question #2: what market response, if any, would shift the Fed? We don’t expect the data to shift the Fed, but we do expect it to respond to anything that looks like destabilization.

The probability is low of any such thing, although so far today S&P futures are still negative. It looks like the dollar downdraft is continuing, but we worry about one-day reversals and about a Tuesday pullback.

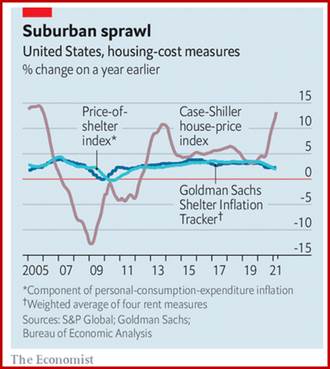

More about inflation: We have seen inflation due to sticky vs. flexible prices and “trimmed” by the Cleveland Fed, but if the cost of housing is a primary driver, how do we think about that? Last week The Economist had a chart from Goldman Sachs showing something it names a “Shelter Inflation Tracker.” Again we see that house prices are not the right measure (house are an investment, not a consumer item), but instead, rents. And rents are rising at only about 2% nationwide, with those few exceptional places (mostly in California). Rents are 20% of core PCE, so pay attention.

Logically, the cost of rentals should catch up to house prices, although some reasons can be found for the price-to-rent ratio remaining high, including the low cost of mortgages, the slow pace of construction, and the unthinkable idea that house prices could fall while rental costs do not. One study quoted in The Economist story says “two-thirds of any adjustment in price-to-rent ratios tends to fall on prices. In other words, America might be able to have either a strong housing market or quiescent inflation–but not both.”

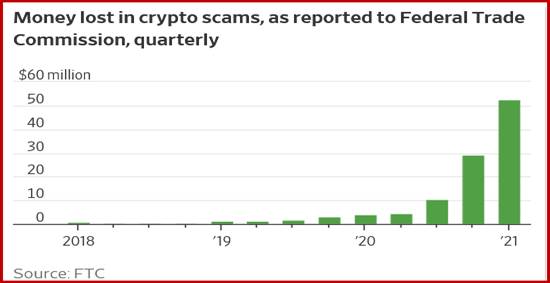

Tidbit: The WSJ shows how crypto scams are starting to hit. See the chart. It’s ridiculous that people who fret about cyber-hacking in energy pipelines, the electrical grid and meat packing do not worry about hacking in crypto. Crypto us starting to look like a Russian ploy.

Tidbits: Facebook banned Trump for another two years (from Jan 7). He is already banned from Twitter permanently and his blog lasted less than a month (comedian Bill Maher said it’s because Trump and his supporters don’t read). Trump believes he will be magically restored to the presidency in August through some mechanism that does not exist (barring a military coup). Psychiatrists say on TV that Trump’s narcissism does not permit admitting he lost the election and his delusions can only get worse. The question is whether he can get enough others to buy into those delusions. So far he’s doing okay with the majority of Republican party voters and members of Congress, but they are still a minority overall. Those with the patience watched Trump speak at a political event over the weekend and report he was a little worse in terms of lies and incoherence.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat