USD/JPY Weekly Forecast: US data confirms recovery but markets take profit

- USD/JPY falters as Treasury yields slide, drops 1% on the week.

- 10-year yield sheds 15 points to Thursday, recovers 5 on Friday.

- Excellent US Retail Sales, Jobless Claims provide no immediate dollar support.

- Consolidation likely in USD/JPY as markets await initial US second quarter data.

- FXStreet Forecast Poll predicts extending USD/JPY weakness.

In a classic case of following the bouncing yields, the USD/JPY sank for the first four days as US Treasury yields saw their steepest losses in a month then rebounded as the credit market reversed on Friday.

From Monday’s close at 1.675% the return on the benchmark 10-year note dropped 15 basis points to 1.530% on Thursday and the USD/JPY descended from 109.66 to 108.78. Friday’s reversal in yield, up six points to 1.59% stabilized the USD/JPY above 108.80 after Thursday’s intra-day dip to 108.61.

US 10-year Treasury yield

CNBC

Treasury yields have been the currency market focus since the New Year. After closing out 2020 at 0.916%, the 10-year rose moderately to to the first week in February and then rapidly ascended to peak at 1.776% on March 30. Its highest pandemic close was the next day at 1.753%.

That period from early February to the end of March also marks the sharpest climb of the USD/JPY, from 104.57 to 110.71.

Interest rates in the first three months of the year quarter have responded to the brightening prospects for the US economy, a view that reached fruition this week.

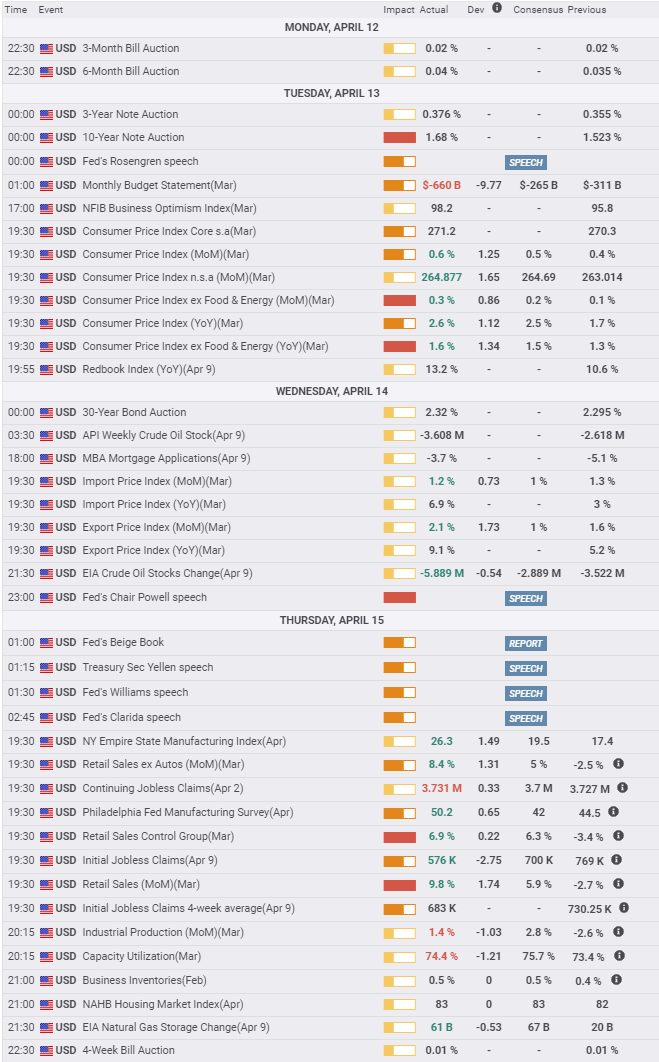

First quarter gross domestic product (GDP) jumped to 8.3% annualized in the Atlanta Federal Reserve GDPNow model on April 15.

