US Non-Farm Payrolls: Correlation what correlation?

- Non-farm payrolls adds 224,000 in June far better than the 160,000 prediction

- Unemployment rate climbs 3.7%, 0.1% above May’s 50 year record

- Wages growth unchanged at 3.1%, participation rate rises

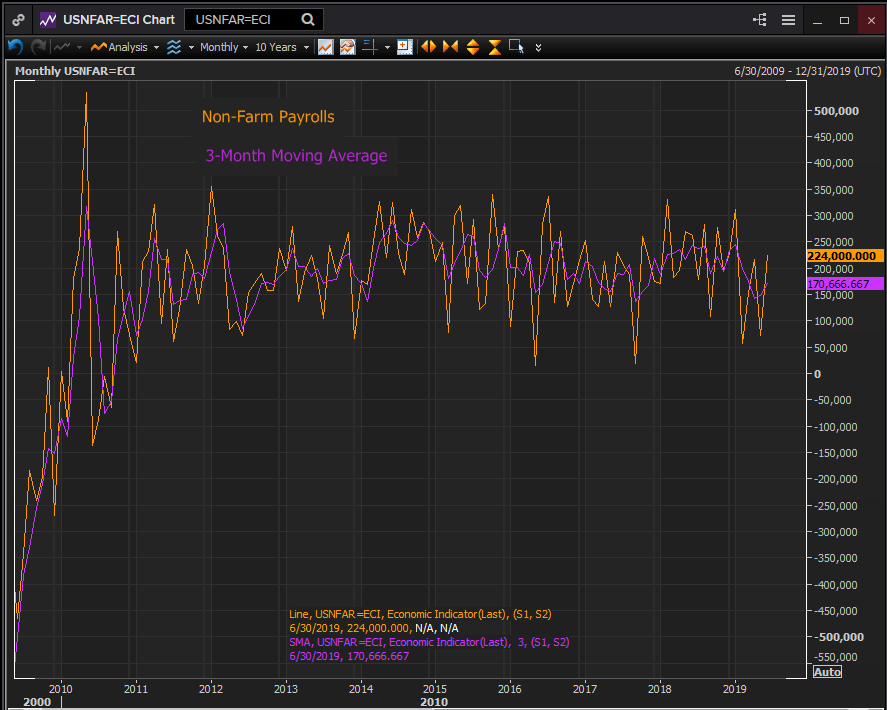

Job creation in the US returned to form as businesses added 224,000 new positions in June, well above the 160,000 forecast. The best performance since January helped to arrest concerns that the labor economy had begun to cool in line with apparently weaker GDP growth in the second quarter.

Reuters

The unemployment rate rose to 3.7% just 0.1% above May’s five decade record and the labor force participation rate climbed to 62.9%, according to the Labor Department on Friday.

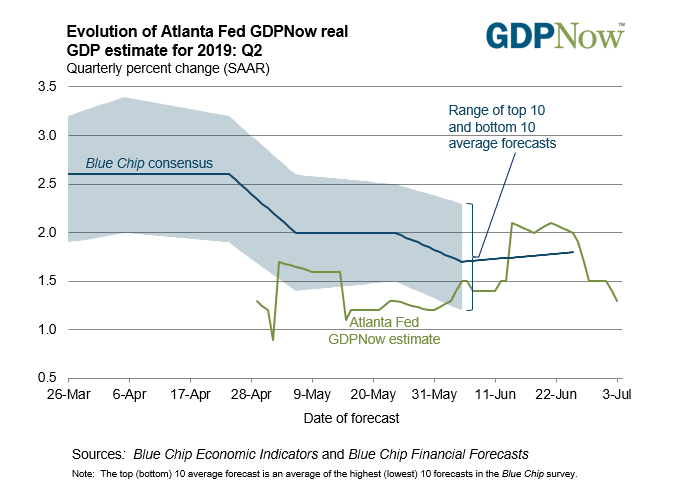

May’s poor payroll report of 72,000, revised from 75,000, which came three months after February’s 56,000 result and coincided with the ADP private payroll figures of 41,000 in May and 102,000 in June had raised intense speculation that the labor market, long a strongpoint of the expansion was shifting lower perhaps following the Atlanta Fed’s GDPNow estimate for the second quarter of 1.3% on July 3rd. The April NFP total was also revised down to 216,000 from 224,000.

The Fed governors have been watching the payroll numbers carefully for a reading of the direction of the US economy.

