Week ahead: Crude Oil returns to focus

While the coronavirus continues to infect at an alarming rate, a new focus has emerged which is also helping steer the markets: Crude Oil. Theoretical tweets by US President Trump regarding oil supply cutbacks forced Saudi Arabia to show its hand and call for an emergency OPEC+ meeting to ask for all to contribute to a cutback. Crude shot higher over 30% last week. NFP data showed that 701,000 people lost jobs in March, however most of the data was collected before lockdowns began. Initial Claims will continue to be watched. China PMI data was better than expected, while the rest of the world was worse. Is China recovering? However, we must remember that the coronavirus is still the “main attraction” for traders.

US President Trump tweeted on Thursday that Saudi Arabia and Russia were expected to announce an oil production cut of 10-15 million barrels per day. Both countries denied this claim, however Saudi Arabia did call for an OPEC+ meeting to ask ALL producers to cut back supply. Gulf States and Russia will meet on Monday, while Trump will met with US oil producers on Friday. Watch for more comments this week regarding the OPEC meeting. Oil prices may move higher if 1) new buyers enter the market looking for a production cut and 2) shorts get squeezed, forcing them out of positions at higher prices.

The US Dollar was volatile once again, as the DXY was up nearly 2.25%. This led to large moves in some major US Dollar pairs, such as AUD/USD (-2.72%), EUR/USD (-2.87%), NZD/USD (-3.00%). In addition, many Emerging Market currencies were hit particularly hard, such as USD/TRY (+4.4%), USD/MXN (+6.00%), and USD/ZAR (+8.00%). Stock markets took a breather this week as no major indices opened “Limit up” or “Limit Down”. The FTSE ended the week down 1.5%, while the DAX and NASDAQ were down less than 1%. The S&P 500 was down -2.25%, while the Dow Jones closed down -2.7%. Gold and silver were also down less than -0.5% on the week.

Last week, coronavirus cases surpassed 1,000,000 worldwide. As fiscal and monetary stimulus continues, there also continues to be a desperate need for Personal Protective Equipment (PPE) for health professionals as infection rates continue to climb throughout most of the world. US President Trump invoked the Defense Production Act earlier this week and companies such as Ford and GM have repurposed their equipment to make ventilators. 3M is making millions of N95 masks. Both large and small companies across the global are making PPE to help keep front line workers safe. Companies such as Amazon and Britain’s Tesco are hiring additional workers to help move products and stock shelves.

Q1 earnings reports will begin this month. Traders will be watching to see how not only Q1 reports, but also how emergency measures affect bottoms line outlooks for Q2. Tesco reports earnings on Wednesday. In addition, markets will be watching airlines and hospitality providers to see how the coronavirus measures have affected them. Delta Airlines reports Wednesday as well.

Although many of the state primaries for US Presidential candidates have been postponed, Wisconsin and Alaska are still planning on holding their primaries on Tuesday and Friday, respectively. Recall, there are only 2 candidates remaining for the Democratic nomination to face off against Republican Donald Trump in the November election for President. Joe Biden currently leads with 1,217 delegates, while Bernie Sanders has 914 delegates. 1,991 delegates are needed to win the Democratic nomination.

NFP data released Friday showed that the US economy lost 701,000 jobs for March during the survey period which ended on March 12th. The survey period ended before state lockdowns were put into effect, such as Florida, Georgia, and Tennessee. The lockdown closed non-essential businesses, including many service businesses such as restaurants, bars, nightclubs, hair salons and gyms. Over the last 2 weeks, initial jobless claims totaled nearly 10,000,000. Initial Claims will be continued to be watched as it is the timeliest employment data we have. Expectations for this week’s initial claims reading is currently 5,000,000!

Below is a list of important economic data to be released this week:

Monday

- EU: Construction PMIs (MAR)

- UK: Construction PMI (MAR)

Tuesday

- Australia: Interest Rate Decision

- Germany: Industrial Production (FEB)

- US: IBD/TIPP Economic Optimism (APR)

Wednesday

- Australia: RBA Chart Pack

- Canada: Housing Starts (MAR)

- US: FOMC Minutes

- Crude Inventories

Thursday

- Australia: Financial Stability Review

- Germany: Trade Balance (FEB)

- UK: Trade Balance (FEB)

- Canada: Employment Change (MAR)

- US: Initial Claims (Week Ending April 4th)

- US: PPI (MAR)

- US: Inflation Rate (MAR)