Retail Sales vaulted 9.8% in March, far more than the 5.9% forecast and even besting the 7.6% burst in January. The federal government stimulus payments of $1,400 in March, like the $600 check in January, was largely responsible. The Control Group category of sales that enters the Bureau of Economic Analysis’ GDP calculation rose a cumulative 12.2% in January, February and March.

Sales seconded the excellent March payrolls, released on April 2, as did Thursday’s initial Jobless Claims report for April 9 which showed 576,000 filers, by far the lowest of the pandemic era. Stocks rallied on the news with the Dow reaching another all-time record but Treasury yields and the dollar fell on Thursday.

The recent decline in Treasury yields is due to two factors.

First, US economic growth may or may not maintain its more than 8% expansion into the second and third quarters. Much depends on the final size and success of the Biden administration’s planned $3 trillion infrastructure spending. The March Retail Sales figures likely mark a top in consumption.

The second doubt is the ability of the US to avoid a general rise in COVID-19 cases and the potential economic disruption that would cause.

Neither is assured, but regarding the panndemic the outlook is promising with 3-4 million vaccinations daily.

Given the sharp sell-off in bonds this year, prices move inversely to yields, a profit pause was clearly in order. The overall trend in yields remains higher with the 10-year return expected to revert to more historical levels at or above 2% in the coming month, provided the US economy stays buoyant.

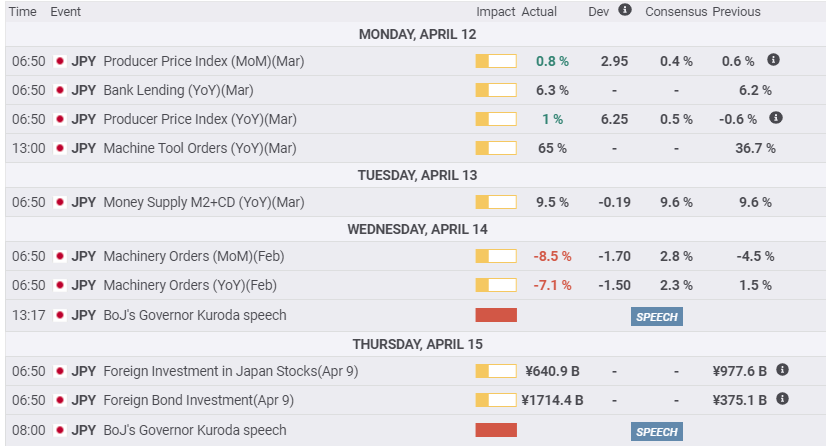

Japanese producer prices doubled their forecasts in March, but as in the US the gain is largely in comparison last year's collapse. The same will hold true for April. Machinery orders in February were much weaker than expected and an absolute decline of the year. At least in that traditional strong export category there is no notice or revival.

Bank of Japan (BOJ) Governor Haruhiko Kuroda said on Thursday that any recovery in the economy will be modest due to remaing caution from the pandemic. "Services consumption will remain under pressure for the time being due to a resurgence in COVID-19 infections since last autumn," the BOJ chief noted in a speech to the bank's branch managers.

Japanese economic statistics should continue to confirm that outlook in the weeks ahead.

USD/JPY outlook

American Treasury yields will not relinquish their sway on the USD/JPY but a temporary halt in rate gains seems likely as traders await economic information from the opening of the second quarter.

First quarter US GDP is reported on April 27 and except for the preliminary Michigan Consumer Sentiment which was weaker than expected at 86.5, April data will not be issued until May. The ISM Manufacturing PMI on May 3 is the first major piece of information.

Absent the driving force of US interest rates technical factors will assume prominence.

