USD/JPY Weekly Forecast: The Fed first, nothing second

- Markets focused on possible policy shift at Wednesday’s FOMC meeting.

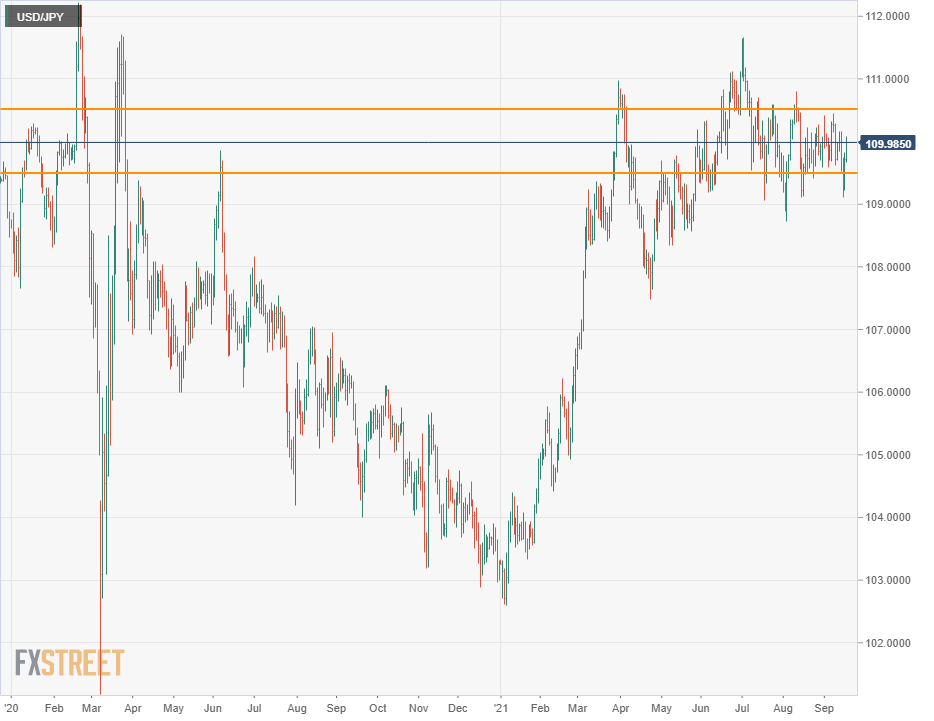

- Dollar yen maintains its three-month 109.50-110.50 range.

- US Treasury rates gain on the week after falling on Tuesday.

- Bank of Japan expected to maintain statu-quo monetary policy.

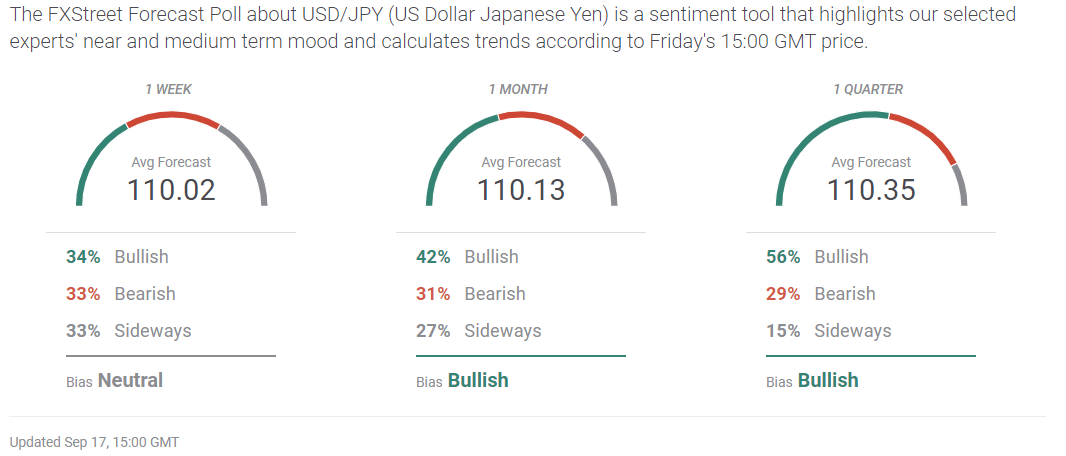

- FXStreet Forecast Poll sees minor upward movement.

The USD/JPY and Treasury yields finished the week modestly higher despite somewhat conflicting directions from US economic data.

