Week Ahead on Wall Street (SPY) (QQQ): No jobs, no taper, no rally. Can earnings change things?

- Friday's jobs report misses expectations badly, 194k versus 500k expected.

- Stocks whipsaw after the number with little direction.

- Headwinds are growing with yields rising and jobs growth slowing.

Equity markets are treading water on Friday with little in the way of strong direction after a weak employment report. This bad number (194k versus 500k expected) has a silver lining in that it may allow the Fed to delay tapering its stimulus program which the equity market has become increasingly reliant on. But that should not really be comforting in the face of the dreaded stagflation. The US may be headed for slowing growth but rising inflation. Certainly, Friday's price action is indicative of this with the ten-year yield continuing higher and trading above 1.6% now, a multi-month high. Adding to inflationary pressures is the march of energy prices with European gas prices hitting all-time highs this week and West Texas Intermediate (WTI) Crude breaking above $80 for the first time in seven years. Price rises are already being passed onto customers in Europe with surging gas prices likely to add significantly to next month's CPI readings and the same will happen in the US. In the face of such inflationary pressures, the Nasdaq, in particular, will struggle. Already on Friday, it is the worst performing index. The Nasdaq finds itself at the mercy of conflicting forces and we remarked on this post the employment report. The initial spike in the Nasdaq after the release was the knee-jerk reaction by traders eyeing a delay to Fed tapering. The Fed balance sheet has a huge correlation with the SPY and QQQ. But while the Fed may not taper and raise rates, that does not mean inflation and real rates cannot rise. The Nasdaq is cornered.

Some good news at least this week with the gradual acceptance that Evergrande may not take down the global financial system as investors focused instead on something that could, that being a US debt default. However, reprieve came from the unlikeliest of sources, Senate Minority Leader Mitch McConnell. In playing a sharp piece of political one-upmanship he placated nervous markets and this led to the turnaround in US indices on Wednesday which had a strong follow-through on Thursday. All we are left with then on the worry wall is inflation, and what a worry it is. We have managed to take delta, Evergrande, and a US default off the wall but the Q3 earnings season is likely to lead to inflation concerns coming front and centre. Already, as mentioned previously, it seems every earnings report is accompanied by the caveat of rising costs and supply chain issues. We are likely to hear more of this in the Q3 earnings season.

