US Retail Sales Preview: Labor Market Rules

- Retail sales expected to cool substantially in April from a robust March

- Control group had the best three months in five years, equal to the best since 2005

- Labor market and wages remain expansive

The US Census Bureau will issue its Advance Monthly Sales for Retail and Foods Services for April at 8:30 am EDT. 12:30 pm GMT on Wednesday May 15th.

Forecast

Retail sales are projected to decline sharply in April to 0.2% from the March reading of 1.6%. Sales excluding automobiles are expected to rise 0.7% following March's gain of 1.2%. The control group, sales minus building materials, motor vehicles and parts and gasoline and food service receipts is predicted to gain 0.4% after the 1% increase in March.

Retail Sales and economic growth

The US economy’s 3.2% GDP performance in the first quarter softened concerns that the 2% decline in growth from 4.2% in the second quarter to 2.2% in the fourth was evidence that the administration’s tax and spending package had only provided a temporary lift to the economy.

Following the reporting confusion surrounding the government partial closure in January the accuracy of several statistics was uncertain. The retail sales and control group numbers from December which reported huge declines were discounted as the Census Bureau admitted data collection problems. Some of December’s sales were most likely included in the January figures helping to give the first quarter better numbers than might have otherwise been the case.

The control group’s three month moving average in March at 0.8% equaled the best in 14 years and the overall sales average was the highest since December 2017.

Business sentiment figures from the Institute for Supply Management for services and manufacturing slipped sharply in January. Both recovered in February but March and April scores are at the lower end of the post-election range though still well above the 50 division between expansion and contraction.

It is as yet unclear if the drop in business sentiment reflects an empirical change in the US economy or is a moderation from the elevated sentiment of 2018.

The current reading on second quarter GDP from the AtlantFed GDPNow model is 1.6%. The model will recalibrate after the retail sales figures. The final GDPNow estimate for the first quarter was 2.7%, the early reading were under 1%.

The US economy is showing no signs of a slowdown after almost a decade of expansion. The escalating trade war with China may crimp growth if tariffs are placed on all Chinese imports but the existing duties did little to discourage the economy in the first quarter.

Retail sales and the labor market

The robust market for jobs and the rise in wages over the past two years has provided households with the finances and confidence to weather the sentiment killing government shutdown and return to normal consumption in the first quarter.