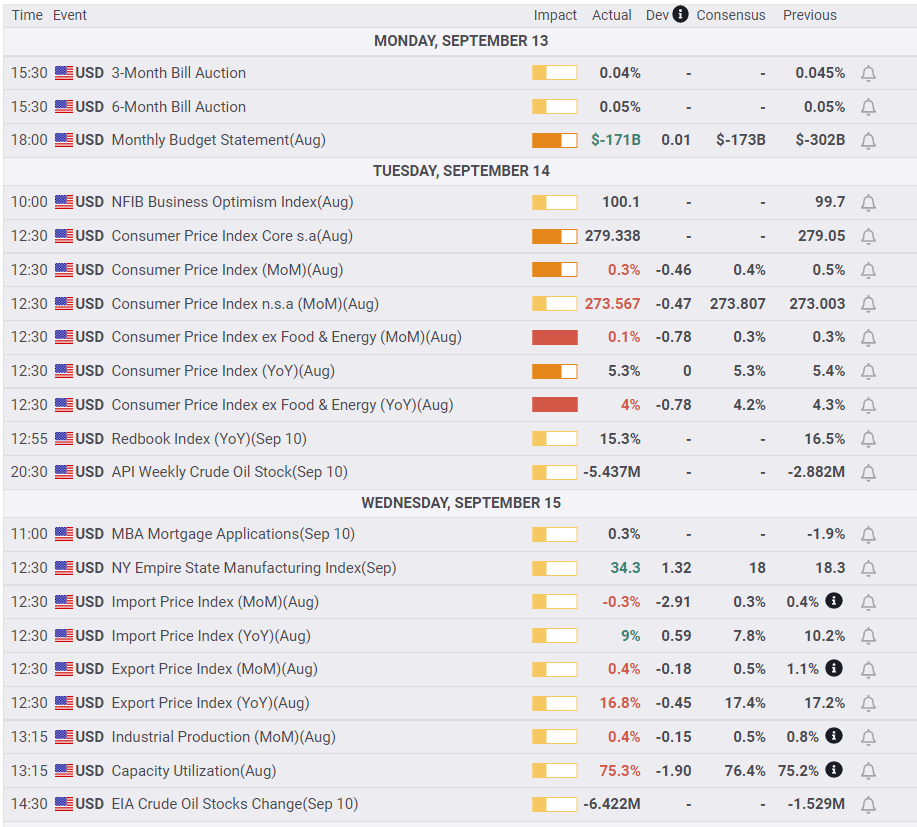

Consumer price gains in the US moderated slightly in August, giving the Federal Reserve additional logic for delaying their bond taper. The USD/JPY dropped on the Tuesday CPI release and continued lower on Wednesday to the week's low.

Retail Sales for August, issued on Thursday, had been forecast to fall for the second month. Consumer outlook in the Michigan survey had previously plunged to a decade low for the month. Instead, outside of automobile sales which have been restricted by shortages, consumers had their most avid month since January. The USD/JPY duly reversed and by Friday at 109.98 was just points above Monday’s open.

Treasury yields also rose slightly. The 10-year return opened the week at 1.340%, slipped to 1.279% after Tuesday’s CPI data and by Friday had added 3 basis points to 1.370%.

Behind the back and forth over US statistics is the pending policy decision from the Federal Reserve at the end of its two-day meeting on Wednesday.

In August, Chair Jerome Powell said that a reduction in its $120 billion a month of bond purchases was likely before the end of the year. When he made that statement, Nonfarm Payrolls (NFP) had averaged over one million new jobs in June and July. Another strong month was expected to follow. August’s disappointment, missing the consensus forecast by more than 500,000, demolished the near certainty that the Fed would announce its taper schedule at the September meeting.

The weak hiring last month is a bit of a puzzle. There are almost 11 million unfilled jobs in the United States. With about 6 million people thought to be still unemployed and extended federal jobless benefits expiring in September, many were expected to return to work.

Federal Reserve policy, as enumerated many times by Chair Powell, has focused almost exclusively on restoring the labor economy to its condition before the pandemic. Inflation has been relegated to secondary status by the adoption of inflation-averaging last September.

There are three more Federal Reserve Open Market Committee (FOMC) meetings this year, September 22, November 3 and December 15. Having promised a change in the bond policy by the end of the year there is no pressing need to announce the details at next week’s meeting.

Has the August NFP provided the necessary caution? Judging from the non-committal attitude of the markets, a renewal of the year-end promise without details seems the most likely outcome.

