Week ahead: Minutes from major central banks in focus

Minutes from the FOMC, the European Central Bank (ECB) and the Reserve Bank of Australia (RBA) occupy the macro throne this week.

FOMC meeting minutes

The Fed minutes will be the highlight event of the week for many market participants. The latest policy meeting saw the Fed leave the Fed Funds rate unchanged at 5.25%-5.50% (22-year high) for a second successive meeting, as widely expected.

You will also recall that the post-rate statement observed only minor changes:

September’s rate statement:

Recent indicators suggest that economic activity has been expanding at a solid pace. Job gains have slowed in recent months but remain strong, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

November’s rate statement:

Recent indicators suggest that economic activity expanded at a strong pace in the third quarter. Job gains have moderated since earlier in the year but remain strong, and the unemployment rate has remained low. Inflation remains elevated.

The U.S. banking system is sound and resilient. Tighter financial and credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain. The Committee remains highly attentive to inflation risks.

Fed Chair Powell’s press conference followed 30 minutes later and was also somewhat unchanged from the previous presser. Notable points were that policy remains restrictive along with the Fed remaining committed to maintaining restrictive policy, and the Fed needs to ‘proceed carefully’ as the full effects of previous tightening have yet to be felt.

As made clear, the Fed is prepared to tighten policy further if needed. Still, the string of disappointing US economic data following the FOMC meeting has seen markets curb bets on any potential rate hike in the near future. US CPI and PPI inflation slowed, lower non-farm employment change and higher unemployment, along with disappointing retail sales, and ISM manufacturing and services PMIs registering poor numbers have seen markets reprice rate cuts to 100bps in 2024 (this is an increase from 75bps).

Therefore, the minutes will be an essential watch this week; should the minutes emphasise the possibility of another rate hike down the road, any dollar bid could be short-lived given the market’s current perception. Of course, any mention of rate cuts (doubtful) will weigh on the buck.

Finally, as a friendly reminder, US banks will be closed on Thursday in observance of Thanksgiving Day.

ECB meeting minutes

The latest minutes from the ECB meeting in late October will be watched on Thursday, which generally does not rattle the financial markets too much.

At the tail end of October, the ECB pressed the pause button on policy firming for all three benchmark rates, which ended ten consecutive rate hikes over 14 months that increased its main refinancing rate for a total of 450bps.

For many, the ECB might be done with rate increases, though some desks believe there’s a chance we may see the central bank attempt to squeeze through one more rate hike. ECB President Christine Lagarde did not explicitly confirm that they’re finished with rate hikes and noted that it would be ‘premature’ to discuss cuts. Time will tell. Another question, of course, assuming the ECB is done and dusted, is how long will rates remain in restrictive territory? Markets are currently pricing in the possibility of cuts in mid-2024 (like the FOMC, the ECB is also now priced to cut by 100bps next year).

RBA meeting minutes

Ahead of the FOMC minutes on Tuesday, the Reserve Bank of Australia (RBA) meeting minutes will be released, which will be used by traders and investors to gather further information after the central bank increased its Official Cash Rate by 25bps to 4.35% (12-year high) on 7 November, as expected. The rate increase follows four consecutive meetings on hold.

You will recall that the RBA noted that further tightening would depend on incoming data—no surprises. In her post-meeting statement, the relatively new RBA Governor Michelle Bullock communicated that inflation is expected to be around 3.5% by the end of next year and at the upper boundary of the target range (2-3%) by the end of 2025.

The latest policy tweak was seen as a ‘dovish hike’ and is thought to be mainly on the back of the remarks in the post-statement, exchanging the following sentence from the October statement: ‘Some further tightening of monetary policy may be required’ to ‘Whether further tightening of monetary policy is required’. This indicates that this could be the last hike in this cycle, hence a dovish hike.

It will be interesting to see what the minutes hold, but as of now, it looks as though the RBA hiking regime is done, and if this is reinforced in the minutes, a bearish response in the AUD (bullish response in domestic equity markets) could unfold. As of writing, the ASX 30-Day Interbank Cash Rate Futures fully price in a no-change at the next policy meeting on 5 December.