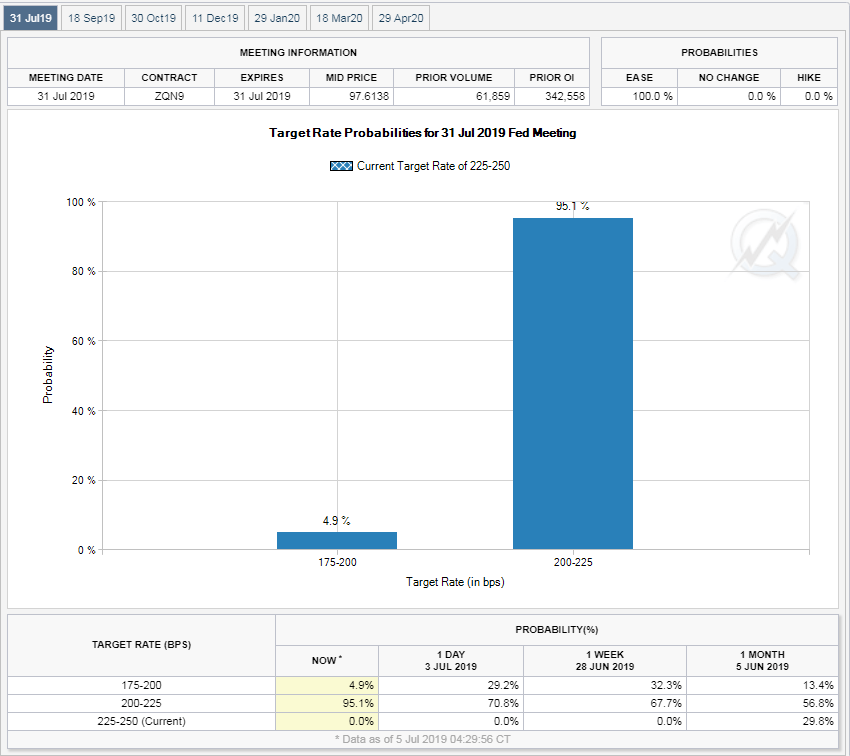

Markets have been widely anticipating a rate cut since the June 19th Fed meeting. The Fed Fuds futures showed a 95.1% conviction for a 25 basis point at the July 31st FOMC meeting and a 4.9% possibility of a 50 basis point reduction. Prior to the payroll numbers the futures had been listing a 74.5% chance of a 0.25% cut and at 25.6% chance of a 0.5% decrease.

CME Group

Federal Reserve Chairman Powell will testify before Congress this coming week at the House Financial Services Committee on Wednesday and the Senate Banking Committee on Thursday.

Mr. Powell will certainly be asked about interest rate policy and whether the Fed expects to cut the fed funds rate at the end of the month. In the political atmosphere of a Congressional hearing he is unlikely to offer specifics or to alter the tone and direction of his comments from the past weeks and to defer the decision to the incoming data.

