US Retail Sales expansion slows in October, GDP estimate improves

- Retail Sales rise for the sixth straight month.

- September results reduced for Sales and Control Group.

- Rising COVID-19 cases may have affected spending.

- Industrial Production and Capacity Utilization gain.

- Sales have limited impact on equity, credit and currency markets.

Americans spent less than analysts had expected in October but the run of positive months extended to six even as new social and business restrictions in some states threaten to curtail holiday shopping and expenditures.

Retail Sales rose 0.3% last month, according to the Commerce Department, missing the consensus forecast for a 0.5% gain. September's initial 1.9% increase was revised down to 1.6%.

Retail Sales

Sales have increased for six months in a row with the average gain from March through October of 0.89%, or 7.1% for the period.

The Retail Sales Control Group, which excludes automobiles, gasoline, building materials and food services rose 0.1% in October following September's negative revision to 0.9% from 1.4%. This Commerce Department category closely mimics the consumption component of gross domestic product (GDP) and is sometimes called core retail sales. Control Group sales have averaged 1.06% for the eight months of the pandemic, or 8.5% in total.

Pandemic impact

Diagnosed cases of COVID-19 have been rising steadily in the United States prompting business restrictions in some states and giving consumers reasons for avoiding restaurants, bars and other public venues, but few of those new closures were in October. Bar and restaurant reciepts declined 0.1% on the month.

The economic impact of these rules and behavior is unknown as many of these businesses had never fully reopened after the original lockdowns in March and April and have been operating at a much reduced level.

Sales patterns have shifted in response to the pandemic with increases in purchases for personal and home use like exercise equipment and new cars while spending for public and social setting like theaters, bars, restaurants and travel have fallen.

Non-store retailers, the government's category which includes online merchants, have been a big winner throughout with receipts rising 3.1% in October. Consumers have moved traditional in-person shopping goods from food and medicines to clothing increasingly online.

Sales and GDP

Consumer spending has been a main ingredient in the economy's 33.1% annualized growth in the third quarter following the 31.4% collapse in the second.

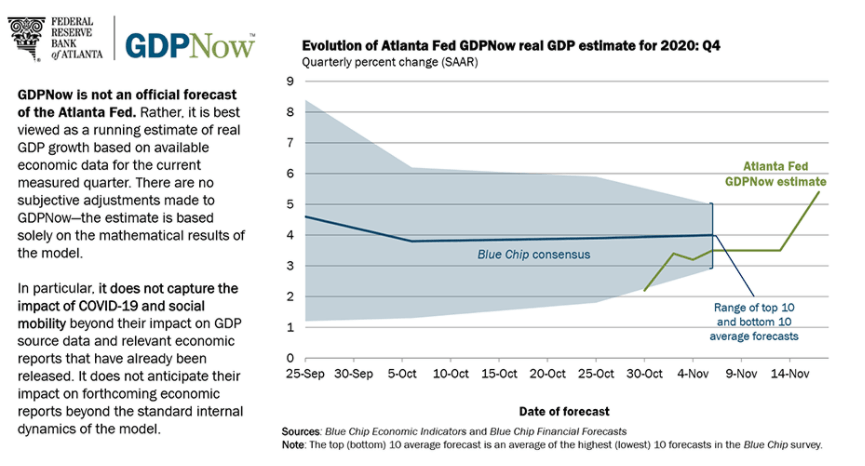

The Atlanta Fed's latest estimate for growth in the final three months of the year rose to 5.4% from 3.5% as real Personal Consumption Expenditures are now expected to increase 2.6% as opposed to the prior -0.4% forecast.

Unemployment and spending

The new series of business closures may cause an increase in layoffs, unemployment claims and a loss of income and spending.

Jobless benefits that normally last for six months have lapsed for a growing number of people. Many of those workers have presumably been rehired but for others a supplement that was part of the pandemic relief bill expired in the summer.

Benefits for millions more self-employed workers may vanish next month when another government program is due to end as will payments to those whose original eligibility was extended.

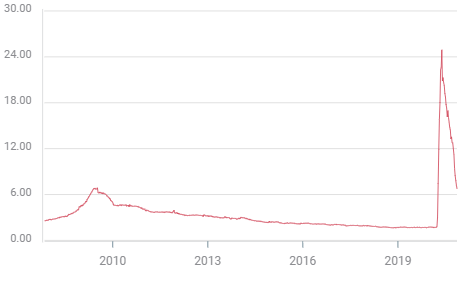

Continuing Claims have been steadily declining since the May peak of 24.9 million. The latest week had 6.786 million listed on the unemployment rolls.