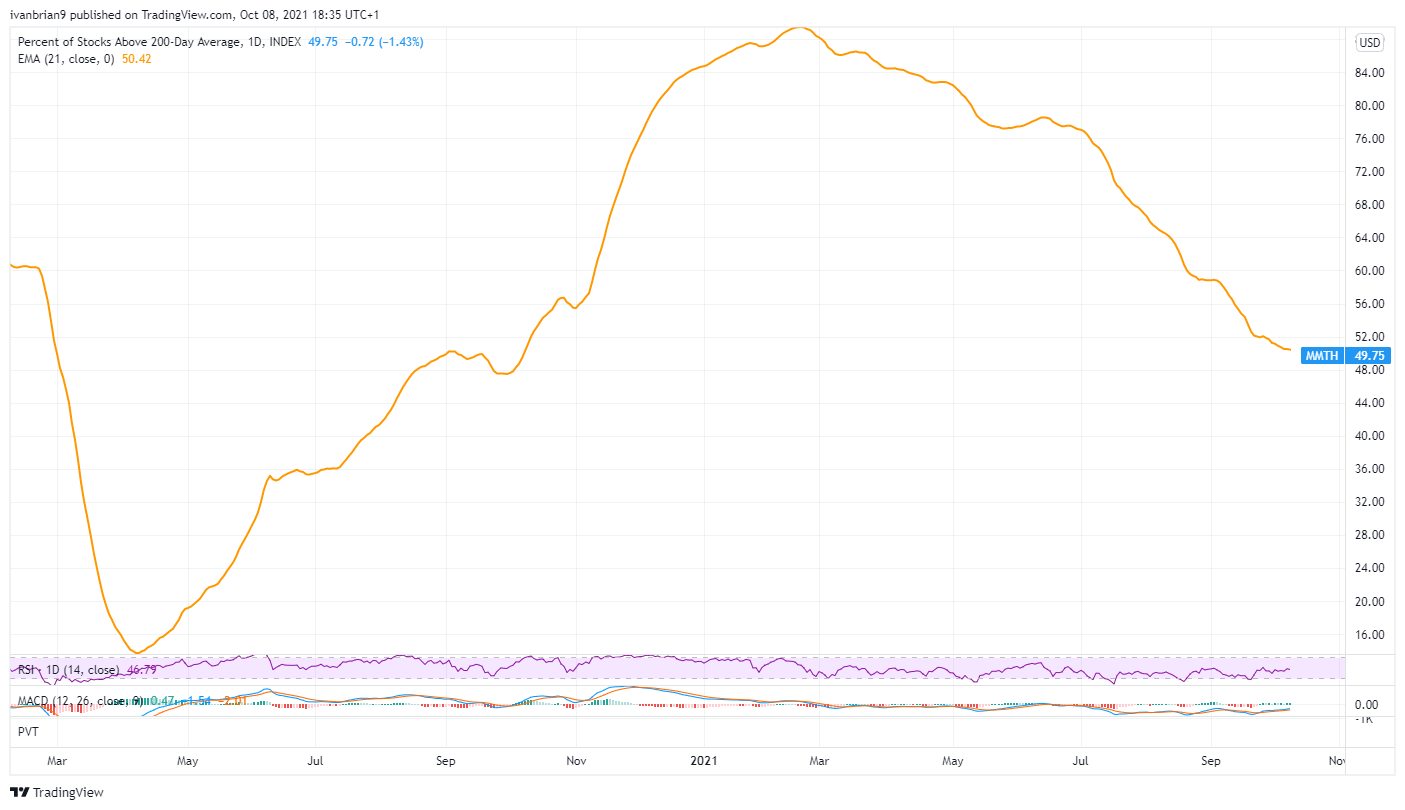

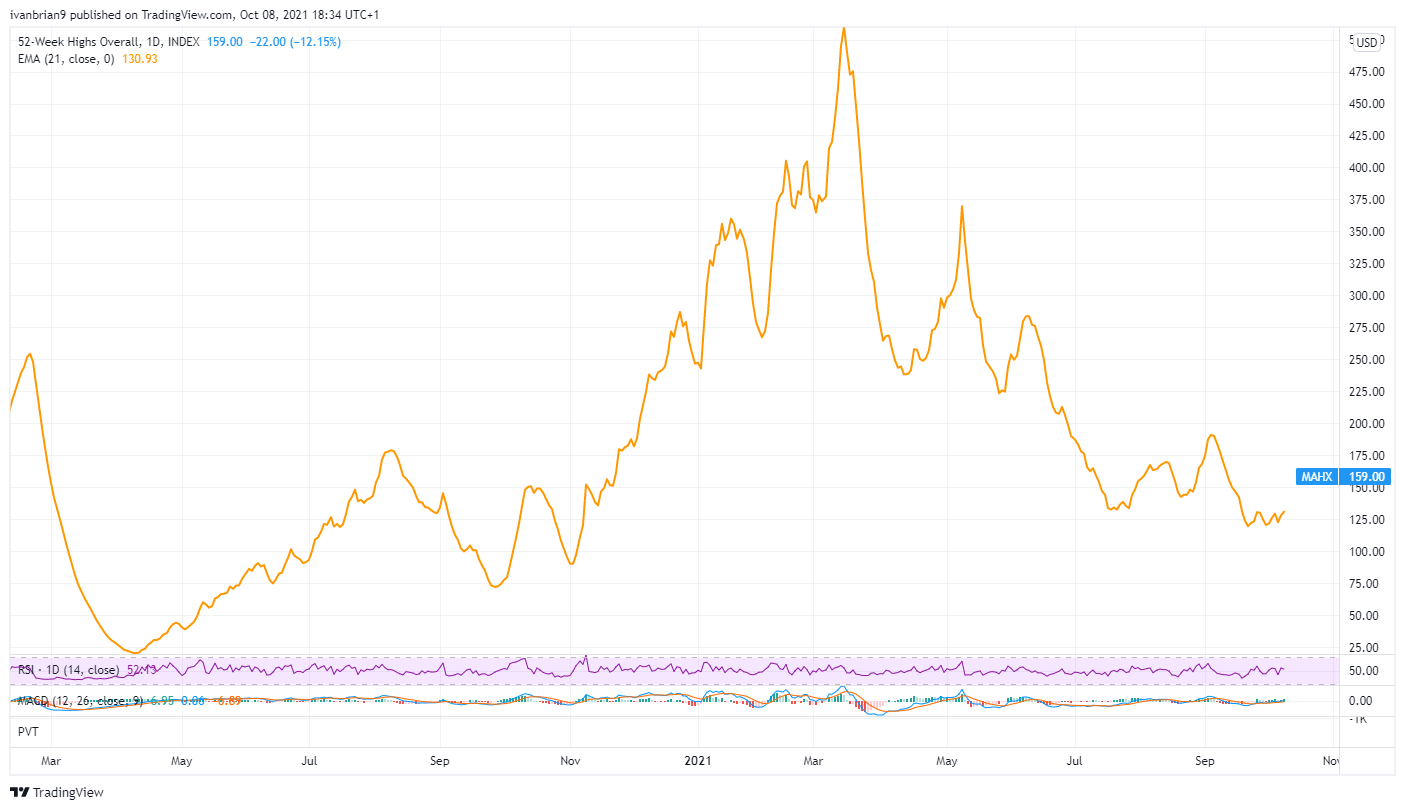

Market breadth indicators continue to decline as shown in the charts below. The top chart is the percent of stocks above their 200-day moving average and the lower is the amount of stocks making new 52 week highs. Both show pretty decent declines from the summer highs. Indicative of a less than optimistic scenario. Of course, the concentration of gains has largely been focused on the mega names. The small-cap space, as represented by the Russell 2000 (IWM), has not been as loved despite meme stock madness.

The Russell 2000 continues to trade in its massive sideways range for 2021 with a break lower surely now on the cards but it has outperformed the Nasdaq and S&P over the last two to three weeks. This will likely continue.

It might be time to get excited about buying Chinese tech names again according to the market ear. The most beaten up and despairing of sectors shows some bottoming out potential on the chart. Names such as DIDI, BABA, JD, PDD, et al staged strong rallies on Thursday and it feels to us like the sector is waiting for a catalyst to break higher. The bullish divergence is in place from the Relative Strength Index (RSI) and Moving Average Convergence Divergence (MACD) in KWEB (China Internet ETF). High risk but worth keeping an eye on if risk-on is back on!

Fund flow data

