USD/JPY Forecast: A quiet week may be a prelude to risk recovery

- USD/JPY closed at par for the week and the month.

- Risk aversion has ebbed but risk appetite has not yet returned.

- The enormous addition to global dollar may begin to undermine USD/JPY.

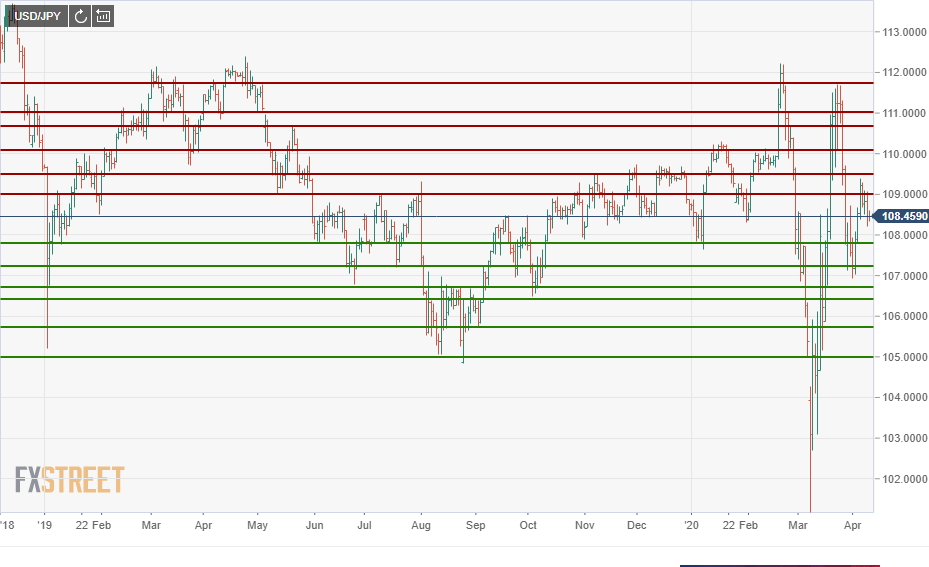

If you didn’t know that the last six weeks have been a time of pandemic and panic you might not realize it if you checked the USD/JPY closing rates. On March 2 the pair closed at 108.53. Six weeks later on Friday April 10 the USD/JPY finished at 108.46. Concealed by those endpoints is a more than ten figure range and a trough to peak ascent of 10% in just two weeks.

Friday’s close puts the USD/JPY at about the mid-point of its trading for the past ten months.

Over the past several weeks risk aversion flows to the US dollar have won out over two other streams that would normally undermine dollar strength. First the Federal Reserve provided a massive flood of dollars to the global financial system to keep it running smoothly as safe have demand for the US currency soared in the early weeks of the viral crisis. Second the central bank has directed a torrent of liquidity at the American economy first through asset purchases of $700 billion and then with a $ 2.3 trillion loan program for state and local governments and firms to help them fight the economic dislocation caused by widespread closures of businesses and the enormous job losses they have caused.

Japan’s own stimulus, a record a 108.2 trillion yen ($992 billion) is less than one-third of what the Fed alone is doing and that does not include the federal government’s own support program of more than $2 trillion passed by Congress and signed by President Trump.

Japanese statistics April 6-10

Japanese economic data for February, though passé now, was better than expected. Overall household spending on the year fell 0.3% much less than the -3.9% predicted and was the best reading in five months. The Coincident Index which rates the overall condition of the economy rose to 95.8 from 95.2 s and the Leading Economic Index rose to 92.1 from 90.5 in January. Machinery orders climbed 2.3% on the month, much better than the -2.7% forecast and on the year they fell 2.4% less than the -2.9% indication.

The March numbers were a different order. Consumer confidence in March plummeted to 30.9 from 38.4 in February for its worst reading since the 2009 recession. The Eco Watchers Survey Outlook Index which measures regional economic trends fell to 18.8, far beneath its 38.1 estimate and February’s 24.6. It was the lowest score since January 2009. The current conditions Index plunged to 14.2 from 27.4, the lowest reading on record for this series which started in August 2001.

