USD/JPY Weekly Forecast: Treasury yields, Treasury yields and Treasury yields

- Dollar/yen climbs above 130 for the first time in two week, adds 3.1%.

- Treasury yields in the US rise sharply from six-week lows, JGB returns stable.

- US payrolls best forecast, enabling Fed policy, wages fall.

- FXStreet Forecast Poll anticipates failure above 130.00.

Reviving US Treasury yields and a tacit admission from the Bank of Japan that its accommodative policies are unchanged sent the USD/JPY flying back towards its two-decade high this week. The USD/JPY gained 3.1% in five trading sessions from Monday’s open at 127.01 to 130.96 in Friday morning New York trading.

Treasury returns in the US were higher across the yield curve with the commercial benchmark 10-year rising 20 basis points to 2.946% and the 2-year adding the same to 2.677%. Both yields had fallen to their lowest in a month-and-a-half last week. Japanese JGB rates were largely unchanged with the 10-year losing 1 basis point to 0.235%.

In a somewhat uncommon statement from an individual Bank of Japan (BoJ) board member, Seiji Adachi repeated the bank’s ultra-easy policy remained intact despite National CPI registering 2.5% in April. Japanese inflation is centered in commodities and oil, core CPI was just 0.8% in April.

Last week’s USD/JPY plunge to below 127.00 has been aided by BoJ Governor Haruhiko Kuroda’s reported admission in the Diet that a shift in the bank’s monetary policy was possible.

Data releases were dominated by the US payroll report on Friday and its impact on Federal Reserve policy. The US economy added 390,000 workers to the official job rolls in May, better than the 325,00 forecast and more than sufficient to keep Fed tightening policy in place. Wage increases for the year at 5.2% were as forecast and likely to widen the decline in consumer purchasing power when CPI is reported this coming Friday.

Treasury futures have the odds for a 50 basis point increase at the June 15 meeting at 98.5% and 91.1% for the July 27 conclave. Purchasing managers’ indexes for May were mixed with all manufacturing gauges except employment better than predicted while the measures for the service sector were uniformly weaker.

Japanese information was poor on the industrial side, with production in April considerably weaker than forecast, but better for the consumer, as Retail Trade (sales) rose for the month. Consumer confidence in May was also slightly better than anticipated.

USD/JPY outlook

Treasury yields are again paramount for the USD/JPY. The possibility of a change in the BoJ’s seemingly eternal and ineffective easy money policy, brief though it was, is an indication of its potential impact on currency values. It is possible that Haruhiko Kuroda’s observation was the first trial of a policy change and that new ideas are being debated within the bank. Was Mr. Adachi’s comment indicative of the bank consensus or an attempt to forestall a change?

Fed policy is the determinant for the USD/JPY because the BoJ effectively has no policy. It is not at all clear that US rates can continue higher given the unsettled state of the US economy but the current spread is more than enough to provide the USD/JPY with support.

The Atlanta Fed GDPNow estimate for second quarter growth dropped to 1.3% from 1.8%. Were the US to fall into recession with a retraction in GDP in Q2, it is debatable whether the Fed could continue its rate program. However, unless job creation falters in June, the window will remain open until GDP is reported on July 30, after the FOMC meeting on the 27th.

Japanese statistics in the week ahead, first quarter GDP (revision), Overall Household Spending for April and the Eco Watchers Survey for May, which assess regional economic trends will not move markets.

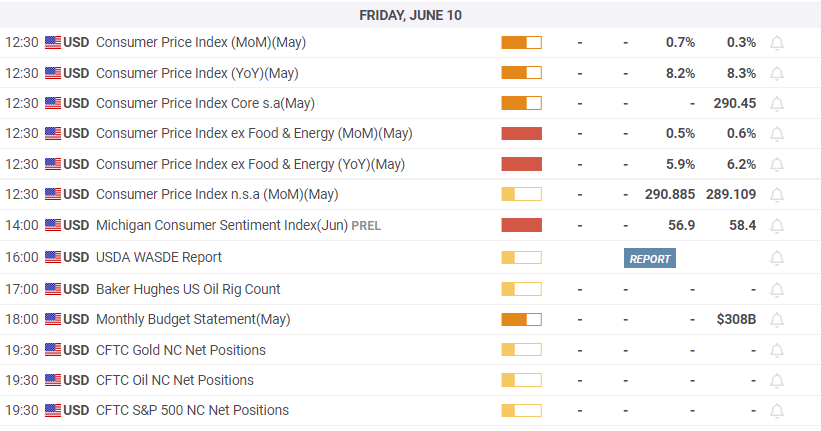

May CPI in the US, issued on Friday, is forecast to slip to 8.2% from 8.3%. For April the negative spread between CPI and annual Average Hourly Earnings (AHE) was 2.8% (8.3%- 5.5%). Earnings were 5.2% last month, every step of inflation above 8.0% increases the loss to consumer purchasing power and makes the Fed's anti-inflation campaign more imperative.

