US Manufacturing PMI Preview: Trade takes back seat to the virus

- Sentiment expected to be in contraction for the sixth month.

- Business investment fell in December after two positive months.

- China trade deal improvement will be delayed by health crisis.

The Institute for Supply Management (ISM) will issue its purchasing managers’ index (PMI) for the manufacturing sector in January on Monday, February 3rd at 15:00 GMT, 10:00 EDT.

Forecast

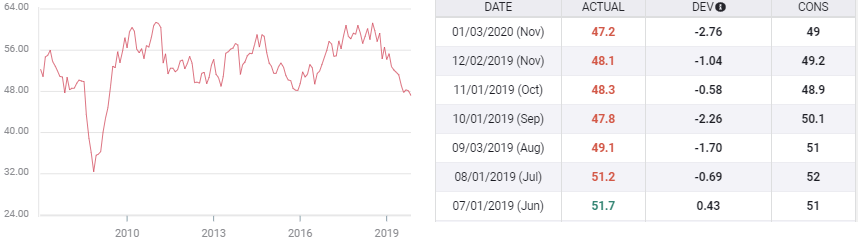

The purchasing managers’ index is expected to rise to 48.5 in January from 47.2 in December and 48.1 in November. The prices paid index is predicted to fall to 49.3 from 51.7.

The new orders index registered 47.2 in November down from 49.1 a month earlier. Employment fell 1.1 points to 46.6 and new export orders dropped to 47.9 in November from 50.4 in October.

ISM Manufacturing Report on Business

The purchasing managers' index is composed of the answers of “a group made up of more than 300 purchasing and supply executives from across the country.” These executives are polled anonymously by a “monthly questionnaire about changes in production, new orders, new export orders, imports, employment, inventories, prices, lead times, and the timeliness of supplier deliveries in their companies comparing the current month to the previous month.”

The responses in the monthly poll are ranked in an index with the division between expansion and contraction is at 50 with the former above and the latter below.

*Quotations from the Institute for Supply Management website.

US Manufacturing: China redux

January was the first month where a positive impact from the US-China trade deal might have been seen. The coronavirus on the mainland has probably put paid to that hope. The widening sphere of quarantines and plant and office closures will have a profound effect on the Chinese economy and these will ramify around the world. China is the center of many manufacturing supply chains, whether providing parts, assembly or the complete process.

Bloomberg has estimated that businesses accounting for 69% of China’s GDP may stay closed until at least the second week of February. If accurate the hit to mainland and global GDP will be large.

