USD/JPY Weekly Forecast: Have US Treasury rates been unleashed?

- Federal Reserve delays taper, Powell says necessary conditions met.

- US Treasury rates rise after Wednesday's FOMC meeting.

- Taro Kono expected to be new Liberal Democratic Party head.

- General elections to be held before November 28.

- BOJ leaves rates, stimulus programs unchanged.

- FXStreet Forecast Poll bullish aspect fades at one month.

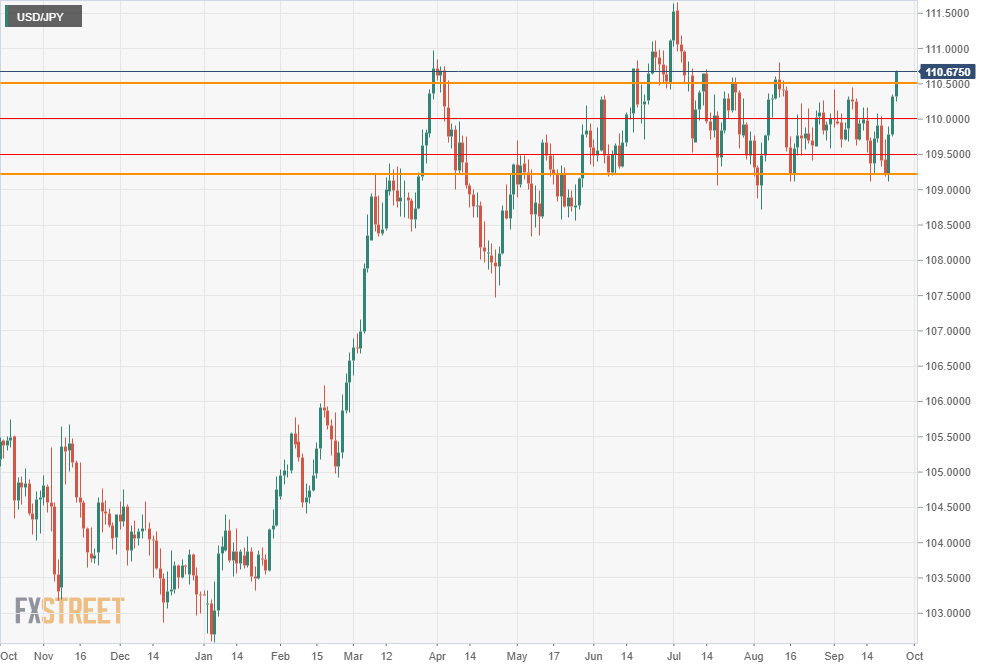

The Wednesday to Friday run from 109.23 to 110.69 in the USD/JPY neatly traversed the complete 109.20-110.50 range of the last three months. Resistance at 109.50 and 110.00 was breached in quick succession. Prior to Thursday, 110.00 had blocked all attempts over the last two weeks to take the USD/JPY higher.

On Thursday, Beijing told China’s heavily-indebted property developer Evergrande to pay its dollar-denominated debt and avoid default. The instructions calmed global equity markets and released the immediate risk-aversion flight to the yen.