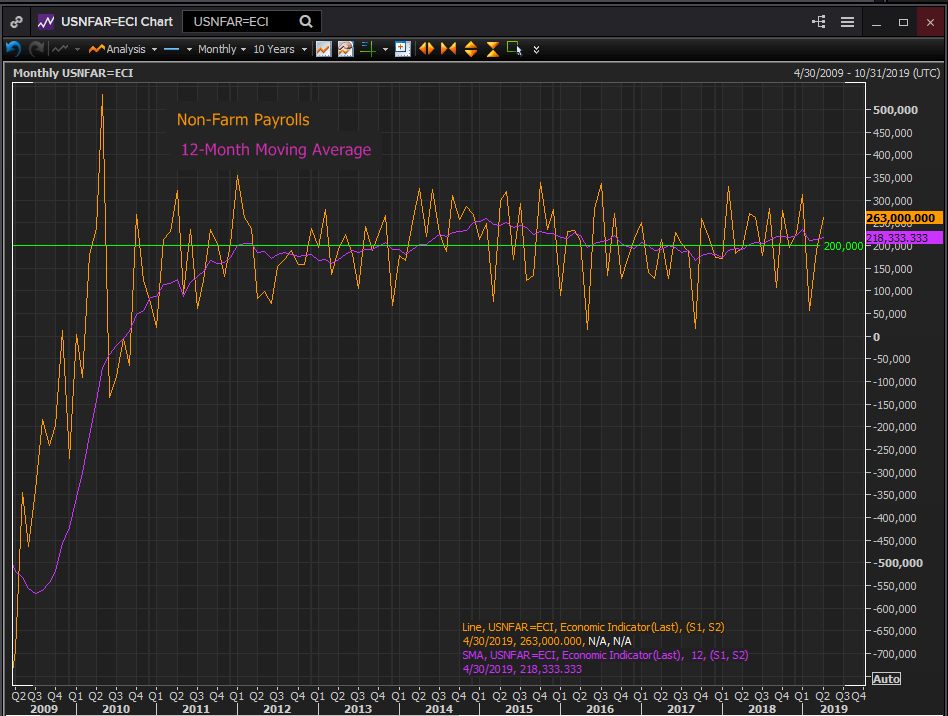

Non-farm payrolls averaged 235,000 a month in the year to January. The April decline to 218,300 was due to February’s anomalous 56,000. The annual moving average has been above 200,000 for a year.

Reuters

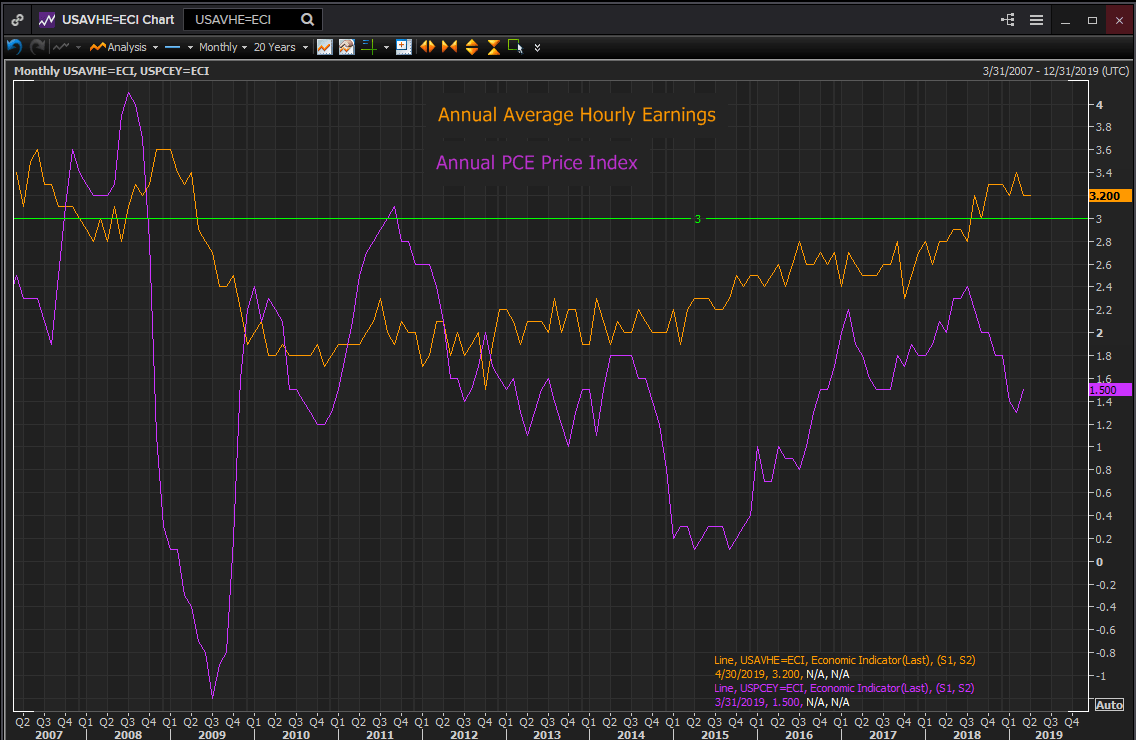

Annual wages gains have been at 3% or better for nine months, the best record in a decade. With PCE inflation below wage increases since 2012 and a widening gap beginning in July last year as wages turned up and inflation down, consumers have seen a sharp rise in purchasing power.