The USD/JPY outlook is higher but with limited potential for extensive gains unless Treasury yields rise above their prior highs.

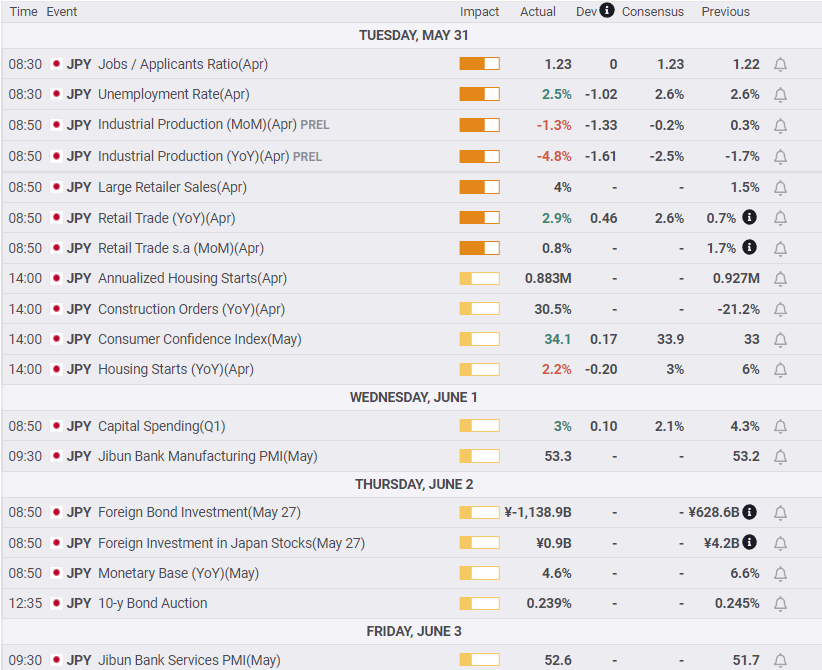

Japan statistics May 30–June 3

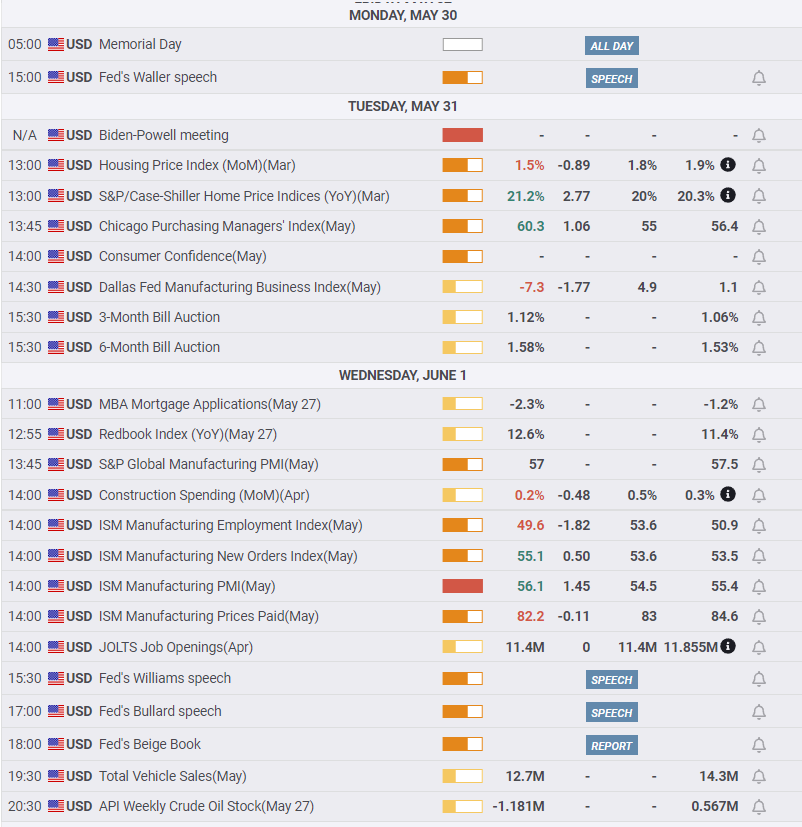

US statistics May 30–June 3

FXStreet

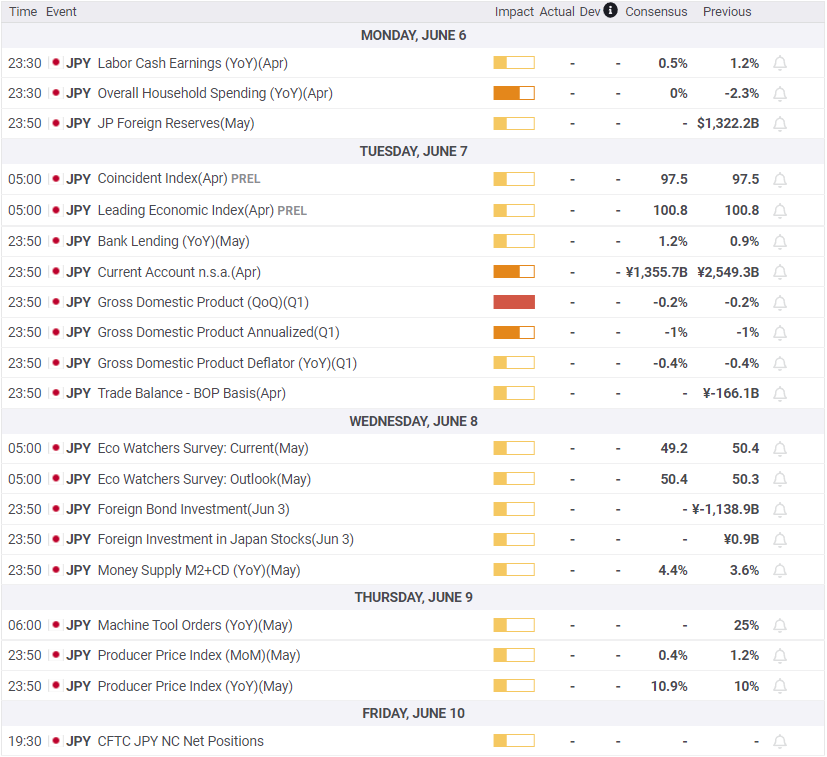

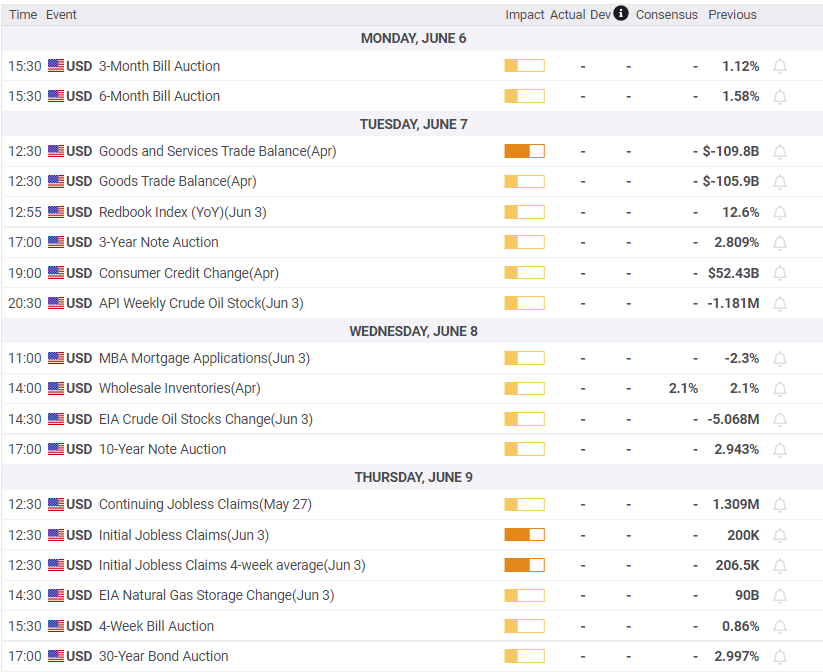

Japan statistics June 6–June 10

FXStreet

US statistics June 6–June 10

FXStreet

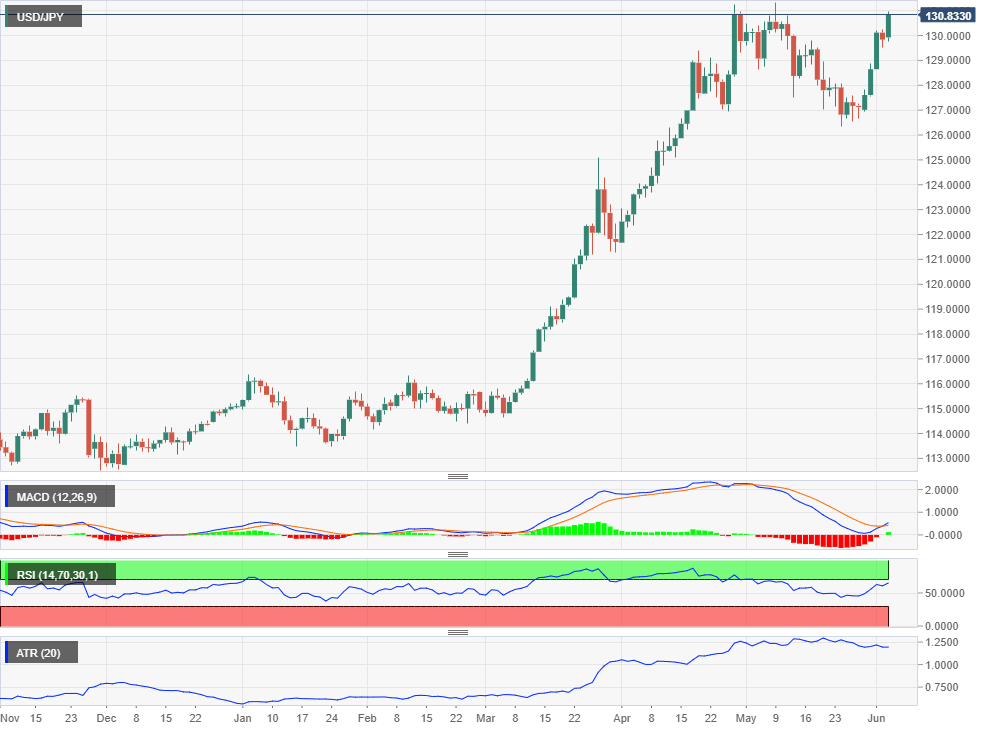

USD/JPY technical outlook

USD/JPY technical outlook