Friday

- China: Inflation Rate (MAR)

- China: PPI (MAR)

- US: Inflation Rate (MAR)

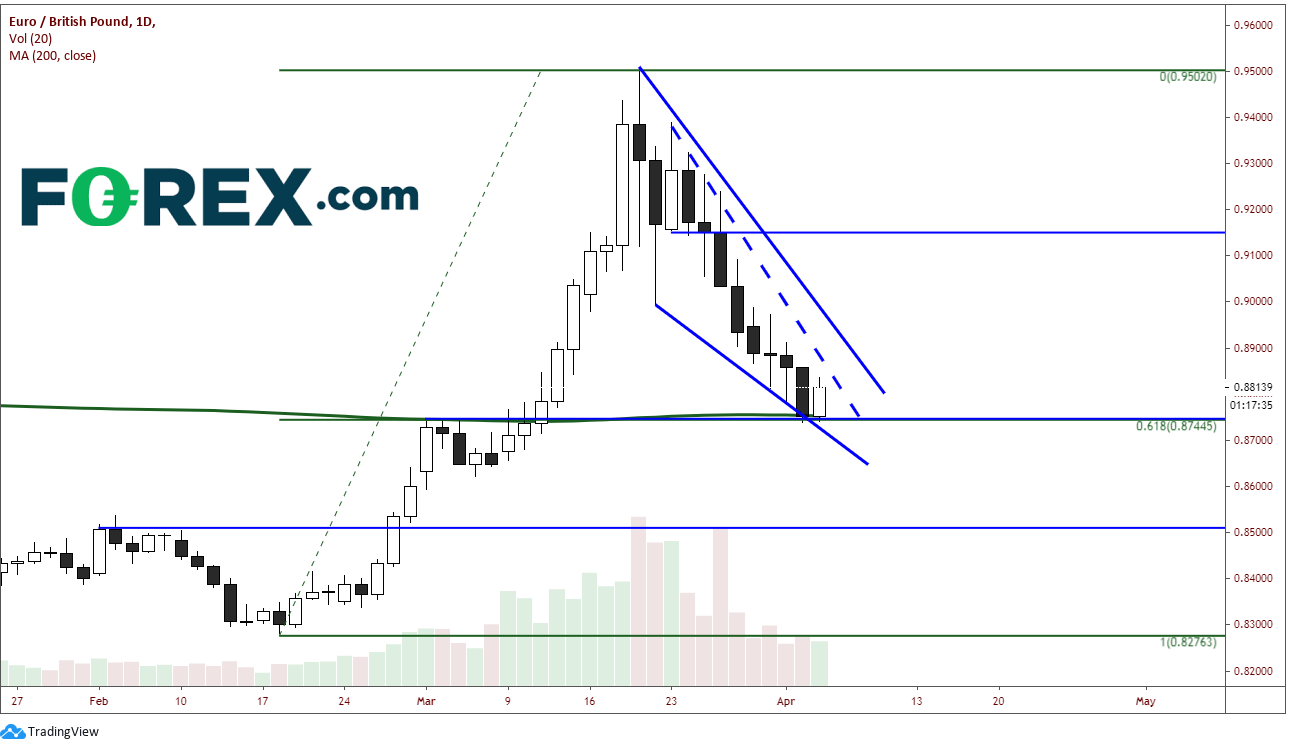

Chart of the Week: Daily EUR/GBP

Source: Tradingview, FOREX.com

After the Euro outpaced the Pound from February 18th to March 19th, EUR/GBP began to selloff. The pair pulled back to the 61.8% Fibonacci retracement level at .8745 in a wedge like fashion. In addition to the retracement level, there is also trendline support from the wedge, horizontal support from the prior highs in early March, and support from the 200 Day Moving Average. This will be a major break if price closed below these support levels, with the next horizontal support near .8500. There are 2 wedges which have formed on the move lower. First resistance is at the dashed trendline near.8857. Second resistance is at the solid trendline near .8990. The third level of resistance is horizontal resistance near .9150.

Traders should continue to look for volatility across the board as the coronavirus continues to take its toll on world markets. Oil will also be in focus and everyone works for a solution to cut back supply.

Have a great weekend and please remember to always wash your hands!

Author

Joe Perry CMT

Forex Analytix

Joe Perry is currently Global Head of Business Development at Forex Analytix. From 2000-2018, Joe traded at SAC Capital Advisors and then Point72 Asset Management. He has traded foreign exchange and commodity futures for the last 20 years.