What happens if the Fed does chicken out and eases policy to assuage the equity traders?

Outlook: We get retail sales and industrial production today, both of which (or neither) can influence risk sentiment. Retail sales might disappoint, given the lousy consumer outlook presented in the Michigan consumer survey. Sales rose 0.5% in March, vs. 0.6% forecast, with 0.9% the consensus forecast this time but Trading Economics feeling glum with 0.6%.

The headline number is not what counts, anyway, because so much inflation in embedded in autos and gasoline and retail sales is not inflation-adjusted. See the chart excluding those–a measly 0.2% gain.

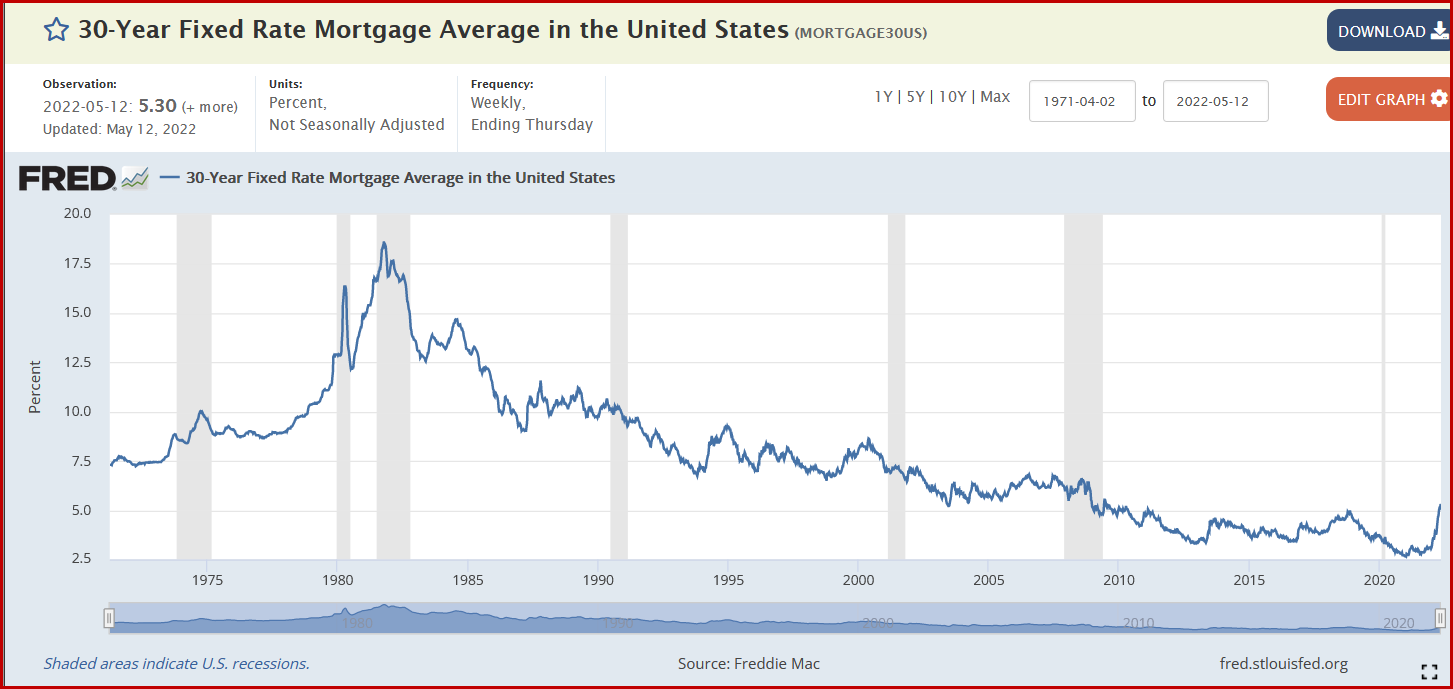

Industrial output may have the same fate. It rose 5.5% y/y in March After 7.5% in Feb, for an annual rate of about 8.1% in Q1–catch-up. This time we can’t find a consensus forecast but Trading Economics has 2%, which will look bad compared to 5.5% in March. In addition, we get business inventories for March and the May NAHB housing market index. We are not following the screaming stories about the death of American real estate, which assume that mortgage rates over 5-6% are the end of the world. Rates count, of course, but housing costs and sales depend also on labor market mobility, cost of new construction, and a ton of other factors it can be heard to tease apart. In the grand scheme of things, mortgage rates are still very low, if at the end of a decades-long decline.

After these releases, the Atlanta Fed will deliver a revised Q2 GDPNow forecast. We need to view the Atlanta Fed in the light of the latest trend in commentary–that various markets, especially equities, are “overpricing” the risk of a recession. This is the view of a JP Morgan analyst. Bloomberg wonders what happens if the Fed does chicken out and eases policy to assuage the equity guys? This is just poking the bear. We have no reason–zero–to think the Fed will chicken out. In fact, it can’t, since it considers its standing among the broad public as a key instrument in the fight against inflation. It’d not, since we’d guess a fat majority of Americans have no idea what the Fed is, but never mind.