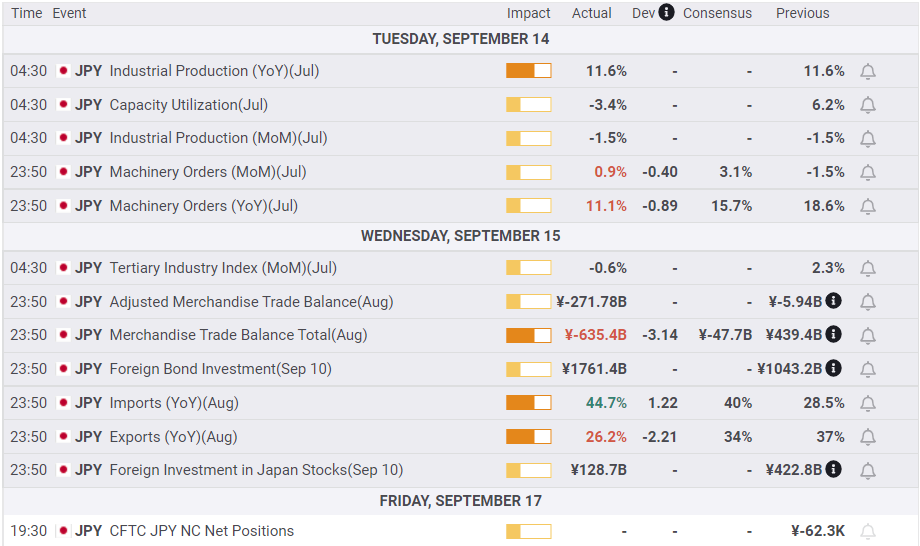

Japanese data produced no major surprises. Industrial Production in July was higher on the year but slipped on the month. Exports in August were weaker than forecast but imports were higher.

USD/JPY outlook

The week ahead culminates early with the US Federal Reserve meeting on Wednesday. Until then markets will remain quiet.

If the Fed announces its taper schedule, the USD/JPY and Treasury yields will rise. The size of the increases depends on the details of the timing and amount. For the USD/JPY 110.00 should be in easy reach. The 10-year yield could stretch towards 1.50%.

If Mr. Powell repeats the year-end promise but declines to specify the contents, the upward bias will be reinforced but major movement will be contingent on US data.

In the unlikely event that Mr. Powell withdraws the taper promise, dramatic falls in the USD/JPY and Treasury yields would be close to instantaneous.

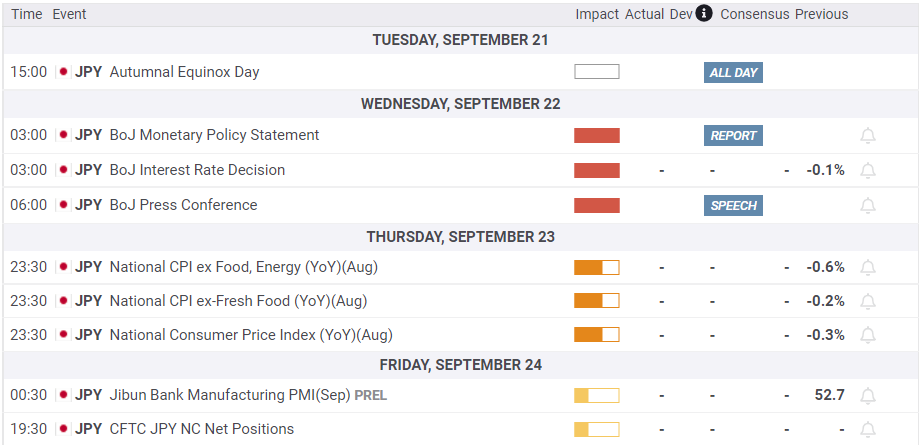

The Bank of Japan (BOJ) meeting this Wednesday is not expected to produce any policy changes. Governor Harukiko Kuroda’s comment this week that the bank could further relax monetary policy if necessary, evinced no market response. That is a rather telling judgement on the BOJ’s effective policy options, few to none, and their potential economic impact, also little to none.

Japan’s National CPI on Thursday will be an afterthought though it should confirm the return of deflation.

In the US the housing market is on tap with Existing and New Home Sales expected to report active turnover with the price gains the most pertinent information.

