US Manufacturing Purchasing Managers’ Index Preview: Revival is near

- Manufacturing sentiment depressed by global trade disputes

- Business spending weak

- Consumer sector maintains even keel

The Institute for Supply Management (ISM) will issue its purchasing managers’ index (PMI) for the manufacturing sector in August on Tuesday September 3rd at 14:00 GMT, 10:00 EDT.

Forecast

The purchasing managers’ index is expected to slip to 51.0 in August from 51.2 in July. The prices paid index is predicted to rise to 46.3 from 45.1. The employment index was 51.7 in July and 54.5 in June. The new orders index was 50.8 in July and 50.0 in June.

ISM Survey

The Institute surveys “a group made up of more than 300 purchasing and supply executives from across the country.” They answer a “monthly questionnaire about changes in production, new orders, new export orders, imports, employment, inventories, prices, lead times, and the timeliness of supplier deliveries in their companies comparing the current month to the previous month.” The responses are scored on a scale with 50 as the division between expansion (above) and contraction (below). *Quotations from the Institute for Supply Management website.

US, China and manufacturing: Waiting for trade

The manufacturing sectors in China and the United States have been hard hit as the trade war and the prospective fallout from the British exit from the European Union has degraded global economic growth.

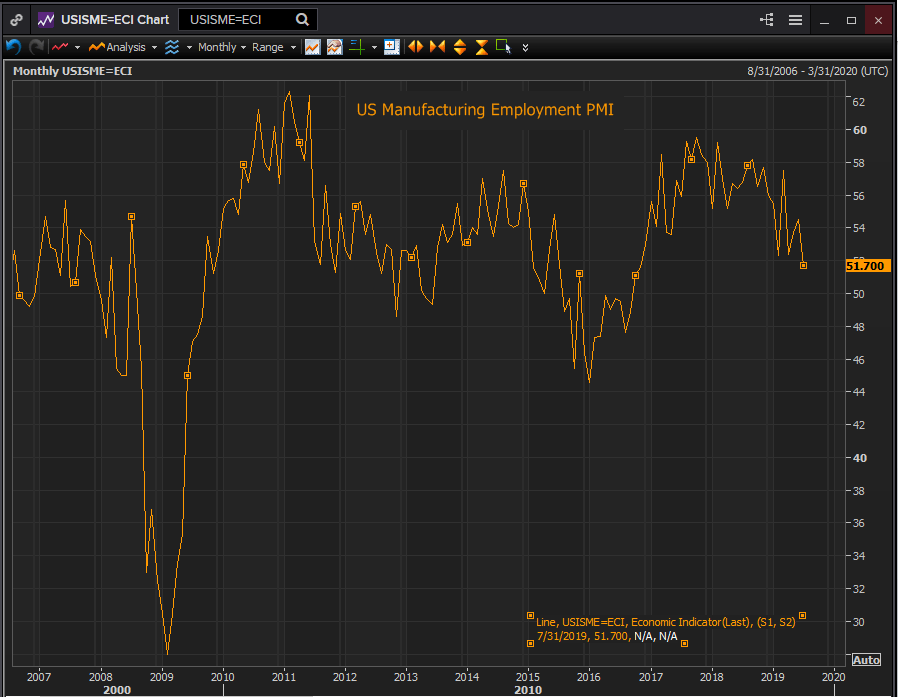

The US PMI manufacturing index has dropped from 60.8 in August 2018, the highest score in 15 years, to 51.2 in July the lowest reading in three. The two most important sub-indexes, employment and new orders have plunged in tandem with the headline. Employment has dropped from 59.2 in February 2018 to 51.7 in July and new orders have fallen from 67.3 in December 2017 and 64.5 in August 2018 to 50.0 in July and 50.8 in July.

Reuters

The sharp decline in attitudes and business in the manufacturing sector has come as the US economy has maintained moderate economic growth, 3.0% in 2018 and 2.55% in the first half of this year with a current 2.0% estimate for the third quarter from the Atlanta Fed.

The optimistic belief that the US and China would be able to settle their trade differences that prevailed for most of 2018 received a sharp blow in May from which it has not recovered when China refused to agree to previously negotiated terms to produce a draft treaty. Since then competing accusations and tariffs by both sides have been the most of the dialogue.

China indicated a willingness to resume negotiations this week saying that the trade war should be resolved with a “calm attitude.” The two sides resumed talks at a “different level” on Thursday according to US President Donald Trump.

Optimism was muted on the US side, “Let’s see what the end product is; that’s what you have to judge it by,” Trump said.