USD/JPY outlook

As the risk trade to the USD/JPY begins to subside the pair will begin to feature the emerging competition between the economic prognosis for the United States and Japan and the ocean of dollars washing through the global financial system. The tendency for the dollar supply to run ahead of demand in the weeks ahead may well drag the pair lower, but the economic comparison is bound to favor the US. The timing of the recovery in the States will determine the immediate fate of the USD/JPY. The assumption being that the pandemic holds no more surprises for the world's economy.

After the wide ranges of the past six weeks there are plentiful well-traded support and resistance lines that, in the absence of fundamental developments, will help order market action.

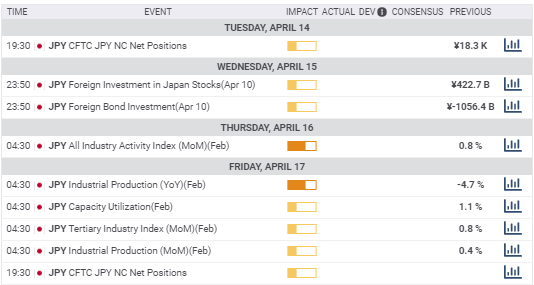

Japanese statistics April 13-17

Thursday

The All iIdustry Activity Index for February which captures change in production by all Japanese industries: January was 0.8%

Friday

Industrial production for February: January was 0.4% m/m and -4.7% y/y. Tertiary index for February which tracks the domestic service sector: January was 0.8%.

Japanese statistics conclusion

As more data for March has becomes available the outlook for the Japanese economy will continue to erode. April's results will be worse and with consumer confidence and the Eco Watchers current and outlook indexes already at decade lows in March the statistics will act to counter the trading strength the yen may have gained from the global dollar surplus.

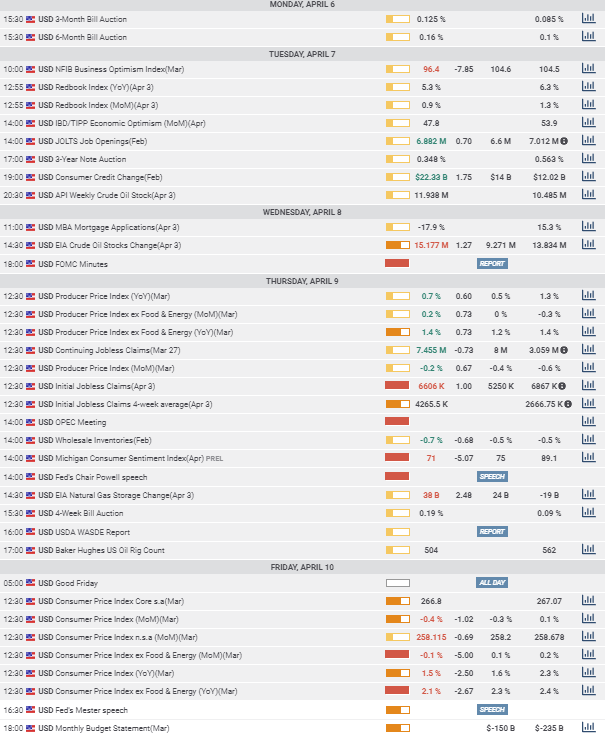

US statistics April 6-10

Tuesday

Redbook Index Y/Y for the week of April 3 dropped to 5.3% from 6.3% and 9.1% the two prior weeks.

JOLTS jobs openings were 6.882 million in February down from 7.012 million in January and a bit of nostalgia for the pre-virus labor market.

Wednesday

The FOMC minutes from the emergency March 15 meeting added little to the Fed’s public explanations for its recent actions with no specific mention of financial market stresses.

Thursday

Initial jobless were worse than expected in the April 3 week, 6.606 million vs 5.256 and followed a revised record in the prior week at 6.867 million from 6.648 million. Continuing claims rose to 7.455 million surpassing the previous financial crisis record of 6.883 million on June 27, 2009.

Friday

Consumer prices fell 0.4% in March after February’s 0.1% increase and annual gains dropped to 1.5% from 2.3%, -0.3% and 1.6% had been forecast. Core rates fell to 2.1% on the year from 2.4% and to -01% from 0.2% on the month.

