US Manufacturing Purchasing Managers’ Index: October’s promise looking for confirmation

- Factory sector confidence to rise but remain in contraction.

- Unexpected jump in October business spending may offer promise.

- Retail sales and GDP stronger than expected.

- Potential dollar rally awaiting improved US statistics

The Institute for Supply Management (ISM) will issue its purchasing managers’ index (PMI) for the manufacturing sector in November on Monday December 2nd at 15:00 GMT, 10:00 EDT

Forecast

The purchasing managers’ index is expected to rise to 49.4 in November from 48.3 in October and 47.8 in September. The prices paid index is predicted to rise to 49.9 from 45.5. The employment index was 47.7 in October and 46.3 in September. The new orders index was 49.1 in October and 47.3 in September.

ISM Report on Business, Manufacturing

The Institute for Supply Management is an over 100 year old non-profit organization whose mission is to help “…industry professionals generate positive outcomes.”

The ISM manufacturing survey is based on the responses of “a group made up of more than 300 purchasing and supply executives from across the country.” These professionals respond anonymously to a “monthly questionnaire about changes in production, new orders, new export orders, imports, employment, inventories, prices, lead times, and the timeliness of supplier deliveries in their companies comparing the current month to the previous month.” The answers are tabulated into an index and rated on a scale that places the division between expansion and contraction at 50 with the first above and the latter below.

*Quotations from the Institute for Supply Management website.

US manufacturing sector

American factories have not paid as heavy a toll for the trans-Pacific trade dispute as their counterparts in China.

According to the ISM purchasing managers’ index the manufacturing sector has been in contraction for three months, since August. The scores have been declining for more than a year after reaching 60.8 in August 2018.

The institute defines contraction as a reading below 50 in the compiled percentages of executives who say business is better and those who say it has gotten worse since the previous survey.

In comparison the official Chinese PMI manufacturing survey from the National Bureaus of Statistics had been in contraction for six straight months and for nine of the last 11 months before November’s 50.2 release on Saturday .

US October PMI

There were positive signs in the October PMI numbers. The overall index bounced slightly to 48.3 from 47.8, which by 0.2 had been the lowest reading since the recession. The index registered 48.0 in January 2016.

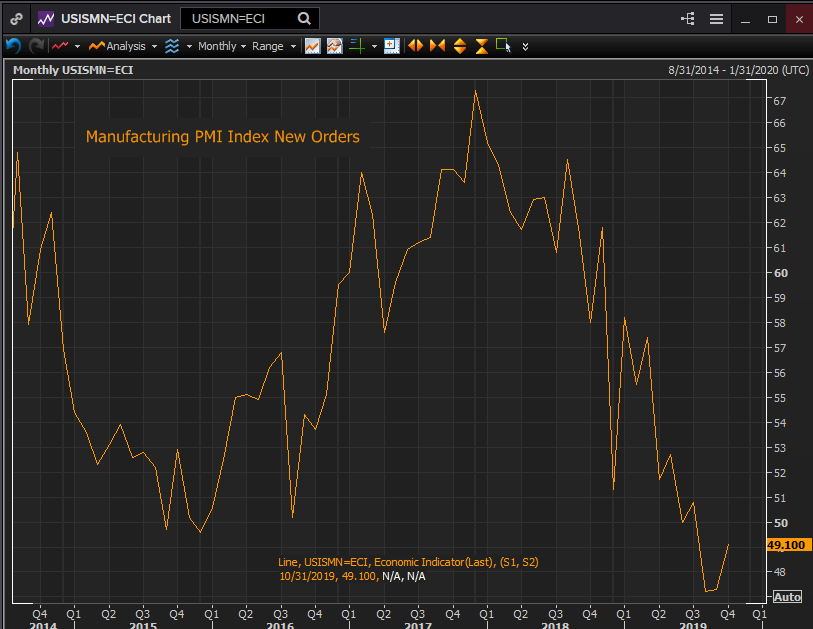

New orders climbed from 47.3 in September to 49.1 in October but the new export orders index jumped into expansion at 50.4, a gain of 9.4 points over the September reading of 41.0.

Reuters

The collapse in export business in the almost two-year old trade war has been one of the sources of the decline in manufacturing. Has the prospect of a US China trade deal, promised but not yet fulfilled, prompted foreign purchasers to take advantage of lower prices from US factories? This index bears watching in the November report.

Business and retail spending

Another notice that recession may have bottomed was the unexpected rise in the business spending proxy category of durable goods orders, non-defense capital goods ex aircraft. This ungainly named class soared 1.2% in October, five times the anticipated 0.3% decline. Had the prediction been correct it would have been the third decrease in a row and the fourth month without an increase, July was flat.

Durable goods, non-defense capital goods ex-aircraft

The decline in business spending has been the chief culprit in the decrease of GDP from an annualized 3.1% rate in the first quarter to 2.0% in the second and 2.1% in the third.

Retails sales, supported by the strong labor market and consumer sentiment, have maintained a steady pace throughout this year. Consumer spending has kept the economy on an even keel and a better than expected consumption component in was responsible for the upward revision in Q3 GDP from 1.9% to 2.1%.

Conclusion: Dollar may rally on improving PMI

Early signs from export orders, business spending and retail sales indicate that the manufacturing downturn may be lightening. If the confidence in an eventual US China trade deal takes hold in the business community the initial turn could become a rush for advantage.

Currency markets may be on the edge of a dollar rally. If the US manufacturing sector starts to exhibit a positive aspect, the dollar could quickly follow.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.