Reuters

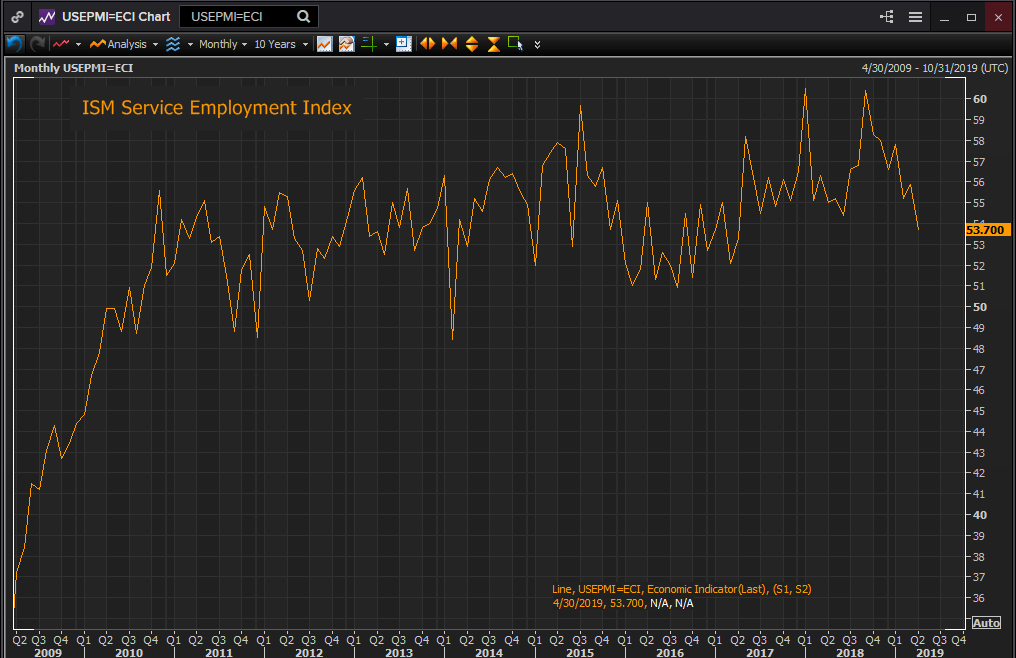

Employment indexes in services and manufacturing from the Institute for Supply Management have declined from their late 2018 highs. Services was at 53.7 in April down from last September’s euphoric 60.4, and manufacturing registered 52.4 off the 2018 top of 58.2 in September. Both employment indexes have lost all of their 2018 gains and though they remain well above the 50 division the steep drop in the past six months may mean that business demand for employees is waning. But for the moment the job market shows little sign of retrenchment.