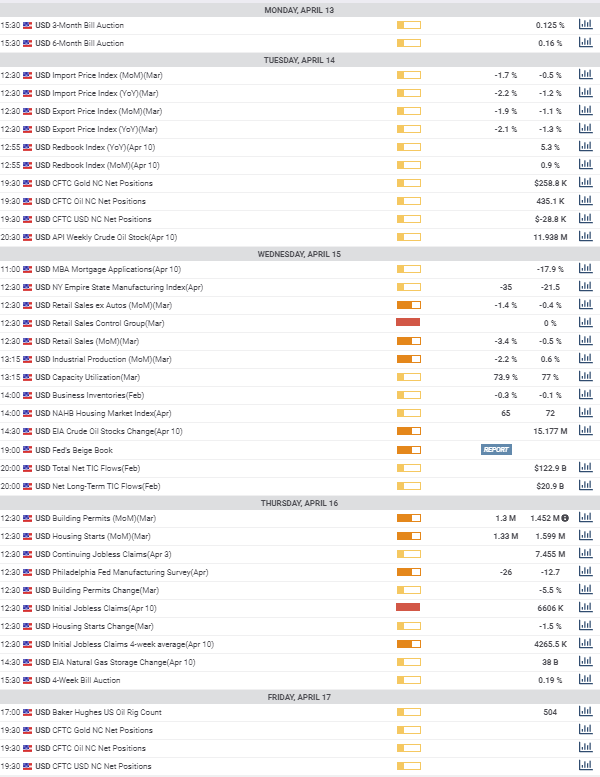

US statistics April 13-17

Wednesday

Retail sales for March will give the first substantive view of the consumer impact of the job losses. Overall sales are expected to fall 3.4% after February’s 0.5% drop. Ex-autos should fall 1.4% from -0.4%. The control group was flat in February.

Industrial production is slated to decrease 2.2% in March; it rose 0.6% in February.

The Fed’s Beige Book assessment of the US economy prepared for the April 28-29 FOMC meeting will deploy the bank’s careful language in its anecdotal description of the catastrophe that has overtaken the US economy.

Thursday

Initial jobless claims. After three weeks of record job losses with almost 17 million new claims market will be looking for any sign that firings are easing.

US statistics conclusion

The detailing of the collapse of the labor market from record performance to debacle in three weeks was the only statistic that mattered this past week. Though its power to shock markets into risk-aversion positioning has diminished.

In the week ahead March retail sales will bring the wider economic implications for the consumer driven US economy into focus. A much worse than expected figure will suggest the same for April and US GDP in the first and second quarters. With estimates for economic growth in the first three months having dropped from 3.1% to 1% in the Atlanta Fed model and for April, May and June varying from -5% to -20% and lower, retail sales figures tending to confirm the larger loss projections could bring the risk trade back to prominence and return support to the US dollar.

USD/JPY technical outlook

The relative strength index (RSI) was stationary for the week at neutral from the negligible change in the USD/JPY open to close.

The moving averages are also nearly flat. The 21-day reflecting the stable open and close on the week and the 100-day and 200-day averages showing the negating moves of the past six weeks which have ended essentially at the midpoint of the past 10 months.

Resistance: 109.00; 109.50; 110.05; 110.70; 111.00; 111.75

Support: 107.80; 107.20; 106.70; 106.40; 105.70; 105.00.

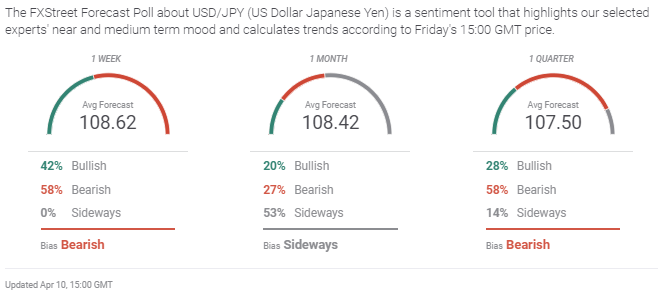

USD/JPY sentiment poll

The retreat of the safe-haven trade which started in last week's sentiment poll, even if it is not evident in the range for the week, has moved into the one week view now flipped to bearish at 42% to 58%. The one month outlook shows the uncertainty that the competing strains of pandemic, dollar supply and economic contraction have fostered. The strongly bearish one quarter view is probably due to reversion on USD/JPY collapse in the second and third weeks of March than to any prospective recovery in the Japanese economy.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.