US Retail Sales August Preview: Surprising facts on retail sales

- Retail sales forecast to gain 1% in August after 1.2% in July.

- GDP component control group expected to add 0.5%, following 1.4%.

- Pandemic collapse in sales exceeded by 21%, control group 41% in recovery.

- Sales average March through July the best in 11 years.

- Dollar off its lows but range bound for more than a month.

The US consumer has more than replaced the sales debacle of the pandemic closures but the excellent half year has not brought the American labor economy back to its heights of last year.

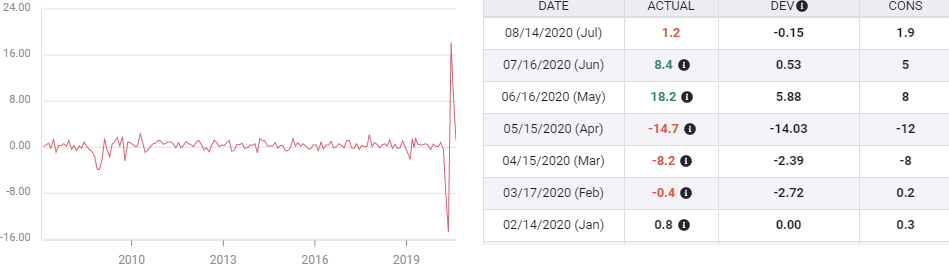

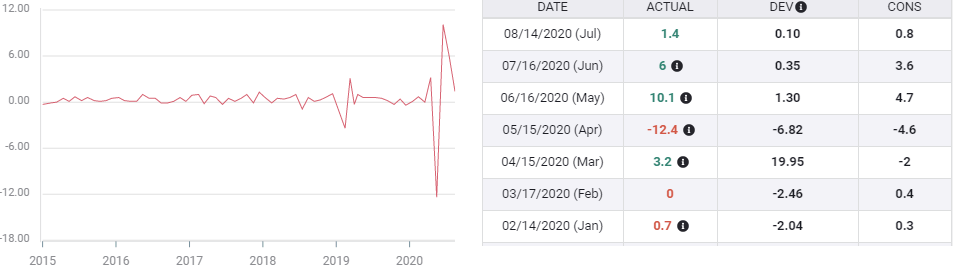

Retail sales are expected to grow 1% in August after rising 1.2% in July. Purchases in the GDP component control group are forecast to increase 0.5% following the July gain of 1.4% and sales ex-autos are projected to rise 0.9%. They were 1.9% higher in July

Pandemic sales recovery and GDP

The major categories of retail sales have had an excellent five months, the best in over 10 years. Despite March and April when sales collapsed by the largest amount on record as the economy was shut by government fiat, the recovery in May June and July was so energetic that the average for the whole period is one of the highest in history.

From March through July sales averaged a 0.98% increase each month. The last time the US consumers spent so avidly was in 2009 when sales gains averaged 1.02% from April through August.

Retail sales

The control group was even more energetic averaging 1.66% monthly for the recent period.

It is worth repeating that these averages include the collapse of sales in March and April. This surge in consumption is the main reason that GDP is expected to reverse the second quarter’s 31.8% plunge with a redemption estimated by the Atlanta Fed to be at 30.8%, both figures annualized.

Control group

The total sales decline in March and April was 22.9%. The subsequent three month recovery was 27.9%. The average for the five month period as above is expected to continue into August at 1%, making it one of the best periods for sales on record.

The decline in control group was 12.4% in April, these sales rose 3.2% in March. The additions of 10.1% in May, 6% in June and 1.4% in July produced the 1.66% average noted earlier. The 0.5% forecast for August will only drop the six month average to 1.47%.

Payrolls and initial jobless claims

The resumption and extension of the retail purchases has not restored the labor market to its per-pandemic health.

Non-farm payroll have recovered 48% of the March and April shutdown job losses (10.56 million vs 22.16 million). Initial jobless claims continue to run at nearly 1 million new filings per week and continuing claims rose to 13.385 million from 13.292 million in the latest, August 28, week.

Many of the jobs lost and not recreated were in the service sector and not directly related to the production and sales of retail goods. These businesses continue to lay off workers though some of the income has been replaced by claims unemployment benefits and various other programs.

Conclusion and the dollar

The decline in the dollar over the past two months was based on the anticipated damage to the US recovery from the second Covid wave. If the Atlanta Fed numbers are accurate the economy has continued to expand, hiring millions more back into the labor force at the same time that specific sectors continue to shed jobs.

That dual-track labor economy has penned the dollar into a tight range over the past weeks, unable to gain traction in either direction. While the US economy and labor market improve the continuing high levels of layoffs have undercut the notion of a wholly successful recovery and blocked the boost an unequivocal return would give to the US dollar.

Retail sales have been excellent for three months replacing the entire spring collapse with a surge of near record volume but it has not been enough to restore the labor market and that is where the focus for the dollar resides.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.