Reuters

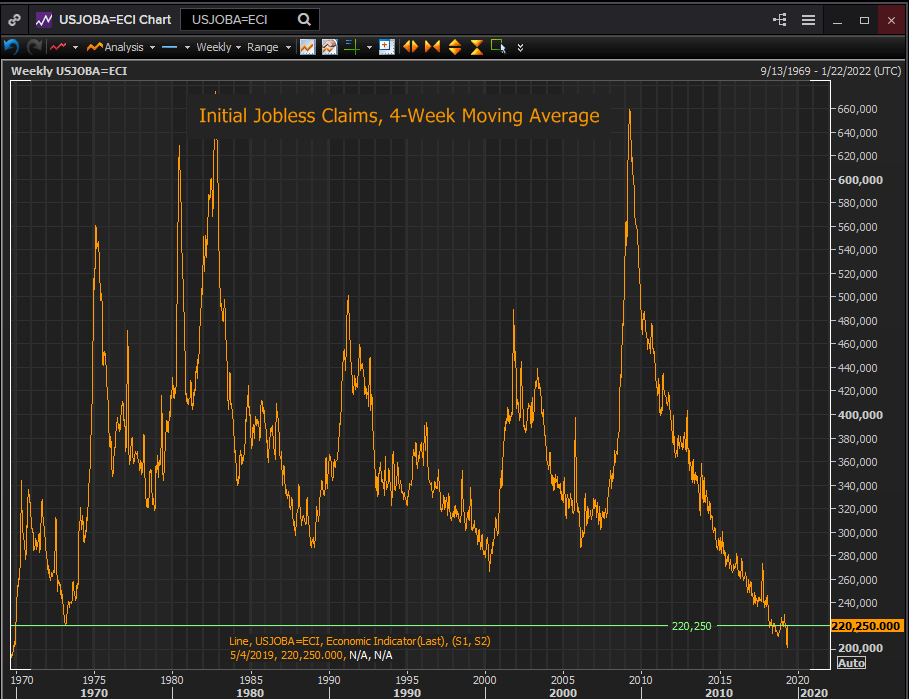

The 4-week moving average of initial jobless claims has seen a rise in the past two weeks (4/27 & 5/4) from 206,000 to 220,250 but the range of the past 18 months has been the best in 50 years. It is difficult to ascribe a labor market warning to such figures.

Reuters

It remains to be seen if the demand for labor is showing the earliest signs of slackening. For workers it is still the best job market in 50 years.

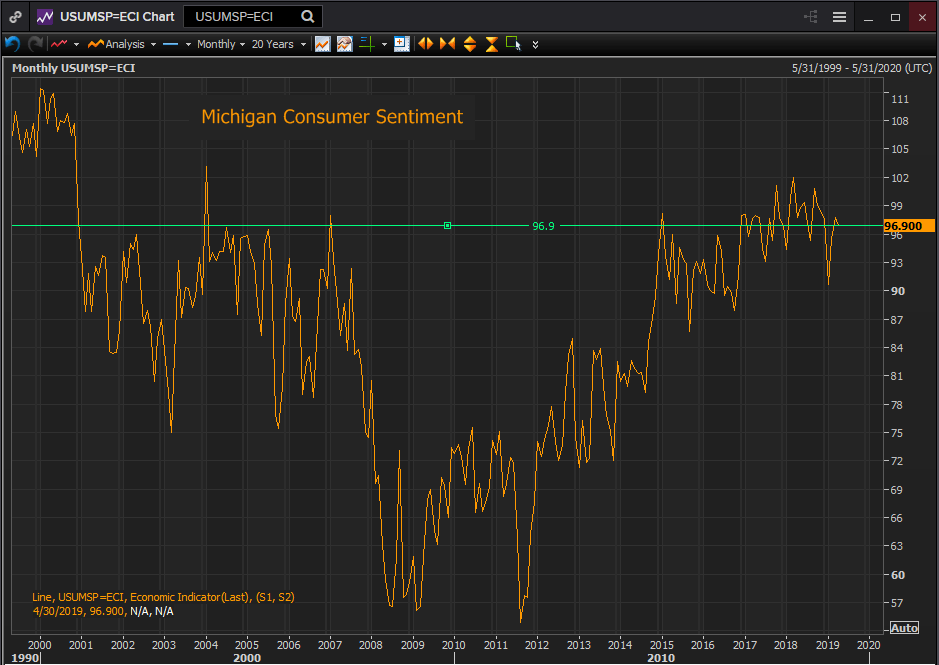

Consumer Sentiment

Optimism among American consumers has returned from its shutdown plunge. The Michigan Consumer Sentiment index was 96.9 in April midway in the range of the last two years which have been the best in two decades. The May number to be released on Friday is expected to show a slight rise to 97.5.

Reuters

Redbook Index

The Redbook Index charts change in consumer purchases based on same store sales of about 9,000 general merchandise establishments representing over 80% of the Census Bureau’s retail sales statistics.

Sales increased an average of 0.8% weekly in April continuing their rebound from the January and February decline. It was the largest gain in two years.

Conclusion

Labor market, sentiment and wages numbers point to a continuation of the first quarter’s strong retail performance. The undue pessimism of last month’s predictions seem to be repeating for April. The median estimate for March sales was 0.9%, the number was 1.6%, for the control group the prediction was 0.4% and the result was 1.0%.

This month we have a 0.2% projection for overall retail sales and 0.4% for the control group.

The labor market remains exceptionally strong, wage increases and inflation continue to improve real wages and purchasing power. Consumer sentiment is positive. If businesses seem wary that may have more to do with trade worries than any real change in the US economy.

The US consumer has little reason to pull back from enjoying the benefits of exceptional times.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.