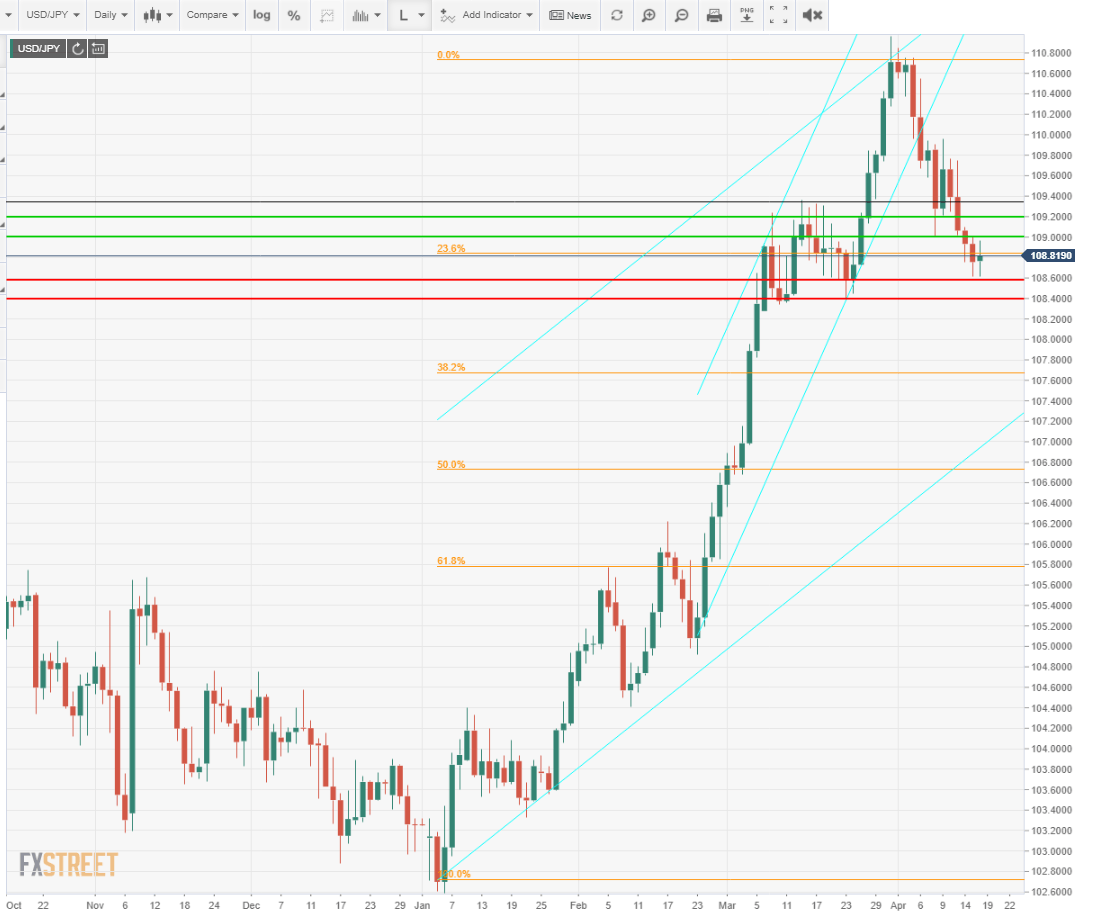

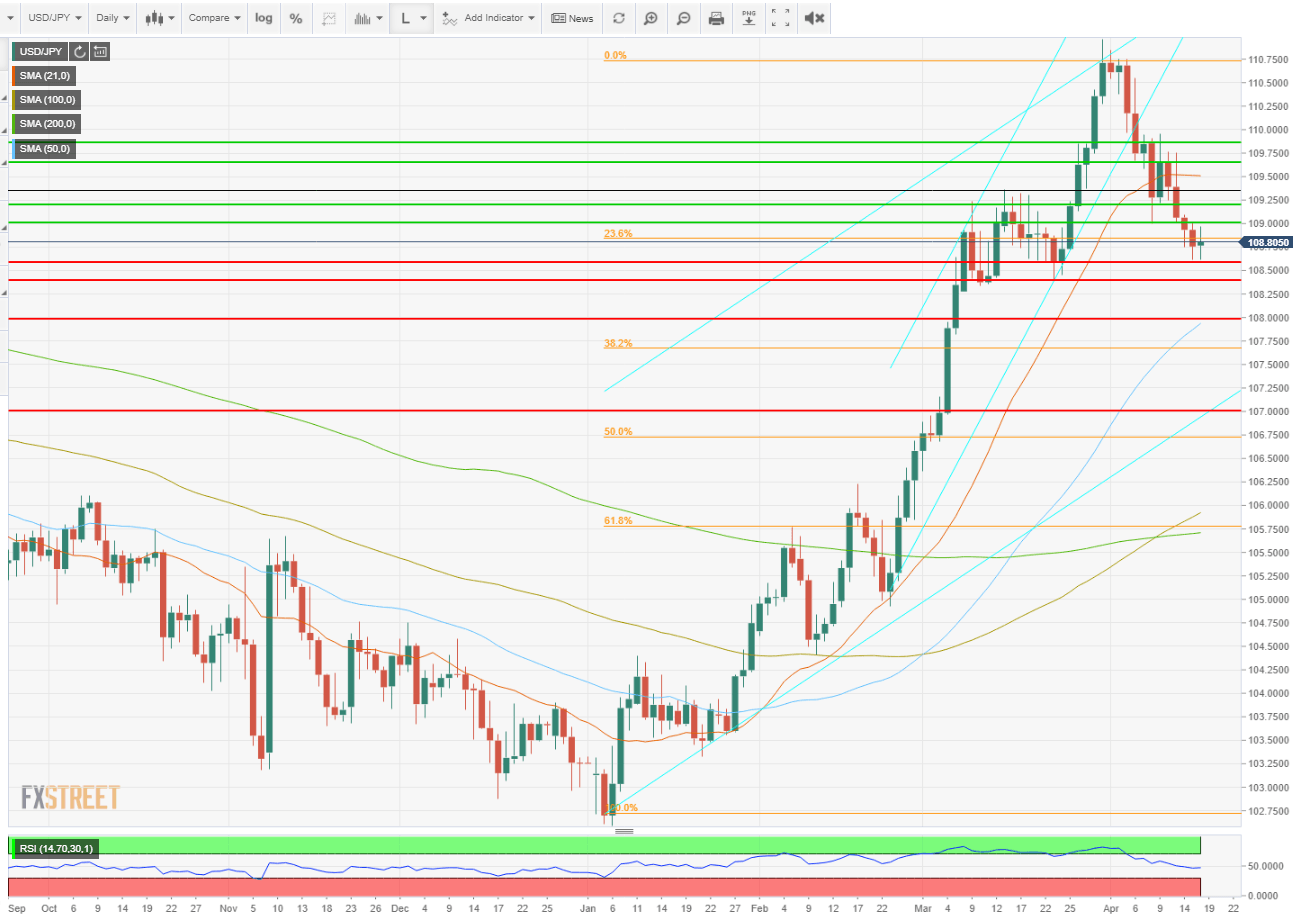

The USD/JPY consolidation from March 3 to March 24 provides support at 108.60 and 108.40. The first 23.6% Fibonacci level at 108.85 of the January 5 to March 31 run is weak resistance at 108.85, (at the time of writing the USD/JPY is at 108.82) but if the pair finishes above this level it reverts to equaly weak support.

Immediate resistance lines at 109.00 and 109.20 reflect the March 3 to 24 period.

Given the current ambivalence after the steep first quarter gains in USD/JPY and the firm base at 108.40 a consolidation above that level within the March range lies ahead.

The overall trend remains higher but a new set of US economic directives and a resumption of rising Treasury yields will be needed for the USD/JPY to move.