Continuing Claims

A second economic package is unlikely until a president is inaugurated on January 20.

Consumer sentiment

Attitudes among American consumers have not recovered from the pandemic impact.

The preliminary reading from the Michigan Consumer Sentiment Index for November showed the first drop in four months to 77 from 81.8 in October. For the six months to February the average was 97.6.

Industrial Production and Capacity Utilization

In a separate report from the Federal Reserve Industrial Production rose 1.1% in October slightly more than the 1% forecast. The September result was adjusted to -0.4% from -0.6%.

Capacity Utilization, which measures the percentage of the US industrial base in use, rose to 72.8% in October from 72.%. It was the highest reading since March.

Markets

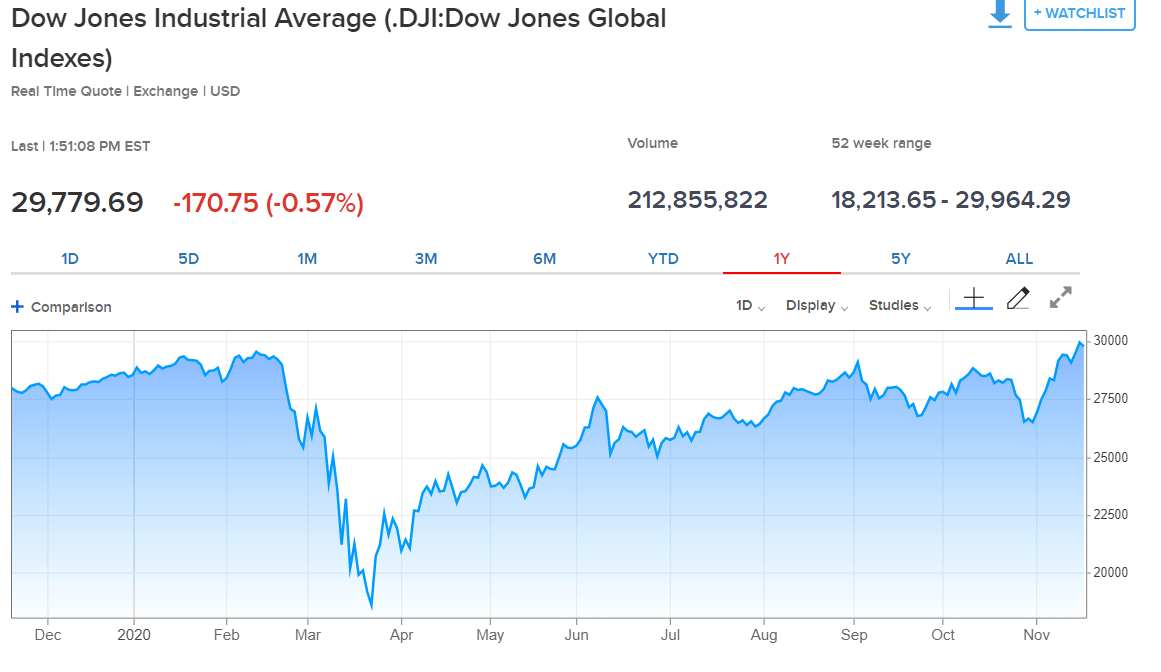

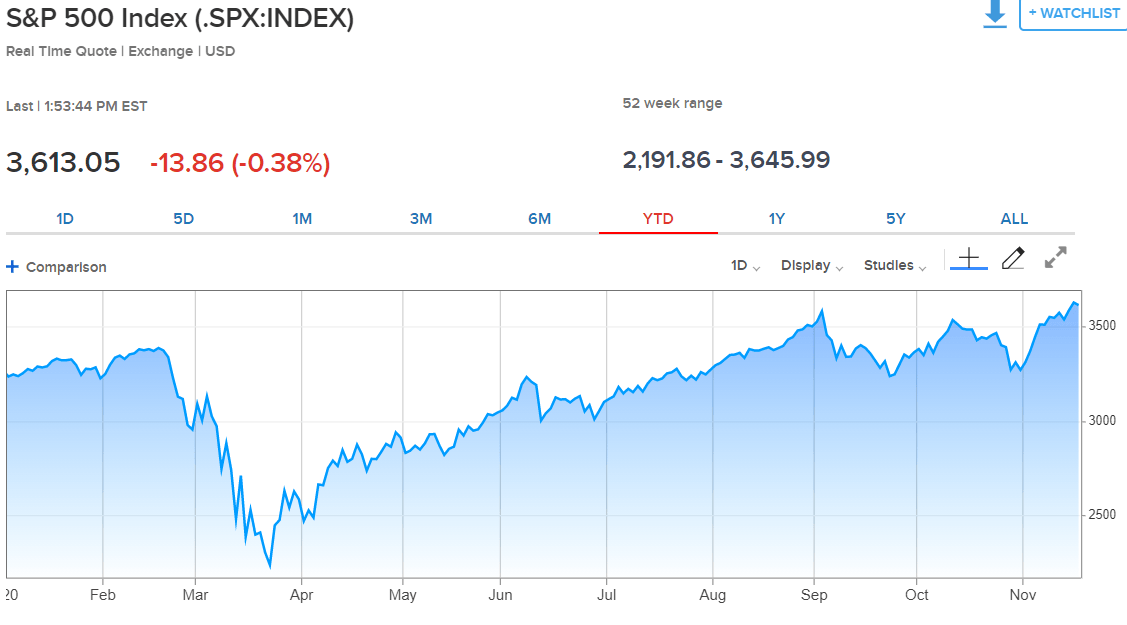

Equities and credit market yields declined as the sales figures somewhat undercut the recent optimism from successful vaccine trials.

The Dow was off 170.75 points as of this post, at 29,779.69, but that comes after yesterday's record close at 29,950.44.

The S&P 500 was down 14.15 points at 3,612.78 also after setting a all-time high on Monday of 3,626.19.

Treasuries were modestly higher with the yields on the 10-year, which moves inversely to prices, at 0.872%, down three basis points ( 1:56 pm ET). The return on this benchmark note had reached an eight-month high of 0.972% on November 10.