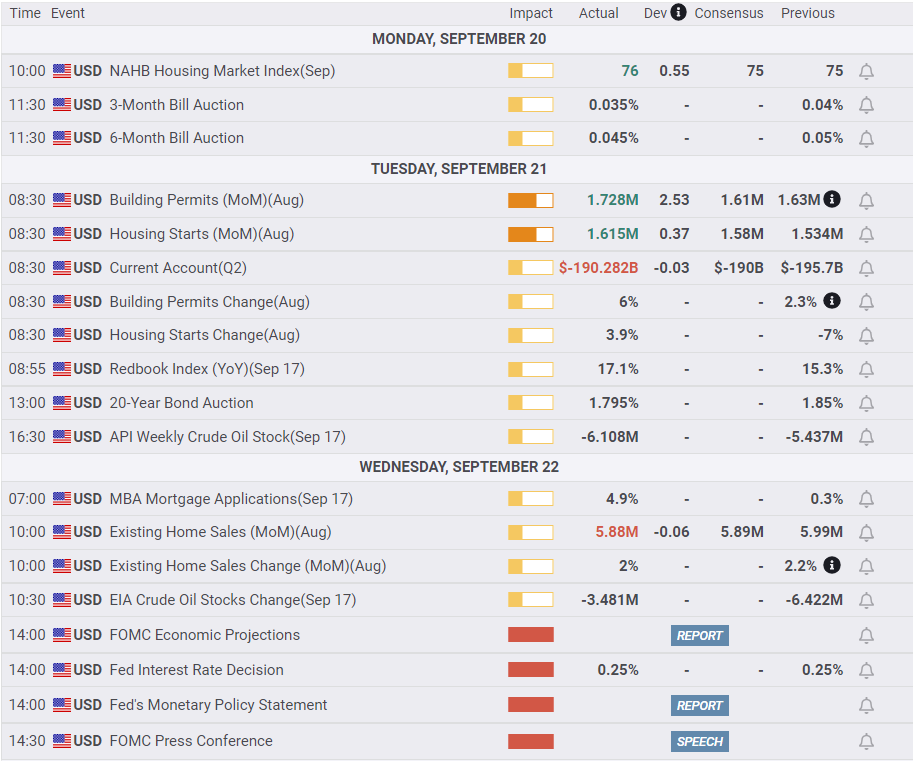

Treasury yields in the US took a sharp jump after Fed Chair Jerome Powell’s surprisingly aggressive prognosis on the taper and the bank’s own forecast for a fed funds rate hike next year.

The US 10-year Treasury yield added 12 basis points from Monday to Friday’s close at 1.42%, with 10 of those points coming on Thursday. It was the highest for this benchmark debenture since July 1 and the biggest one-day jump since February. The yield on the 30-year bond rose 9 basis points to 1.935%. The 2-year return climbed 4 basis points to 0.259% as the yield curve steepened considerably with the gains at the longer end proportionally greater.

In contrast, the Bank of Japan (BOJ), which also met on Wednesday, seems as far as ever from a change in policy. Officially, the bank renewed its base rate at -0.1%.

The contest for the head of the ruling Liberal Democratic Party (LDP) seems likely to be won by 58-year old Taro Kono, current vaccination minister and former holder of the defense and foreign affairs portfolios. Mr Kono is fluent in English and has lived and worked in the United States and Singapore. In second place in a poll of LDP members, but far behind, is Kishida Fumio, another past foreign affairs minister. The nearly complete dominance of Japan’s political system by the LDP virtually guarantees that its leader and candidate will win the national elections that must be called by November 28 this year.

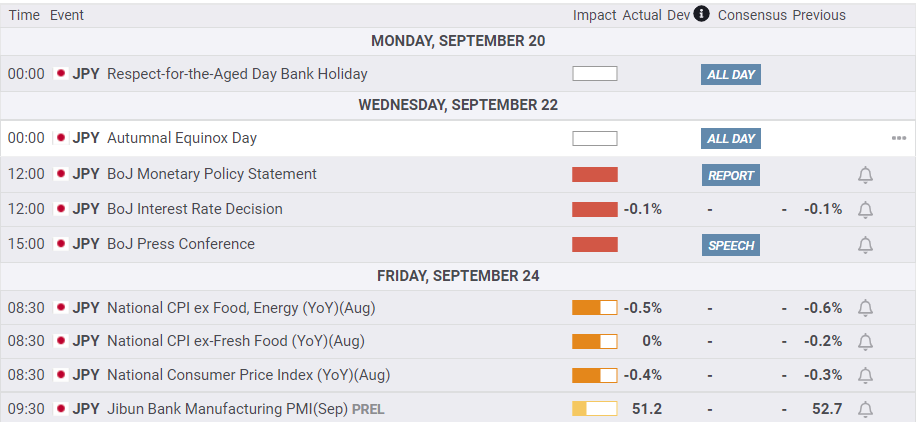

Price measures in Japan stretched deflation to 13 months. The National Consumer Price Index (YoY) slipped 0.4% in August and the core rate was off 0.5% on the year.

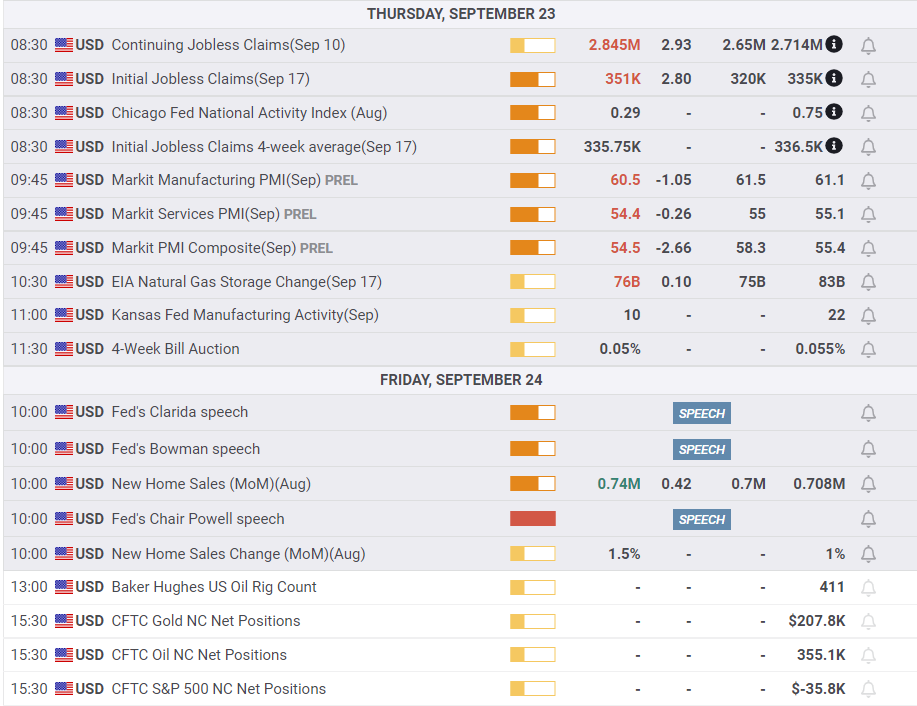

In the US, the Wednesday Fed meeting dominated news and prompted a revival of Treasury rates in the second half of the week. Stocks recovered from their China-inspired Monday sell-off, returning to last week’s level by Friday. Existing Home Sales, 90% of the US market, performed as expected in August. Initial Jobless Claims rose for the second week in a row. Neither affected markets.

USD/JPY Outlook

The post-Fed surge in US Treasury rates and the relaxation of China’s Evergrande fears have given the USD/JPY decided upward bias.

Treasury rates continued their rise on Friday after Fed Chair Powell observed that most of the Federal Open Market Committee (FOMC) members thought the conditions for a bond taper had been met. He added, tellingly, that this was his opinion as well.

The pending Japanese election and the new Prime Minister will produce another in the endless series, going back two decades, of government stimulus packages. It will not stimulate the economy, but it will highlight the structural weaknesses in Japan and undermine the yen.

The US will continue to outperform Japan and the gradual subsidence of the pandemic as a inhibiting factor will assist the more flexible American economy.

Japanese Retail Trade (sales) for July will be noted as the consumer has been a reluctant participant in the recovery, but it is too retrograde to impact markets. Industrial Production for August has more bearing but also little potential impact. The Tankan Report for the third quarter should confirm the weak state of Japanese manufacturing and non-manufacturing industries without adding any forward knowledge. Consumer Confidence for September is expected to remain moribund.

US data begins with Durable Goods Orders for August, essentially a restatement of the Retail Sales figures with the important exception of the Nondefense Capital Goods Orders, a much followed proxy for business investment. The manufacturing Purchasing Managers’ Index will shed insight on whether the factory sector is surmounting labor and material shortages and price inflation. A positive assessment will support the dollar.

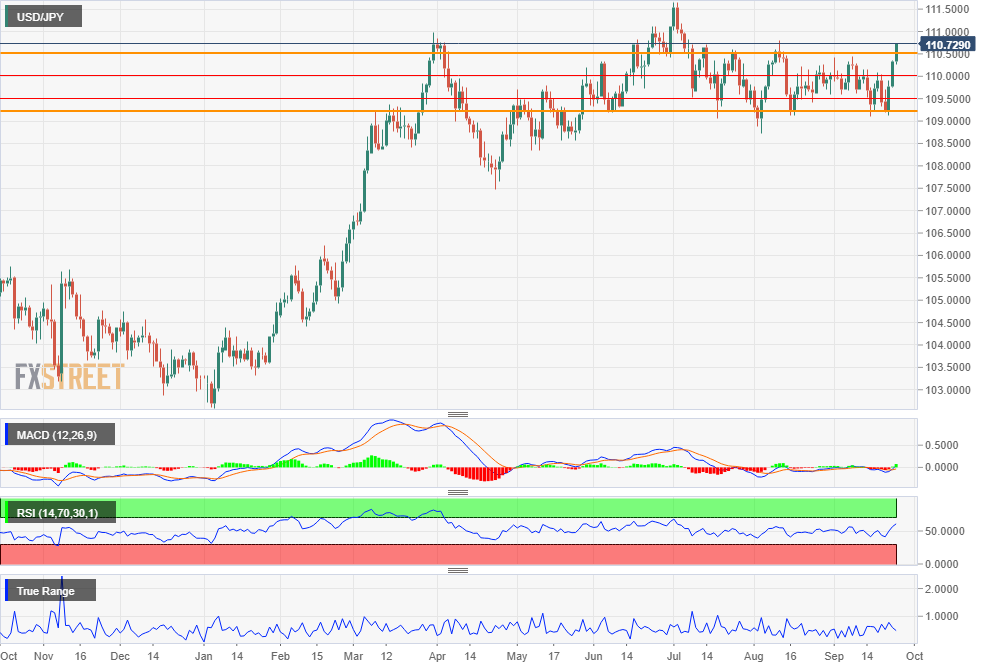

The range inertia at 110.50 was of considerable duration, but it was broken on Friday without fanfare. Resistance at 111.00 is far less important and beyond that are only the brief panic points of February and March 2020.

As long as the US Treasury market is not detained by Fed temporizing, rising US rates should propel the USD/JPY higher.

Japan statistics September 20–September 24

US statistics September 20–September 24

FXStreet

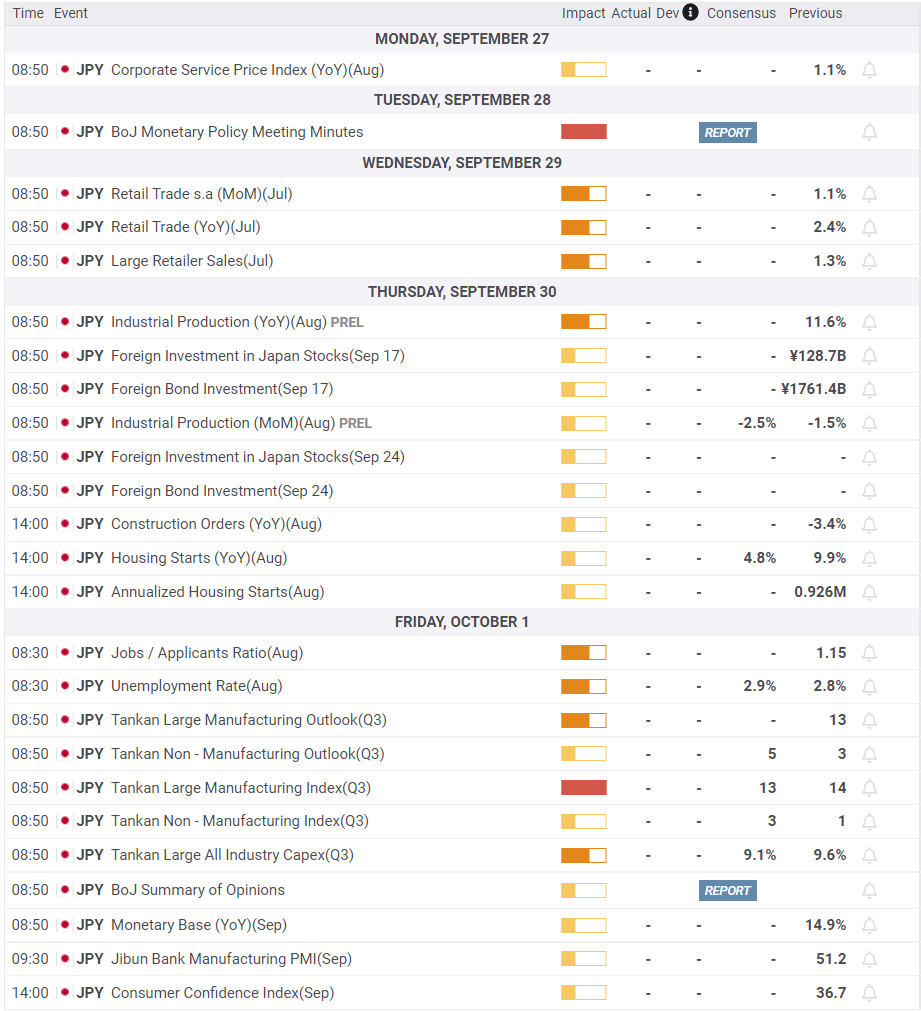

Japan statistics September 27–October 1

FXStreet

US statistics September 27–October 1

FXStreet

USD/JPY technical outlook

The MACD (Moving Average Convergence Divergence) and Relative Strength Index (RSI) moved decisively into positive territory on the post-Fed climb in the USD/JPY. True Range peaked with the reversal on Wednesday but remains in the upper half of the last month's readings.

The cluster of the 21-day, 50-day and 100-day moving averages (MA) within three points at 109.88, 109.87 and 109.89, is a strong positive signal, in addition to being solid support. The cross of these then resistance lines on Thursday was a major technical factor in releasing the USD/JPY up to and through the next resistance line at 110.50. Technical momentum is clearly higher.

The heavy balance of support over resistance favors a continued USD/JPY ascent.

Resistance: 111.10, 111.55, 111.70

Support: 110.50, 110.35, 110.00, 109.88 (21-day, 50-day, 100-day MA), 109.80, 109.25, 109.00

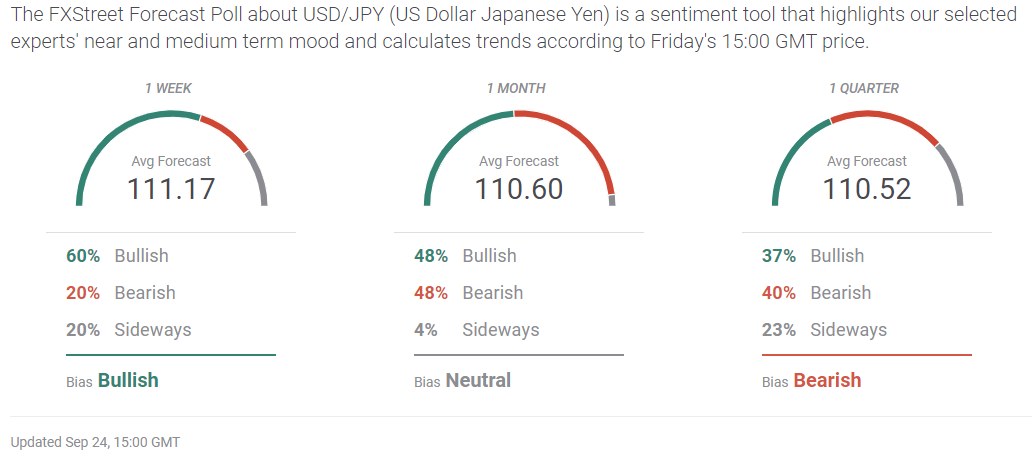

FXStreet Forecast Poll

The FXStreet Forecast Poll prediction for an immediate move above 111.00 fades to neutral after one week.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.