The MACD (Moving Average Convergence Divergence) price line crossed the signal line on Thursday with an incipient buy signal. The Relative Strength Index (RSI) has been rising since Monday. The qualification on both indicators is the previous inability of USD/JPY to make any permanent move above 130.80. The MACD had also crossed the signal line on April 27 but as the USD/JPY never generated any upward momentum, the buy indication was never operational. The identical situation applies now. The USD/JPY needs to close above the old high finish at 130.87 and trade above 131.35 the May 9 high, to verify the buy intention.

Average True Range (ATR) remains high, indicating as it has for the past five weeks, that the area above 129.00 is conducive to volatility.

Resistance: 130.87, 131.35

Support: 130.60, 130.00, 129.50, 129.00, 128.35

Moving Averages: 21-day 128.79, 50-day 127.38, 100-day 121.73, 200-day 117.37

Fibonacci levels (March 7 114.81-April 28 130.87): 23.6%-127.00, 38.2%-124.67, 50%-122.71

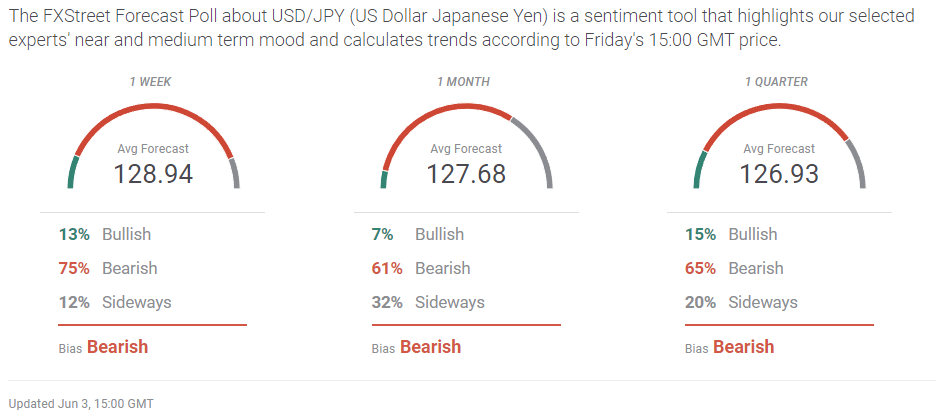

FXStreet Forecast Poll

The FXStreet Forecast Poll implies that US Treasury yeilds will not move beyond their prior highs, bringing a technical reversal to USD/JPY.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.