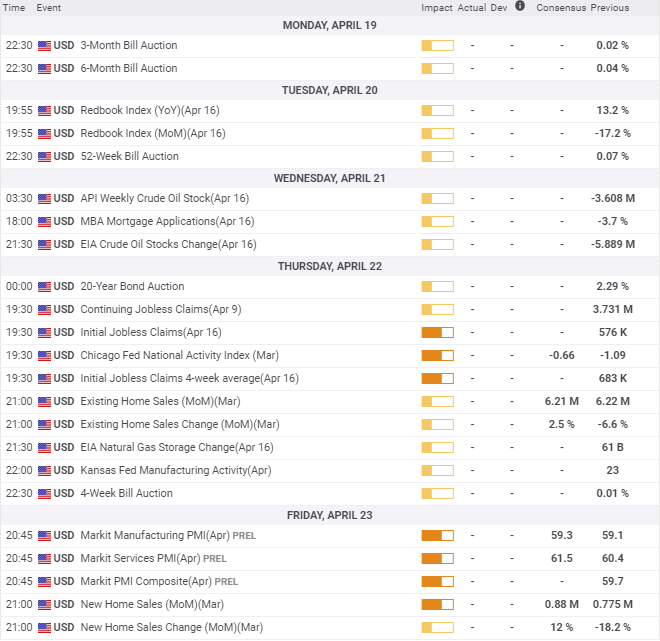

Japan statistics April 12–April 16

The jump in the annual March Producer Price Index, twice its forecast, was due to the base effect, which should continue through May. In March, April and May 2020 annual PPI dropped 0.4%, 2.5% and 2.7%. Machinery Orders, a long-time staple of Japanese exports were much weaker than expected in February and substantially lower than January.

US statistics April 12–April 16

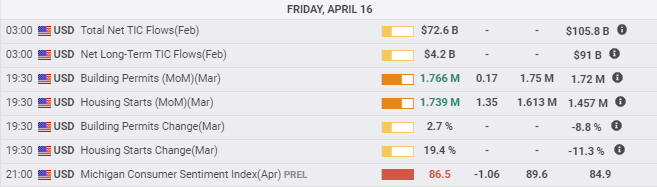

Retail Sales were the main event.The nearly10% burst in consumption was fueled by the federal stimulus payment and the confidence imbued by the excellent March labor market reported two weeks ago. Initial Claims showed good progress for the first time since November. The housing market remained very strong with both starts and permits beating forecasts in March. Industrial Production in March came in at half its estimate but was an outlier in an otherwise impressive month. Consumer inflation was higher than predicted in March, and the base effect should continue through May. With the Fed's adoption of inflation averaging last September and the many statements by Chair Jerome Powell and other officials that low rates will remain until the economy is fully recovered, price changes have ceased to motivate markets.

Japan statistics April 19–April 23

The last month of the quarter is on tap with an improvement expected in Exports but a drop in Imports. Revisions to March National CPI are expected to produce few changes with none important as is true of April Jibun Manufacturing PMI. Markets will not trade these statistics.

US statistics April 19–April 23

A thin week for US information. The housing market can be expected to remain strong in March with Existing Homes Sales, 90% of the US market, and New Home Sales, the balance, reported. Jobless Claims for the April 16 week have the most economic significance but little market impact.

USD/JPY technical outlook

Consolidation within the general March 3 to March 25 range,108.40 to 109.20 is this week's prognosis. Support and resistance levels are the product of recent trading. As noted above, Treasury rates took the USD/JPY lower, as profit-taking and a sense that the first quarter's economic strength may moderate in the second undermined both. The rising channel that dates to the New Year is intact, though the far steeper one for the February to March run, is history.

The Relative Strength Index (RSI) at 47.03 is neutral. The conclusive cross of the 21-day moving average (MA) on Tuesday after three sessions of back and forth, makes it a resistance marker at 109.50. The 50-day MA at 107.94 is a good second for existing support at 108.00. The 100-day MA at 105.92 and the 200-day MV at 105.71 are part of the range prior to March 26.

Resistance: 108.85 (23.6% Fibonacci), 109.00; 109.20; 109.65; 109.85

Support: 108.60; 108.40; 108.00; 107.67 (38.2% Fibonacci) ; 107.00

FXStreet Forecast Poll

The FXStreet Forecast Poll expects that the March range will be unable to contain the USD/JPY. The area below 108.40 has few supports over the quarter to deter penetration to the base of the large March 3 increase. This view depends on US Treasury rates. If US yields begin to rise again, they will take the USD/JPY with them.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.