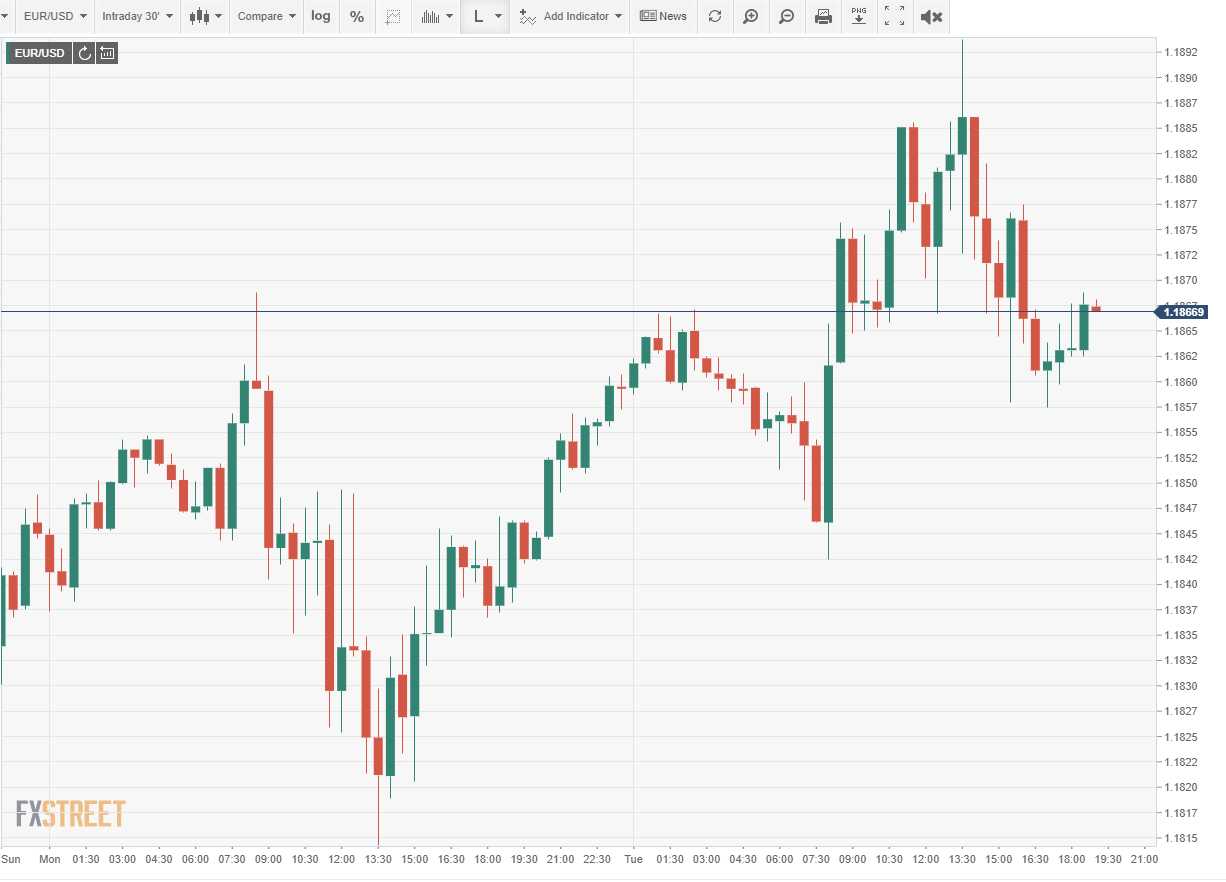

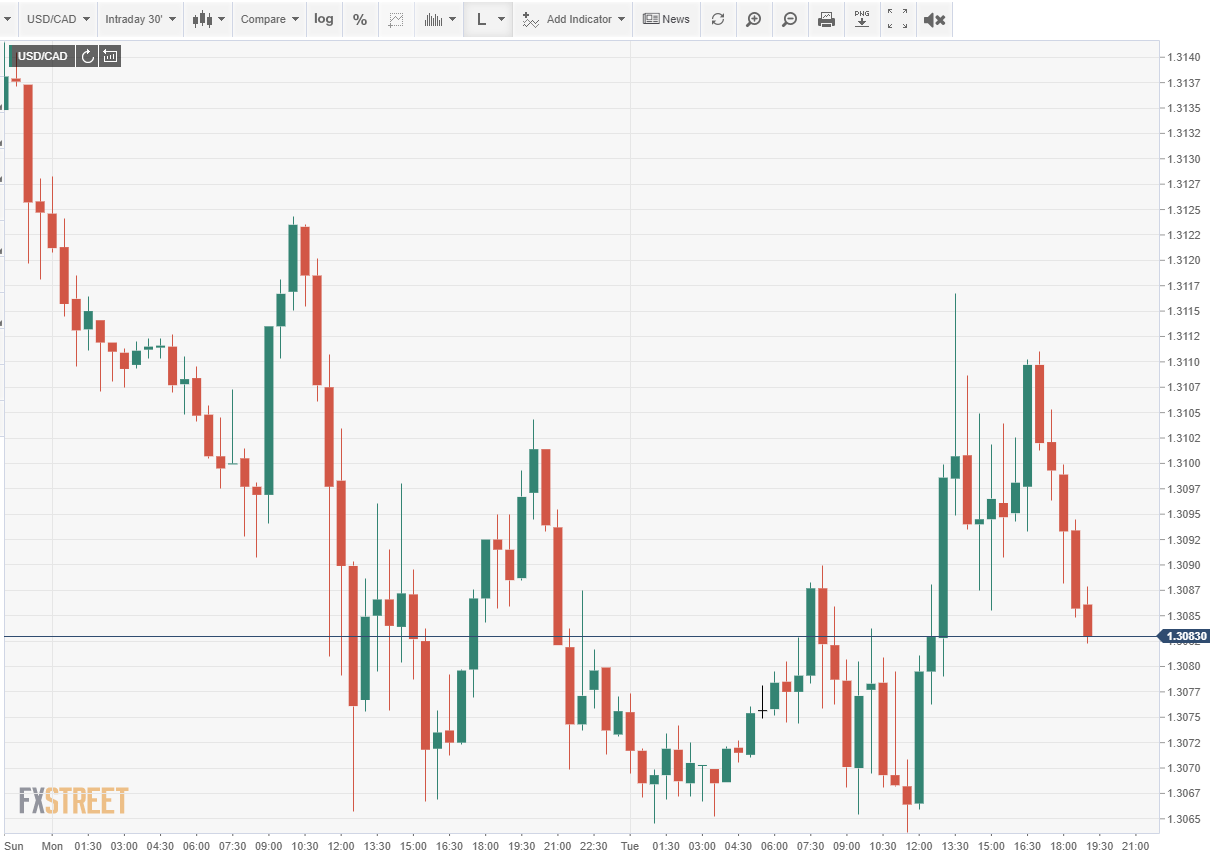

The dollar has improved slightly since the release at 8:30 am ET (13:30 GMT) against the EUR/USD adding 15 points to 1.1867 and lost ground against the Canadian dollar from 1.3099 to 1.3083. The greenback is flat versus the Japanese yen.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.