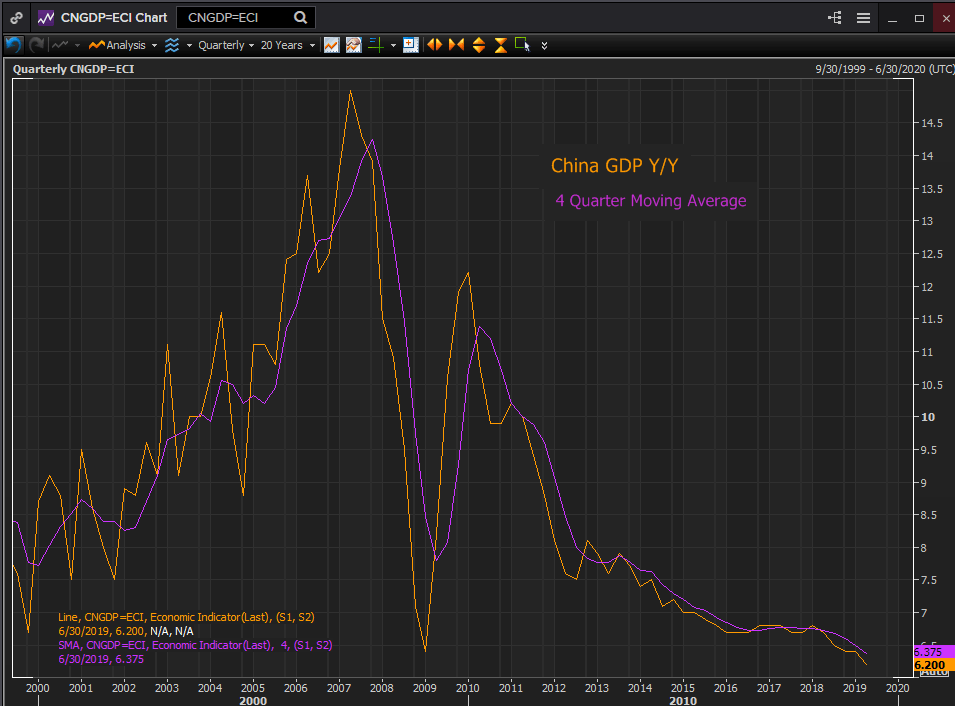

The Chinese economy, which is far more dependent on manufacturing and exports than the US, has seen it slowest official growth in a generation in the last quarter at 6.2%.

Reuters

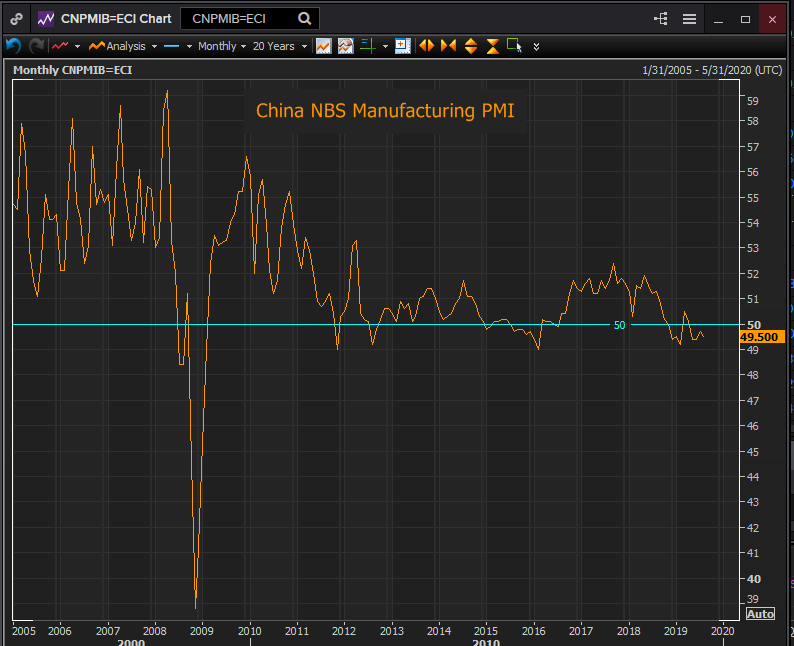

The purchasing managers’ index in manufacturing from the government’s National Bureau of Statistics has been below 50 for four months and for seven of the last nine months. The decline in sentiment mirrored that in the US though it started from a much lower level.

Reuters

US manufacturing employment

The drop in the overall manufacturing PMI sentiment and employment has been partially reflected in actual employment numbers in the Non-Farm Payroll report.

In the six months from February that have seen the rapid fall in the manufacturing employment PMI the three months moving average of new hires has dropped from 15,000 in February to 10,000 in July. The last two reported months, June and July, averaged 14,000.

Reuters

The August payroll numbers will be reported on September 6th with 159,000 expected overall and 7,000 in manufacturing. If those forecasts are accurate that would leave the three month moving averages at 172,000 for NFP and 11,700 in manufacturing. Those are not the figures of a pending collapse in employment. The other significant labor indicators, initial jobless claims, unemployment and ADP payrolls remain healthy.

Conclusion

The precipitous fall in US manufacturing PMI this year may have as much to do with disappointment that the trade talks with China did not fulfill their original promise, which would have provided a substantial boost to the factory sector, as being an accurate reflection of the state of the US economy.

The US-China trade relationship has assumed a mildly acrimonious but functional aspect. The negotiations and the public view of them are now based in realism and much clearer ideas of the competing national interests at stake. This new normal in the US China may not be as dangerous as the Fed feared when it paid the first economic insurance premium in July.

The US labor market continues to fuel a buoyant consumer economy. Domestic manufacturers could regain some of their optimism if sales continue at their present pace. The US and China may be at trade loggerheads, but the American consumer is paying little attention.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.