Week ahead – Could strong US data shift focus from Trump’s rhetoric?

- Significant market moves keep investors on their toes.

- Trump has been the primary source of volatility, mainly when targeting the Fed.

- Pivotal US data releases next week as markets adjust to potential Warsh Fed nomination.

- RBA, BoE and ECB meet next week; decent chances of surprises across the board.

- Dollar/Yen prepares for February 8 elections; gold experiences its first substantial correction.

Dollar’s outlook remains bleak

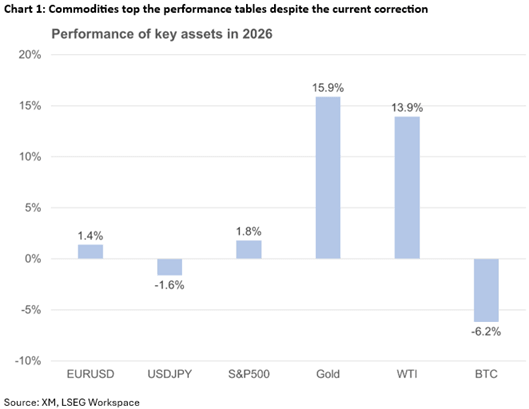

The final week of January can be safely characterized as tumultuous, given the significant market moves and the plethora of issues troubling investors’ minds. The dollar has been in the spotlight due to persistent weakness, commodities, led by gold and silver, have been making strides in uncharted waters, and the major US stock indices have been tentatively trying to post fresh all-time highs.

The root of these moves is the uncertainty stemming from US President Trump’s actions and rhetoric. Since the start of the year, he has authorized the transfer of the Venezuelan President to the US, threatened his closest European NATO allies with additional tariffs over Greenland, and is also ready to raise the punitive tariffs on imports from both Canada and South Korea.

But the dollar is mostly hurt by Trump’s strategy towards the Fed. The mid-month judicial probe targeting Fed Chair Powell, the Supreme Court case about Lisa Cook’s firing, and speculation regarding the new Fed Chair are casting a shadow over the future of one of the most respected institutions in the US. Particularly, the nomination of a ‘soft’ candidate for the Fed top spot – with the latest information pointing to Kevin Warsh being the chosen one – could put the final nail in the dollar’s coffin.

US economy is solid footing

Despite Trump’s shenanigans, the US economy is progressing well, with the Fed keeping rates constant, as widely expected. Notably, Chair Powell commented after the FOMC meeting that “the outlook for economic activity has clearly improved since the last meeting”, and “upside risks to inflation and downside risks to employment have diminished”. That said, as noted by Powell, there are some tentative signs of consumer spending fatigue, keeping expectations for two rate cuts in 2026 alive.

In the meantime, corporate America is progressing well also, with the current earnings round proving satisfactory, fueling a muted rally in risk assets, particularly on sessions during which US sovereign yields retreat. Interestingly, the S&P 500 index has never finished January in negative territory with Trump in office.

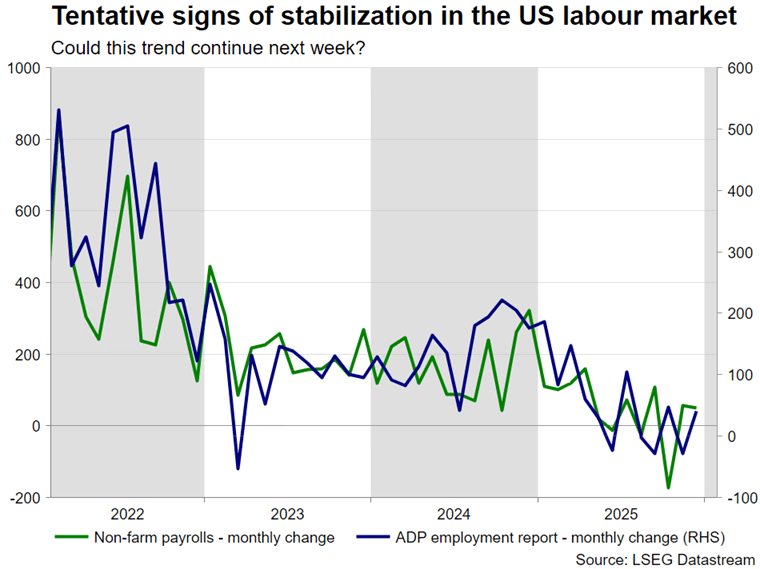

Further good news from the US labour market?

