US Retail Sales February Preview: Old news or a forecast?

- Overall retail sales and ex-autos expected to slow slightly in February.

- Control group predicted to rise after flat January.

- Michigan consumer sentiment remained firm in March.

The US Census Bureau will release the advance report on Monthly Sales for Retail and Food Services for February on Tuesday March 17, at 12:30 GMT, 8:30 EDT.

Forecast

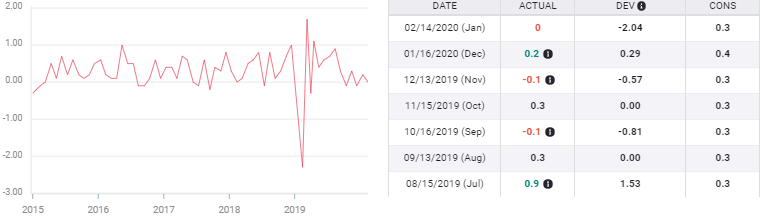

Retail sales are expected to fall to 0.2% in February from 0.3% in January. The retail sales control group, the Bureau of Economic Analysis’ (BEA) GDP component, is predicted increase 0.4% in February after being flat in January. Sales ex-autos are projected to dip to 0.2% from 0.3%.

Retail sales control group

Consumer sentiment

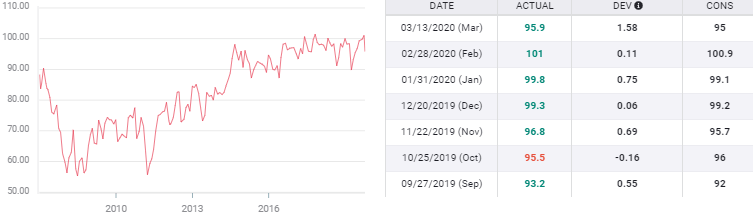

The Michigan Survey released on March 13 is the first view of the consumer economy in March after widespread knowledge of the Coronavirus in the US and the extensive declines in the stock market.

The overall index of consumer sentiment dropped to 95.9, slightly better than the 95.0 forecast and down from 101 in January. Consumer attitudes remain in the upper half of the range for the past three years but that is likely to change as the fast-moving situation develops.

Michigan Consumer Sentiment

Richard Curtin, the chief economist of the survey wrote in the note accompanying the release. “Importantly, the initial response to the pandemic has not generated the type of economic panic among consumers that was present in the runup to the Great Recession. Nonetheless, the data suggest that additional declines in confidence are still likely to occur as the spread of the virus continues to accelerate. Perhaps the most important factor limiting consumers' initial reactions is that the pandemic is widely regarded as a temporary event. “

As Mr. Curtin observed the component that fell the most was that which measured the prospects for the economy in the year ahead. This dropped by 29 points and constituted 83% of the decline in the overall index.

The gauge of current economic conditions in March slipped to 112.5 from 114.8 and the expectations index decreased to 85.3 from 92.1.

The labor market, wages and unemployment

The labor market in general and wages, job creation and unemployment were strong in February. Non-farm payrolls have averaged 231,000 in the three months to February and wages growing 3% annually and a 3.5% unemployment rate are excellent numbers. Initial jobless claims at 211,000 in the first week of March have no sign of layoffs and the forecast for the March 13 week at 216,410 is no different.

Conclusion

In the rapidly changing economic situation statistics for the months before March have become useful mostly as a gauge for measuring the expected decline.

As the Michigan Survey noted, the most promising fact on the consumer side is that the virus is seen as a temporary event. If and when that changes, especially if the impact generates layoffs and widespread financial difficulties as many businesses may furlough workers, consumer spending can be expected to decrease sharply.

Most companies are reluctant to fire workers and this may be particularly true in a situation, which no matter how unnerving, is still regarded as transitory.

The February retail sales figures are, to a much greater degree than normal, retrograde and not useful in assessing the current economic direction. Unless of course, they show an unanticipated drop, in which case they will be seen as a harbinger of much worse declines to come.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.