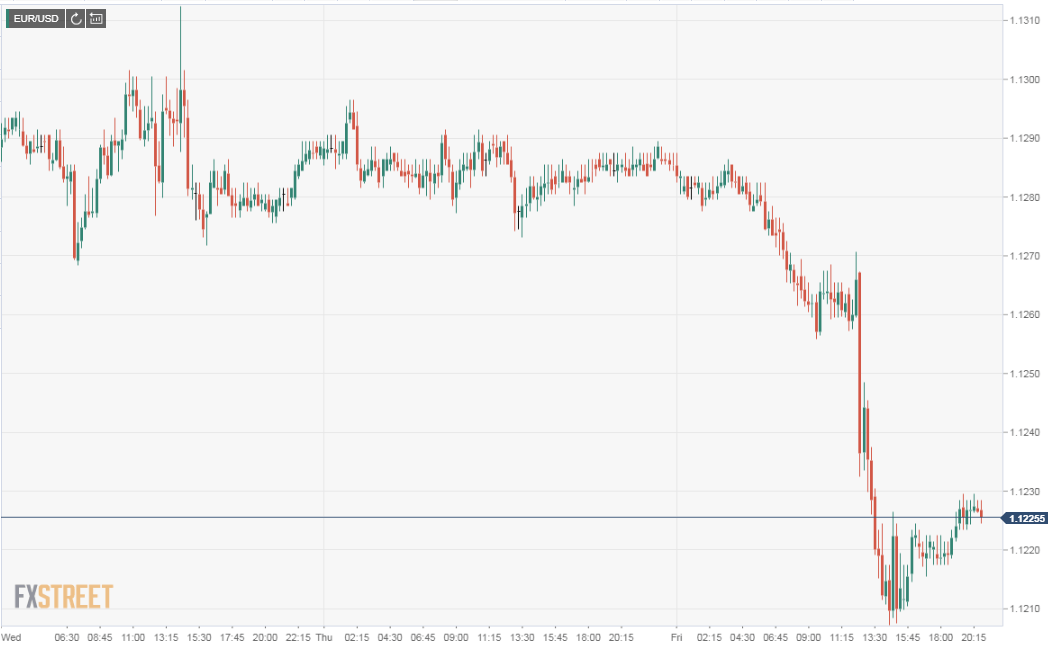

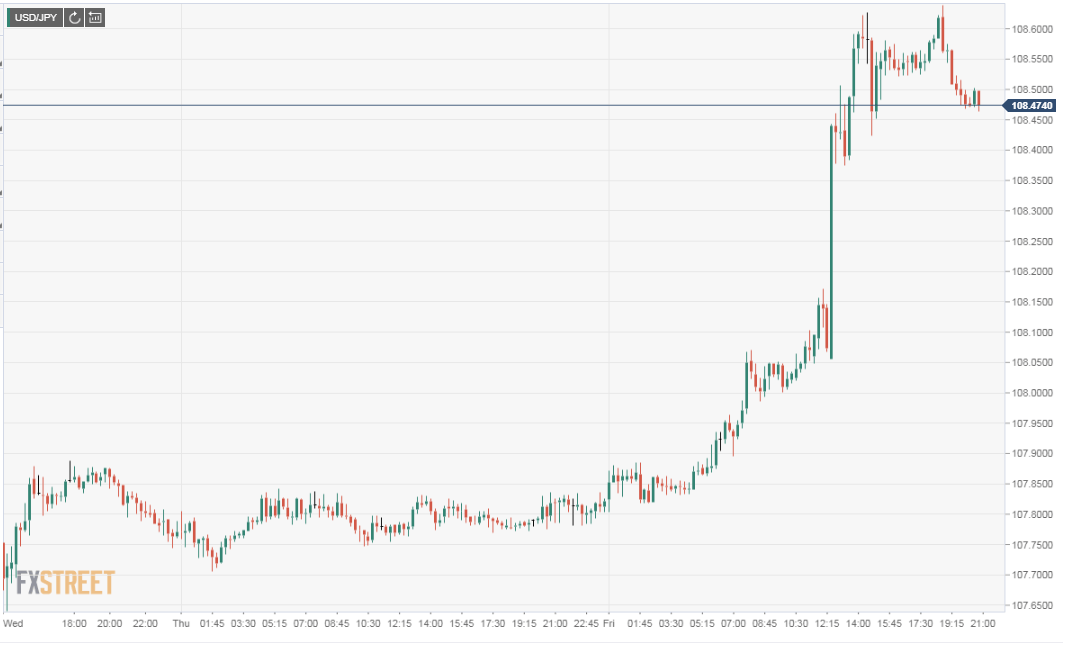

The better than expected payrolls gave the dollar a sharp boost initially gaining about 75 points against the euro and more than a figure versus the yen and the sterling. Near the New York close they were trading at 1.1227, 108.49 and 1.2525 respectively.The yield on the 10-year generic bond gained 9 points to 2.04%. The 2-year added 11 points to 1.87%, its highest in almost three weeks.

The Dow closed down 43.88 points, 0.16%, at 26,922.12 having been lower by over 200 points early in session. The S&P 500 finished off -0.18%, 5.41 points at 2990.41.

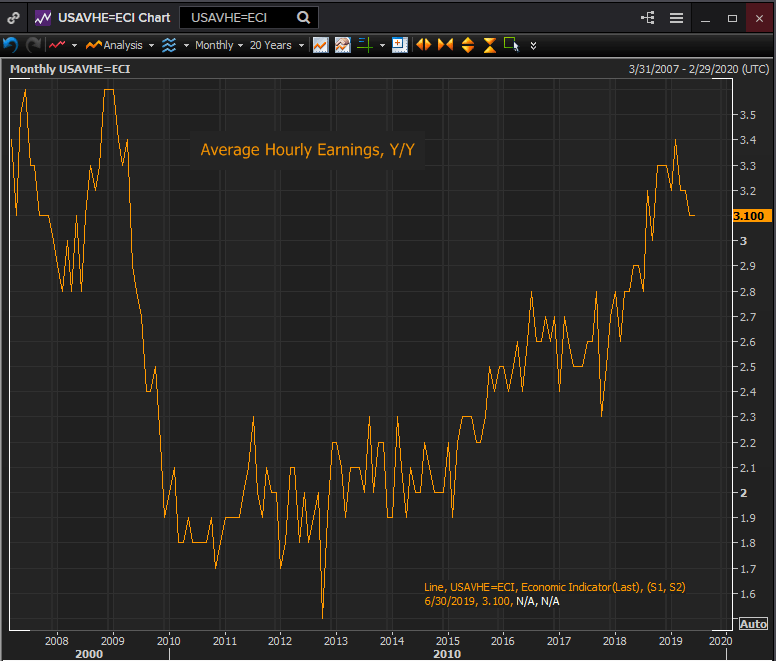

In other statistics from the Employment Situation Report, the official title of non-farm payrolls, annual average hourly earnings were unchanged at 3.1% in June. They have now been at or above 3% for 11 straight months, the best sustained run since April 2009. Wages rose 0.2% in June, missing the 0.3% prediction but as the prior month was revised up to 0.3% from 0.2% the net change was nil. The average work week was stable at 34.4.