With investors being alert to Trump’s commentary and geopolitics, the focus next week will shift to the usual early-month US data releases and Fedspeak. The calendar includes the key ISM Manufacturing and Services PMI surveys, and Wednesday’s ADP employment report, but the highlight of the week is Friday’s January nonfarm payroll report. A solid 70k increase is currently forecast for the latter, maintaining the recent trend of positive prints and weakening the Fed doves’ arguments for a ‘fragile job market’.

A strong set of US data, confirming current indications for a stabilizing labour market, along with another small pullback in inflationary pressures, could offer some significant respite to the dollar. However, hawkish Fedspeak is critical for the durability of such a move. Despite the upbeat Fed meeting, and the fact that Miran voted for a 25bps cut this time, hawkish Fedspeak is not the baseline scenario at this stage.

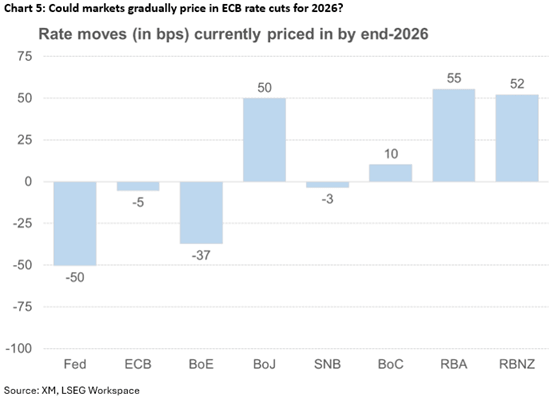

The hawkish (RBA), the boring (ECB) and the anxious (BoE)?

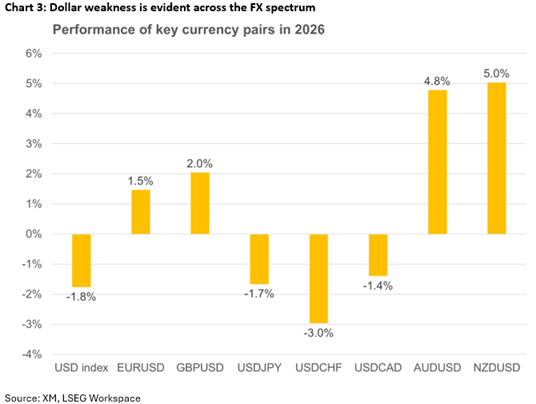

The dollar has been faring very poorly against most major currencies, particularly against the Antipodeans. Interestingly, the RBA, the BoE and the ECB will hold their respective rate-setting meetings next week.

After a short easing cycle, there are strong expectations of the RBA changing its course next week due to January’s robust data releases: the January S&P Global PMI surveys posted impressive jumps, the unemployment rate dropped unexpectedly to 4.1%, and, more importantly, the Q4 inflation print climbed to 3.6%.

At the December meeting, the RBA highlighted the upside risk to inflation and the tight labour market conditions, with Governor Bullock stating that “if inflation does not slow, then it will be considered at the February meeting”. Being true to her words, a 25bps rate hike will be discussed on Tuesday, with the market assigning a 72% probability to such a move.

Aussie/Dollar has climbed to the highest level since February 2023, fully taking advantage of the US dollar’s troubles and some positive momentum from China. The announcement of a rate hike will most likely result in a short-term rally, but this might prove short-lived if the accompanying statement is not hawkish enough.

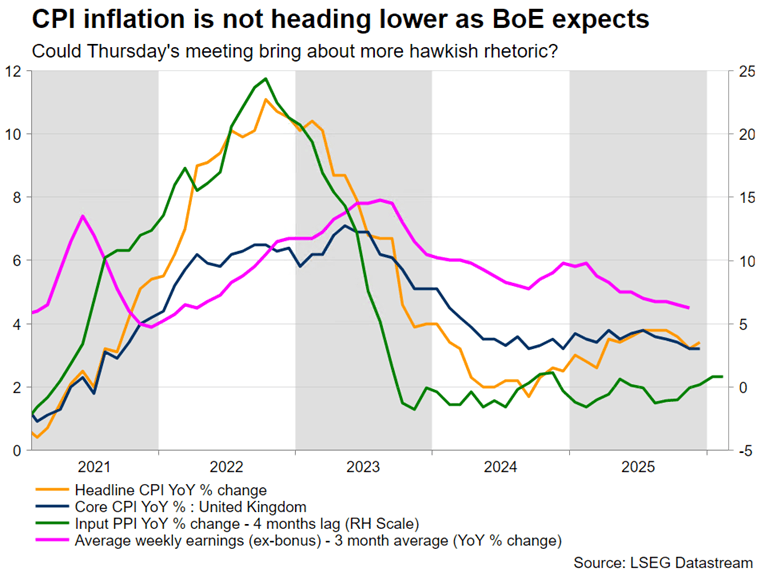

Do doves still hold the upper hand at the BoE?