The fresh data is not going to change the developing pushback against the dollar, which seems divorced from the data and sentiment changes in other markets, especially equities. If we can’t find a reasonable reason, it must be position adjustment by big players and then the rolling wagon joiners. It might even have an element of stop-hunting. We don’t believe for a minute that the Fed chickening out is behind it, or any other big institutional change like that. One that is plausible, just barely, is Ukraine winning the war.

The Case of the Mysterious Yen Rally: We are getting a technically significant reversal in dollar/yen that is inexplicable on the face of it, and not likely to last. But it can wreak some damage before the ship steadies. One potential explanation is a sense of dread coming from the latest Chinese data so buying yen is an act of risk-aversion. Re-opening Shanghai on June 1 can’t erase the awful numbers yesterday and we can’t expect warp-speed recovery. This a variation of the “China sneezes” theme that supposedly accounts for medieval migrations and the like. Do the Japanese feel more risk averse because of events in China and that drives them to the safe haven of their home currency?

We doubt it, if only because the Chinese April data was always going to be near-catastrophic. After all, Shanghai was shuttered over 6 weeks ago. What happened in the past three days to change minds on this subject? If re-opening the financial and industrial central hub of the Chinese economy has boosted the Australian dollar, does it boost the yen, too? This is the same cause, different effect on risk perception.

Another idea is that Japanese investors enamored of the US 10-year at 2.50-3.00% (when their own is 0-0. 25%) are put off by a seeming peak in the US note. As we showed yesterday, the 10-year breakeven is dipping. The idea is that Japanese investors think the Fed will cave and as recession looms, possibly halt hiking for a while, or postpone QT. Hardly anyone thinks the Fed will lose its nerve, but perhaps just the prospect of QT is scaring them away from the dollar.

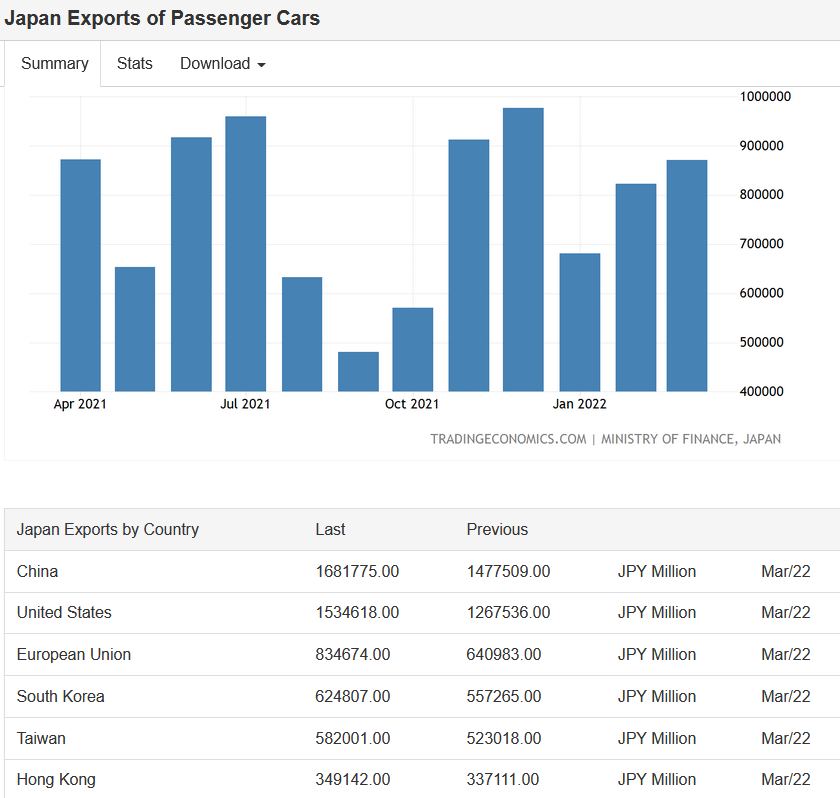

Finally, some common-sense ideas, including a drop in imports because foreign goods are becoming too expensive. On the export side, the same supply chain problems and rising industrial materials costs everyone has, but in the case of Japan, producers are drawing in their horns because demand for high-end Japanese goods is weak–especially cars, car parts and fancy equipment of various sorts, all of which need chips.

See the auto export chart from TradingEconomics.com. This doesn’t begin to cover all transport equipment and parts, other machinery, electrical equipment, steel, etc. And note the top three destinations–China, US and EU–all three pretty much in the soup.