The latest fund flow data from Refinitiv Lipper Alpha shows inflows to Equity Exchange Traded Funds (ETF's) for the first time in nearly a month. This is despite the market volatility. Maybe buy the dip still dominated for ETF players. The Nasdaq (QQQ) took in $1.3 billion but the SPY saw $3.2 billion in outflows. Also of note were inflows to non-ETF equity funds for the first time in fifteen weeks. Buy the dip indeed.

SPY stock forecast

The chop continues and October is known for it. Direction is clearly bearish on the medium-term horizon and we feel Friday's price action has reaffirmed the dead cat bounce on Wednesday and Thursday. Yields up, equities down will likely be the theme next week. Breaking above $444 is our pivot, below we are bearish. $415 remains our extended buy the dip, a lot of volume support there from the 200-day, volume profile and Volume Weighted Average Price (VWAP) for the year.

Nasdaq (QQQ) stock forecast

This one looks even worse, repeating last week's remarks I know but look at that bounce from the longer term lower (blue) trendline. The MACD is miles apart, the RSI is weakening and the market breadth mentioned above is declining. Yields are rising, need we say more!

SPY earnings due

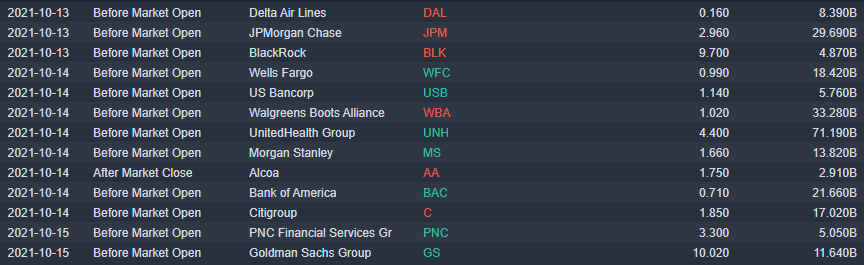

So it begins! Banks as ever first up and rising yields will suit them but the benefits may not hit until the next quarter. In a rising yield environment, bank stocks are defensive.

Source: Benzinga Pro

Economic releases

Author

Ivan Brian

FXStreet

Ivan Brian started his career with AIB Bank in corporate finance and then worked for seven years at Baxter. He started as a macro analyst before becoming Head of Research and then CFO.