Japan statistics September 13–September 17

US statistics September13–September 17

FXStreet

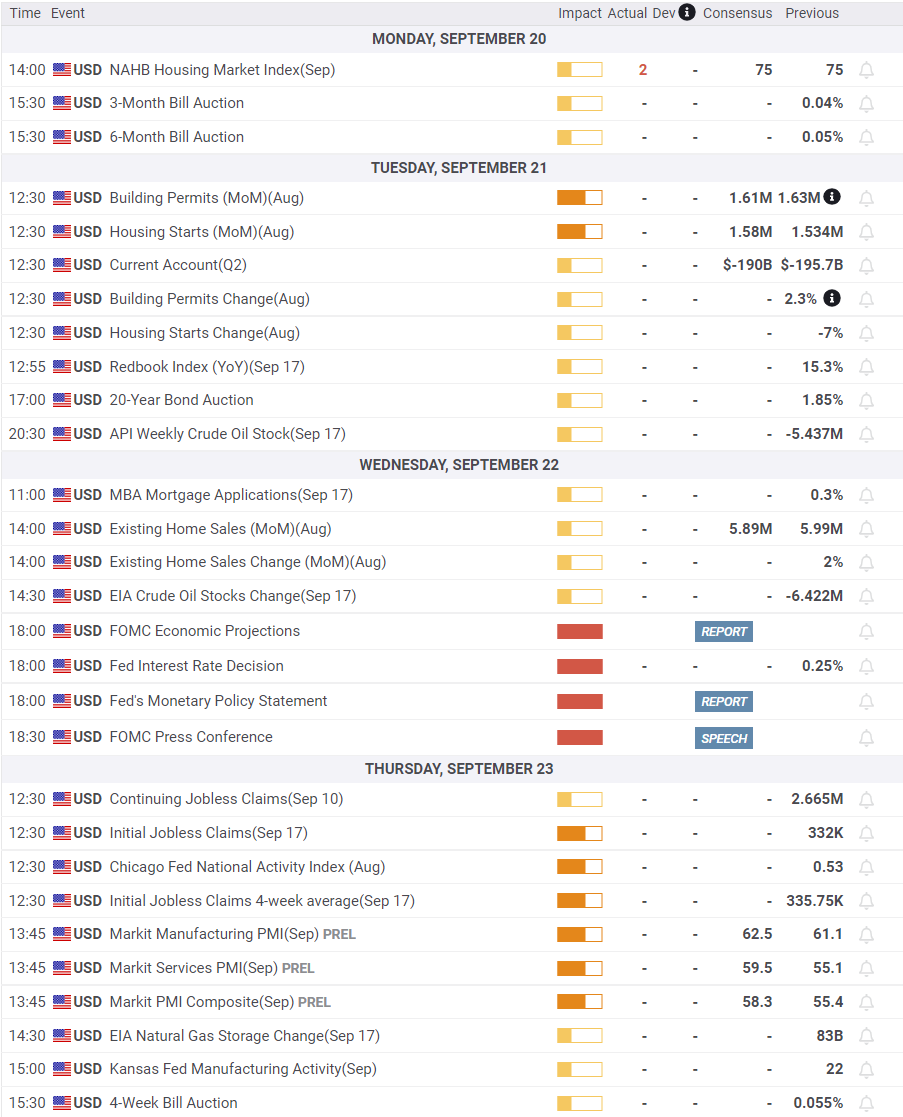

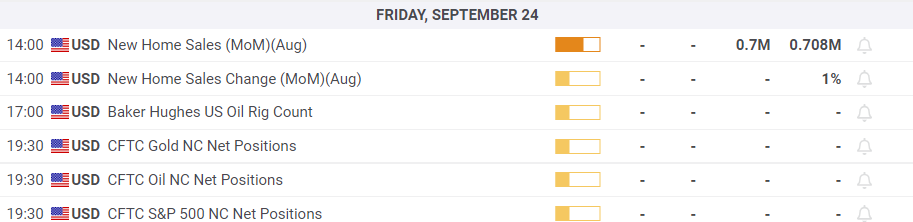

Japan statistics September 20–September 24

FXStreet

US statistics September 20–September 24

USD/JPY technical outlook

Neutrality and fading momentum are to be expected when the USD/JPY ended the week at the center of its three-month range. The MACD (Moving Average Convergence Divergence) recovered from a brief flirtation with selling but found no new interests. The Relative Strength Index (RSI) was flat after a limited spell below 50. True Range had a short and weak increase of momentum with Tuesday's and Wednesday's nearly identical fall and recovery but the subsided. There is no technical momentum evident in these indicators.

The highly unusual circumstance of three moving averages (MA) within10 points of each other just below the market is as clear an indication as possible of the USD/JPY's lack of direction. The 21-day MA is at 109.88, the 50-day MA is 109.90 and the 100-day is at 109.85. The USD/JPY closed at 109.95 on Friday, one point from where it opened the week.

Resistance:110.10, 110.30, 110.50, 110.70, 111.10

Support: 109.85-90 (MA: 21-109.88, 50-109.90, 100-109.85), 109.70, 109.50, 109.20, 109.00

The technical structure, close and frequent, and the clustered moving averages, are indicators that the USD/JPY is ripe for a move. The most likely catalyst is the FOMC meeting on Wednesday.

FXStreet Forecast Poll

The FXStreet Forecast Poll highlights the strength of the USD/JPY technical support.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.