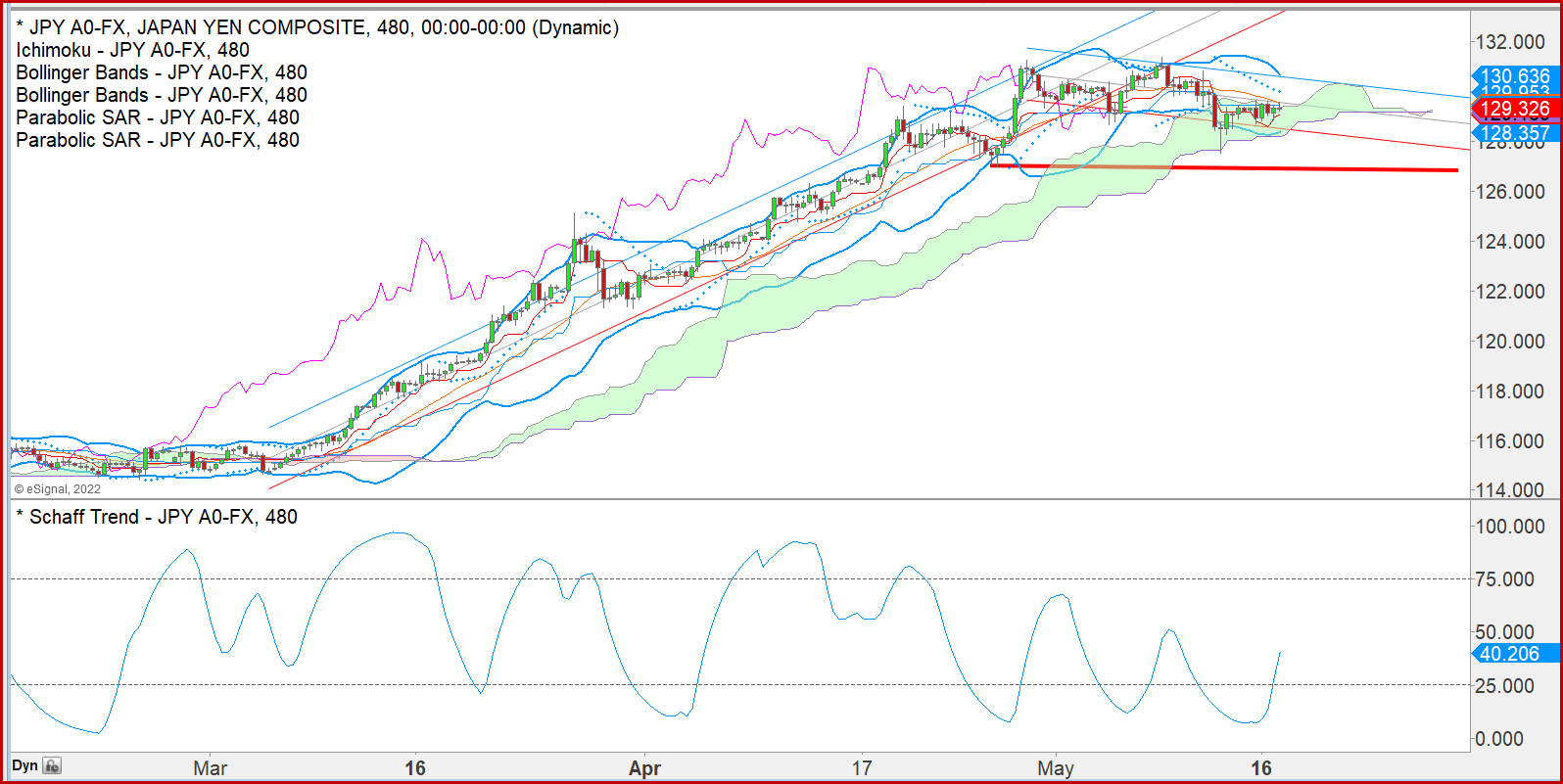

On the chart–shown in the 480-minute version–the last meaningful low was on April 26 at 127.00. The current move should stop before that. And that’s if it breaks the cloud bottom, which is by no means assured.

Tidbit: former Fed chairman Bernanke has a new book coming out this week titled 21st Century Monetary Policy: The Federal Reserve From the Great Inflation to Covid-19 . According to Sorkin in the NY Times, Bernanke says “for the first time since the 1970s, [the US] could be heading toward a period of stagflation characterized by slow growth, job losses plus higher prices. book.

Recession can be avoided if, crucially, the Fed’s credibility with the public is maintained and the supply chain issues can get fixed. Powell should keep the 2% inflation target. He’s not worried about a housing bust because the number of subprimes is so much lower this time. This is, of course, not what former TreasSec Summers says–he sees recession. But Bernanke is modest and Summers is a blowhard, so we’ll go with Ben.

Tidbit: Euronews reports EC members are irate over some countries holding the EC hostage over the Russian oil sanctions. “The proposal to phase out Russian oil across the bloc was unveiled 12 days ago by Commission chief Ursula von der Leyen. But unlike the five previous sanction packages that were swiftly approved by the 27 capitals, negotiations have stalled with no resolution seemingly in sight.

“Four member states particularly dependent on Russian fossil fuels – Bulgaria, the Czech Republic, Hungary and Slovakia – are demanding the European Commission allow them to continue importing Russian energy past December 2024, which already constitutes a significant delay from the rest of the bloc. Hungary is seen as the primary hold-out with Prime Minister Viktor Orban describing the oil ban as an ‘atomic bomb’ for his country's economy.” The most outspoken: Lithuania's Foreign Affairs Minister, Gabrielius Landsbergis, who said "We have to agree. We cannot be held hostage."

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat