USD/JPY Forecast: Powell in play after politics pull the pair down

- The USD/JPY dropped back down on political issues in both the US and Japan.

- Powell's first rate decision is left, right, and center with a focus on the future.

- The technical picture remains negative for the pair once again.

White House Reshuffling, mixed data, and Moritomo

US President Donald Trump remains in the headlines. A week after his Chief Economic Adviser Gary Cohn resigned, the President nominated Larry Kudlow, a TV personality like Trump. While Kudlow worked in the Reagan Administration and supports free-trade, his fresh criticism of China puts him closer to the protectionist views of the President.

Greater worries came from the ousting of Secretary of State Rex Tillerson. The so-called "Rexit" rattled markets and weighed on the US Dollar and stole the show from the inflation report that came out at the same time. There are reports that National Security Adviser H.R. McMaster and White House Chief of Staff John Kelly are also on the way out. Another news story that Special Counsel Robert Mueller has subpoenaed documents from the Trump Organization also made waves.

The inflation report mentioned earlier came out exactly as expected. Core CPI remains at 1.8% YoY, and the pace slowed down to 0.2% MoM in February. On the other hand, US Retail Sales fell short of expectations with a drop of 0.1% and the Control Group rose by 0.1%, also below forecasts.

Late in the week, upbeat data supported the US Dollar: Industrial Output rise by 1.1%, JOLTs job openings topped 6.3 million annualized and the University of Michigan's Consumer Sentiment Index jumped to 102, above 99.3 that was expected. The inflation component of that report also helped. The greenback made a comeback.

In Japan, the Yen strengthened on the Moritomo scandal. A cheap sale of land to a school in which the wife of PM Abe is involved implicated FinMin Taro Aso, and he will skip the G-20 gathering. The alleged forgery of documents has sent the popularity of the government down, risking the stimulus policy that pushed the currency lower. This fear drove the Japanese currency higher.

Fed Focus: more than a hike

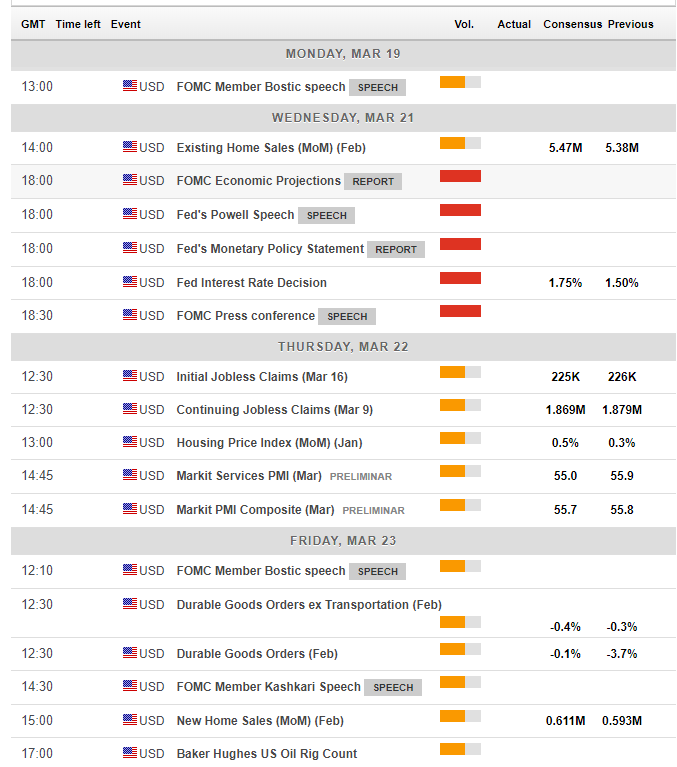

The main event in the upcoming week is undoubtedly the Fed decision. A rate hike is all but certain in the first FOMC meeting presided by Jerome Powell. The focus is on the next moves: will the Fed raise rates three times in 2018 as previously forecast in the dot-plot? Or will they upgrade their assessment to four hikes? This is the central question.

The Fed released the statement and a new dot-plot alongside new forecasts. Afterward, Powell will hold his first press conference, and it may differ from the tone of the statement and the dot-plot. This may provide an opportunity.

See: Fed Preview: Dollar-friendly dot-plot before a Powell punishment?

Apart from the Fed decision, Existing Home Sales on Wednesday and New Home Sales on Friday will provide another view of the housing sector after Building Permits, and Housing starts fell short of expectations. Durable goods orders on Friday and especially the ex-defense ex-air component, serve as the primary economic figure and they feed into Q1 GDP. However, the Fed is left, right, and center.

Here are the top US events as they appear on the forex calendar:

Japan: Aso and Abe are cornered

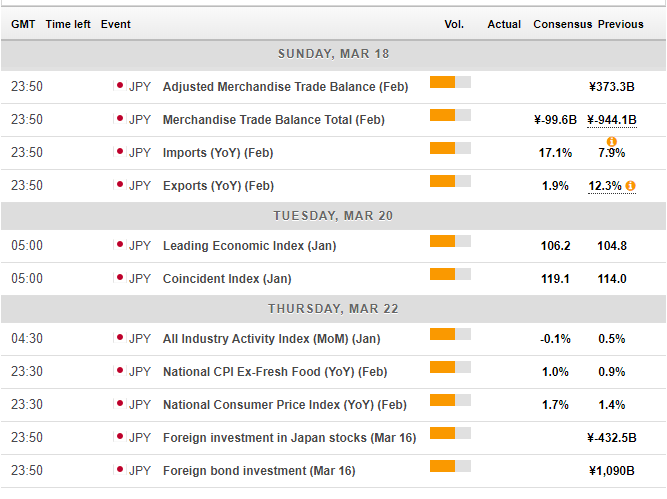

The Japanese yen will move mostly on the ongoing Moritomo scandal in Japan. If FinMin Aso is forced to quit, the Yen could gain further strength. A Japanese government in turmoil will find it harder to resist safe-haven flows. If PM Shinzo Abe is forced to quit, the political uncertainty and fears will push the yen even higher on safe-haven flows.

Apart from that, the Trade Balance and the National Inflation figures are of interest, but a significant immediate market reaction is unlikely.

Here are the events lined up in Japan:

USD/JPY Technical Analysis: Bearish bias

The USD/JPY had already overcome the downtrend resistance line, but the pair is still battling this level and dipped below it once again.

The RSI continues pointing to the downside, situated well below 50 but also keeping a safe distance from 30, therefore not in oversold territory. Momentum leans lower.

¥105.90 was a low point twice in early March and separates ranges. The February 16th low of ¥105.55 is still relevant after another test. The 16-month of ¥105.25 follows closely before the round line of ¥105.00.

Looking up, the March 6th high of ¥106.50 caps the pair. Further above, ¥107.30 capped the pair on March 13th and was a low point in September 2017. ¥107.90 was the high point on February 21st.

-636568085777827074.png)

What's next for USD/JPY?

The Fed is unlikely to be too hawkish: any upgrade by the Fed could be watered down by Powell. Moreover, a weaker Japanese government may find it hard to enact further stimulus nor verbally intervene to weaken the yen. All in all, there is room to the downside.

Examining the FXStreet FX Poll shows a bearish sentiment in the near term, in line with the sentiment expressed here.

Author

Yohay Elam

FXStreet

Yohay is in Forex since 2008 when he founded Forex Crunch, a blog crafted in his free time that turned into a fully-fledged currency website later sold to Finixio.