Reuters

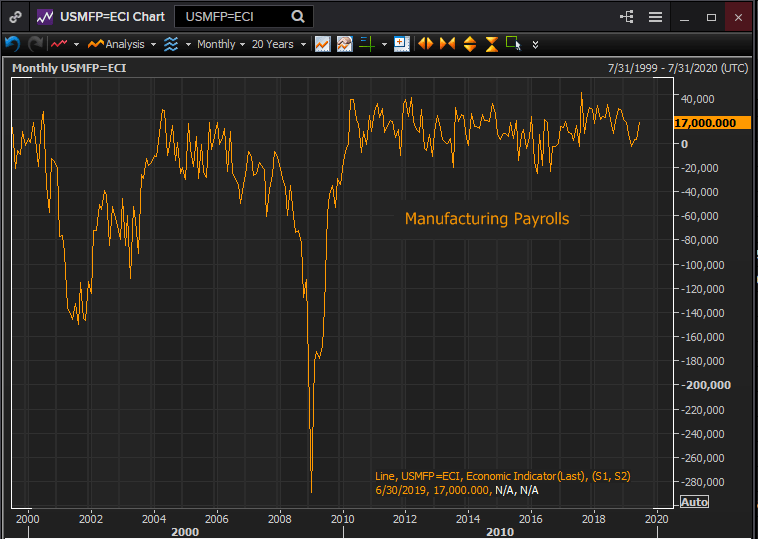

Manufacturing payrolls climbed 17,000 in June outstripping the flat forecast for the largest increase in factory work since January. Government employment rose 33,000 across all levels of local, state and federal bureaucracies.

Reuters

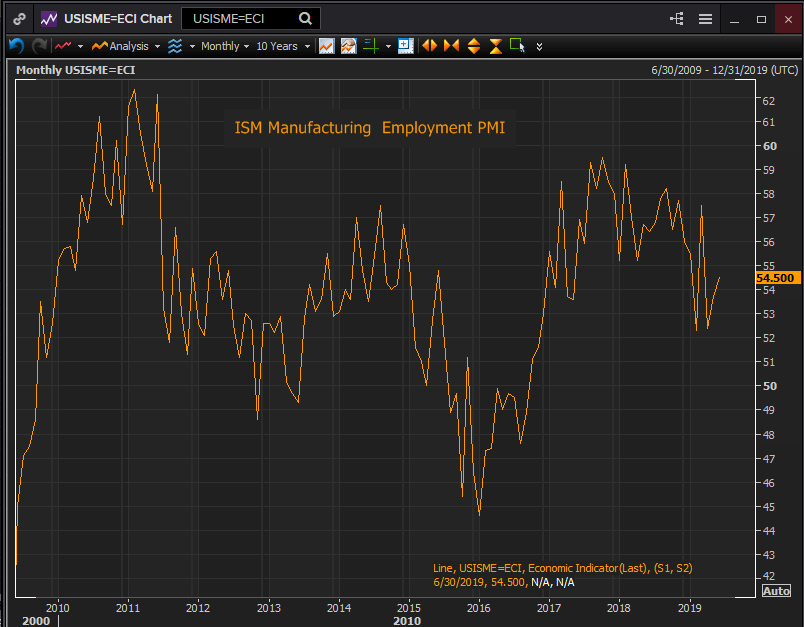

Sentiment in the manufacturing sector has been falling for 10 months. The ISM purchasing manager’s survey reached a post-recession high of 60.8 last August. The June score of 51.7 was the weakest in almost three years. Despite the decline in the overall survey the employment index has seen a modest recovery from its three year lows in February at 52.3 and April of 52.4, registering 54.5 in June.

Reuters

The trade dispute with China has been a large factor in the drop in sentiment and even though negotiations have restarted, expectations for a deal are much lower than they were six months ago. The Fed has consistently cited the disagreement as one of the risks to the US and the global economy.

The excellent overall payroll report has shifted the tenor of the debate on Fed rate cuts. What was expected to be a cycle of several reductions has become a question of whether the central bank will move at all this month and if so will it be one and then a pause. Aside from the economics, it might be risky for the governors to demur on the 31st with expectations running so heavily to a 25 basis point cut. It would certainly rile the markets, undercutting equity strength and adding to the dollar's.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.