Additional tier-1 data this week

21 November:

- Canada Inflation Data (CPI)

- US Housing Data (Existing Home Sales)

22 November:

- US Weekly Unemployment Claims

- US Durable Goods Orders

- Revised US (UoM) Consumer Sentiment Data

23 November:

- European and UK Manufacturing and Services PMIs

- Tokyo Core CPI

24 November:

- German IFO Business Climate Survey

- Canada Retail Sales

- US Manufacturing and Services PMIs

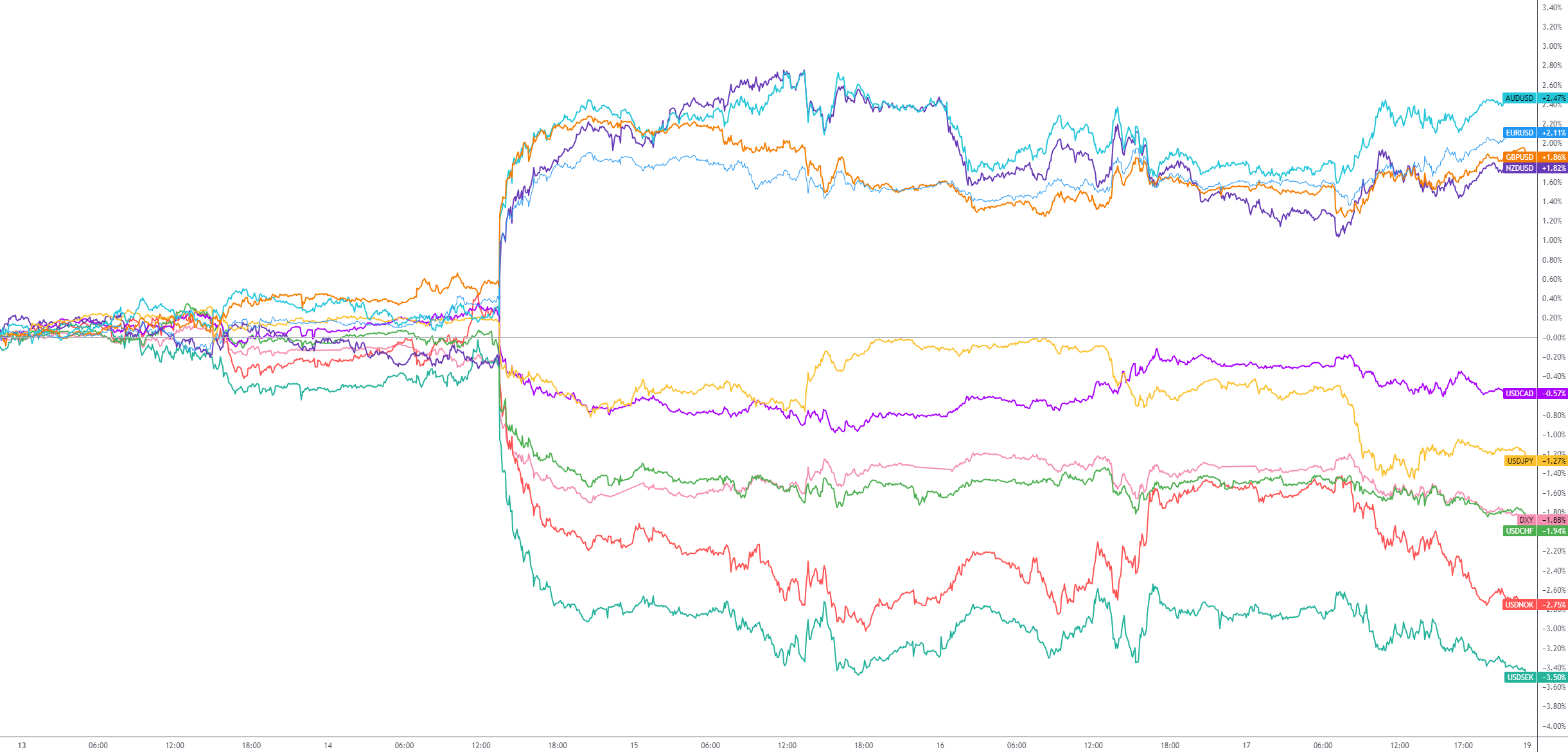

G10 FX (5-day change):

Charts: TradingView

Author

Aaron Hill

FP Markets

After completing his Bachelor’s degree in English and Creative Writing in the UK, and subsequently spending a handful of years teaching English as a foreign language teacher around Asia, Aaron was introduced to financial trading,