We get CPI on Wednesday and the ECB rate decision on Thursday

Outlook

We get CPI on Wednesday and the ECB rate decision on Thursday. CPI doesn’t matter at all because even if it fails to show ongoing improvement, rate cut expectations are as firm as they get. All the same, another dip in inflation would be nice and even nicer would be a dip in the household inflation expectations published by the NY Fed later today.

The CME FedWatch tool now has 75% betting on 25 bp at the next Fed meeting (9/18) and only 25% sticking to 50 bp. On Sunday around noon, it was 70%/30%, so a pretty fast retreat.

As Dolan at Reuters reports, “… the [NFP] report was neither strong enough to completely dispel slowdown and recession fears for next year nor was it seen to be weak enough to nudge the Federal Reserve into a jumbo 50-basis-point interest rate cut this month.

“Top Fed policymakers Christopher Waller and John Williams underscored expectations that a Sept. 18 cut is coming - the former even said the easing cycle should be 'frontloaded'. But neither seemed panicked enough to suggest 50 bps was needed yet.”

Told you so. Now the 50 bp is behind us, there’s another hurdle to jump—that the market is still betting on over 100 bp in cuts by year-end. If it’s 25 bp in Sept, that leaves either Nov or Dec for 50 bp. This remains a troublesome issue, because those expecting such a big cut must think there is a crisis coming. Indeed, some analysts persist in saying the US is already in a recession and we just don’t know it.

We get a new Atlanta Fed GDPNow estimate for Q3 today. Last week it was a small rise to 2.1%. We can agree that the official definition of recession, two quarters of negative growth, is not useful and most of the time comes long after actual recession is in full swing or even ending, but to say we are already in recession lacks convincing data.

Important Tidbit: A Reader sent us this entry. It buttresses our view that the jobs numbers are claptrap and the US still has a labor shortage. Here it is in its entirety:

“The US Still Has a Worker Shortage: Believe it or not, the U.S. labor shortage may be getting worse. Job growth is “anemic on Main Street” but it’s not because owners of small firms aren’t still trying to hire.

“That’s according to the latest monthly employer survey from the National Federation of Independent Business. In NFIB’s August survey, 40 percent (seasonally adjusted) of all owners reported job openings they could not fill in the current period, up 2 points from July. Thirty-six percent have openings for skilled workers (up 4 points) and 15 percent have openings for unskilled labor (down 1 point).

The NFIB economist adds that job overall, the percent of firms with one or more job openings they can’t fill remains at exceptionally high levels. This indicates continued upward pressure on compensation and, ultimately, on inflation. In a range of industries from transportation to manufacturing to professional services to retail, a higher percentage of small firms reported job openings in the NFIB August survey than in the organization’s August 2023 survey.

Two Newish Things: The Economist magazine this week had two things, one we knew and one we had discounted. First, the issue of the lack of credibility of Chinese statistics. We already knew this, but it has gotten worse.

Most recently it was the trade data vs. what the customs department reports. That made the news last week. But there is also GDP itself, the youth unemployment rate, cash flows in and out of equities (now quarterly from monthly), even the number of Covid deaths. The government is “strangling information about the economy.” A critical factor: we do not know the after-effects of Covid and the effects of the harsh Covid polices.

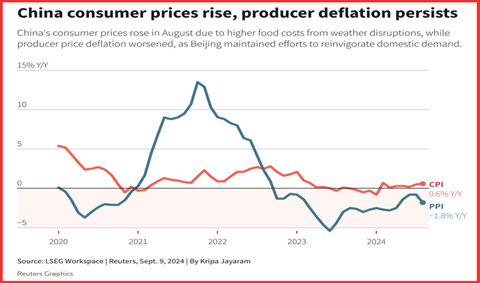

Then there is the lack of a robust response to the crash of savings invested in property. No wonder Chinese consumers are curling up in the corner. The most recent data is a small gain in consumer prices. See the chart. But it lacks credibility. The causes of the gain include bad weather, food prices, and other non-organic demand factors.

Second, the Bagehot column goes to great lengths to support the Labor Party’s support for a return to the European fold after the economically disastrous Brexit. PM Stermer was always a “remainer” and we are flabbergasted to read that 78% of Labor voters would support a return to the EU and 69% favor a new referendum within 5 years. Blimey! The Economist always opposed Brexit. Its full-throated support of Starmer and returning might be overstated, but we doubt it would cite fake numbers. Something to keep in mind.

Forecast

Rate cut mania is in full retreat, not only because the labor market statistics are now seen as having been misinterpreted but also because it’s rare for the Fed to do double the “usual” or “normal” amount.

It takes a crisis to get a 50 bp change but looking at historical data, 50 bp is not all that rare--like the housing crisis of 2008, the dot-com bust and before then, 9/11. Even during the fx crisis in 1998, the cuts were 25 pp, but in 1990-91, the Gulf War crisis, we had several 50 bp cuts. Bottom line, 50 bp is not all the rare…. Because we have a lot of crises.

This raises the question of what happens to the dollar if it’s 25 bp and what happens if it’s 50 bp. The tentative dollar gain on Friday indicates the FX market is suffering a reality check—25 bp it is. Does the dollar go into rally mode? We are placing a small bet that this is it. On the other hand, 50 bp brings on a renewed dollar dump, no matter what the ECB does on Thursday. That’s the conventional interpretation.

MishTalk points out that Trump would prefer 50 bp because it will bring the dollar down, something he says he wants (but then excoriates countries that eschew the dollar, proving his ignorance of finance).

Political Tidbit: The latest polls show Trump neck-in-neck with Harris and even sometimes a tad ahead. The presidential debate is tomorrow night. The pundits’ advice to the debaters is riveting. The microphones will not be open, so if Trump interrupts and shouts, as is his wont, the TV audience won’t know (unless the cameraman keeps him in view). And Harris won’t have the chance to reprise her decisive Pence put down: “I am speaking.”

Harris will almost certainly try to rile Trump and push him off his self-created pedestal right out of the gate. He’s the indicted criminal and she is the prosecutor. Some opine that content doesn’t matter, but rather style. This is not a true debate, with orderly facts and fact-checking, but rather Entertainment (not quite Roman circus but the same genre).

Never mind that economists are reaming Trump’s economic ideas, including former Fed govs and Big Banks. Goldman Sachs, for example, says Trump policies (including those stupid tariffs) will bring US growth down into recession. Harris’ would give a bump, if a small one, to GDP.

Alas, the polls might favor Harris (and increasingly so), but the Silver Bulletin points out that on the electoral college count, Trump has a big lead. Again, it’s those 7 swing states.

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

This is an excerpt from “The Rockefeller Morning Briefing,” which is far larger (about 10 pages). The Briefing has been published every day for over 25 years and represents experienced analysis and insight. The report offers deep background and is not intended to guide FX trading. Rockefeller produces other reports (in spot and futures) for trading purposes.

To get a two-week trial of the full reports plus traders advice for only $3.95. Click here!

Author

Barbara Rockefeller

Rockefeller Treasury Services, Inc.

Experience Before founding Rockefeller Treasury, Barbara worked at Citibank and other banks as a risk manager, new product developer (Cititrend), FX trader, advisor and loan officer. Miss Rockefeller is engaged to perform FX-relat