With developments elsewhere shifting the focus away from the UK, the pound has been benefiting from dollar troubles. Pound/dollar is up 2.3% in January – its strongest start to the year since 2019 – after an impressive 7.7% rally in 2025.

Most data prints during January produced upside surprises – particularly the robust December retail sales and the January PMI surveys – with the market currently pricing just a 5% probability of a rate cut on Thursday. Crucially, the small pickup in CPI and the sustainably elevated average earnings growth have been keeping a lid on MPC doves.

A rate cut next week would be a massive surprise, denting the pound’s recent strength against both the euro and the dollar. Similarly, a possible 5-4 voting result in favour of a pause – with Governor Baily siding with the hawks – would also threaten the pound’s current gains. On the other hand, acknowledgment of the persistent inflationary pressure might boost the pound, particularly if the quarterly inflation projections point to less steady decline over the forecast horizon.

Therefore, the pound stands to gain from a possible lack of dovish tilt and a stronger vote in support for the expected rate pause. That said, the innate dovishness of the BoE cannot be underestimated, with Bailey once again keeping both doves and hawks happy by voting for a pause and keeping rate cuts firmly on the table.

Could the ECB sound alarmed by Euro’s appreciation?

The ECB policy meeting is probably going to be the least exciting one, as no rate cut or noticeable shift in the rhetoric is expected, with President Lagarde et al. most likely remaining content with the underlying growth and inflation dynamics. However, behind-closed-doors discussions and the Q&A will focus on tariffs and the euro strength.

The threat of additional tariffs, potentially forcing eurozone governments to retaliate, and the strong Euro, which is not favoured by most eurozone countries as they are unable to compete with China and other manufacturing powerhouses, could force the ECB to reconsider its stance, putting rate cuts back in the spotlight.

All in all, the eurozone is not dazzling with its growth momentum, but stability appears to pay off. That said, it would be interesting to see if euro/dollar manages to consistently remain above 1.1908, without eurozone-based bullish catalysts.

Dollar/yen bounces higher after drop – Focus shifts to snap elections

Last week’s rate check from the New York Fed, which resulted in a significant sell-off, has probably changed the momentum in dollar/yen. Investors are wondering whether this move proves short-lived, like in April 2024, when it dropped from 160.20 to 151.85, but in just a handful of sessions it climbed, eventually reaching the 161 level. Another scenario is that it might resembles the July - September 2024 move, when actual intervention resulted in a 14% decline, which left yen bears badly bruised.

With intervention risk remaining high, the focus shifts to the February 8 snap elections. Following PM Takaichi’s comment that she will step down if her LDP party does not gain a majority in the Lower House, the stakes are exceptionally high. Based on current polls, the majority looks secure, but the yen would be under severe pressure if Takaichi’s election ‘gamble’ fails, forcing the BoJ to be activated once again in Dollar/Yen.

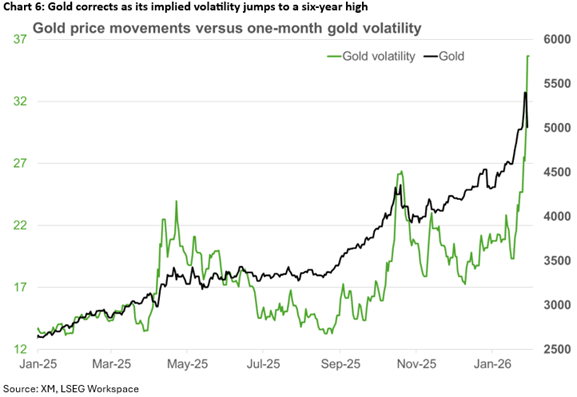

Gold and Silver correction takes place

Following the unrelenting rally since early 2025, partly due to the dollar’s persistent weakness, gold and silver investors are experiencing an overdue correction, partly signalled by the metals’ skyrocketing implied volatility. With their recent price gains being parabolic, this decline feels like a healthy reaction. That said, the bullish case for these precious metals remains intact, with geopolitics potentially in the foreground if Trump continues with his warmongering against Iran.

Author

Achilleas joined XM as an Investment Analyst in November 2022. He holds a BSc in Business Economics from Middlesex University and a MSc in Mathematical Trading and Finance from Bayes Business School, City University.