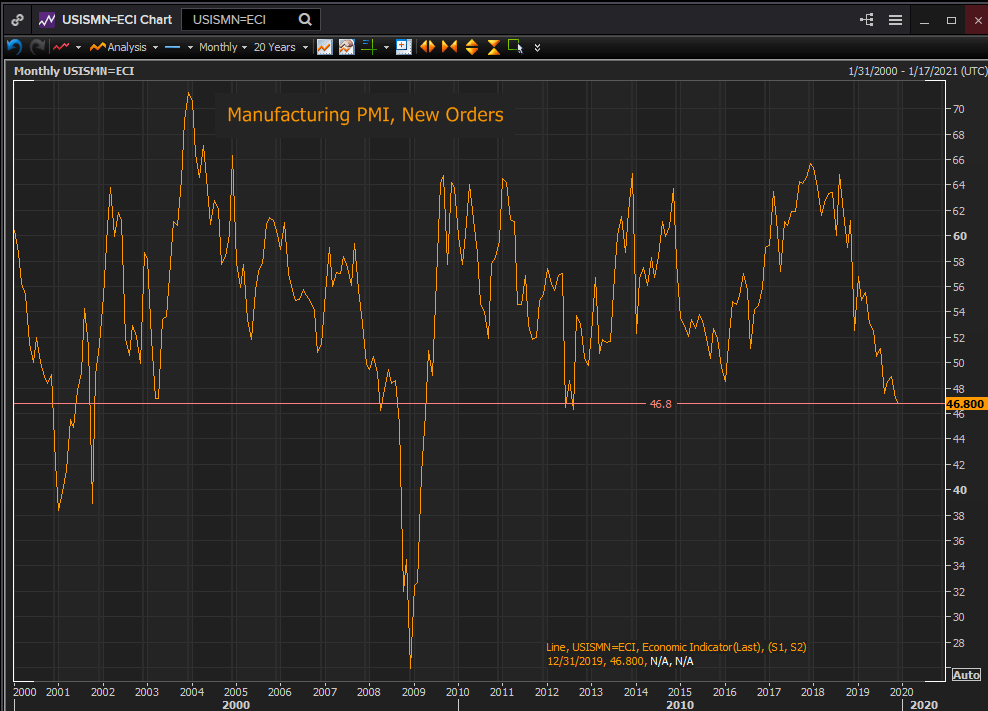

The manufacturing purchasing mangers’ index has been below the 50 contraction line since August and has not at least equaled the consensus forecast since June. The recession in manufacturing was worse than analysts anticipated even before the China health crisis.

The effect on new orders for US manufacturers which were at 46.8 in December, the lowest since August 2012, and new export orders, which slipped to 47.3 on the month from 47.9 in November, will be further damage. But with the sector and all major PMI components already negative, the impact on the overall economy of the 10%-12% engaged in manufacturing will be less than the dire headlines on the crisis.

Reuters

There is a possibility that once the crisis is past the recovery and the surge of delayed orders and replaced production will propel China’s economy and US manufacturing faster and higher than would have been the case otherwise.

Nonetheless, American manufacturing will not see a revival until the crisis is passed.

US Consumer Economy

Employment, job creation, wages and income have kept the consumer prosperous and the consumption economy vibrant. Payrolls, unemployment and average hourly earnings have provided households with the best income gains since the recession and these have flowed out into the economy. This coming Friday’s non-farm payrolls are expected to continue these trends.

Reuters

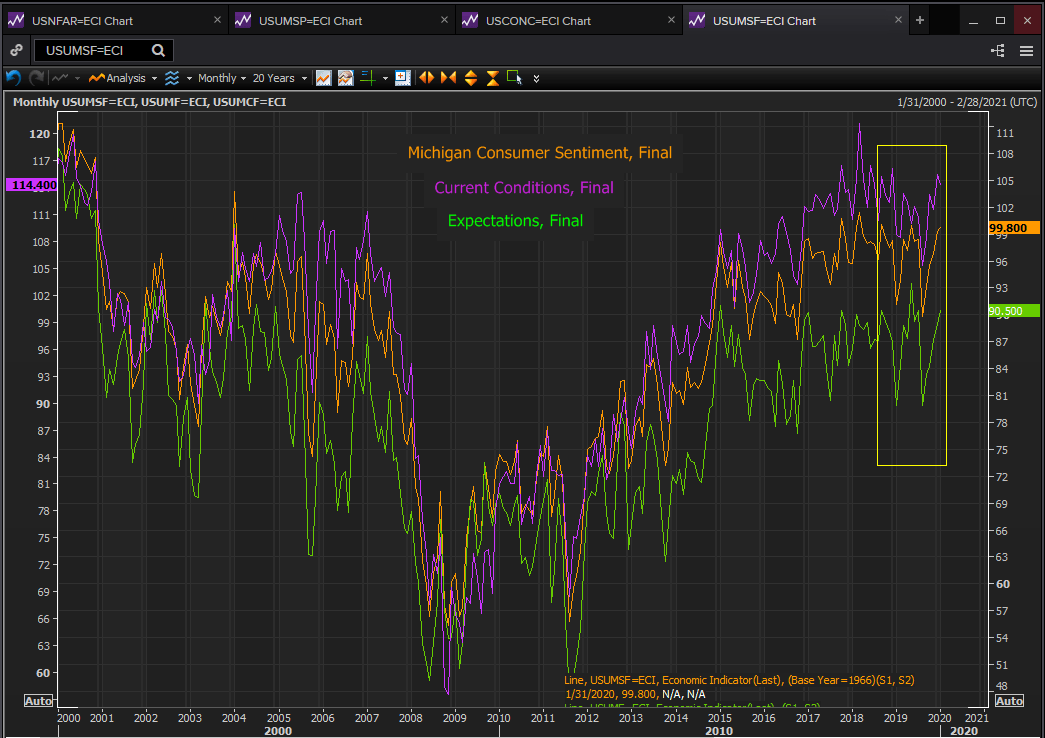

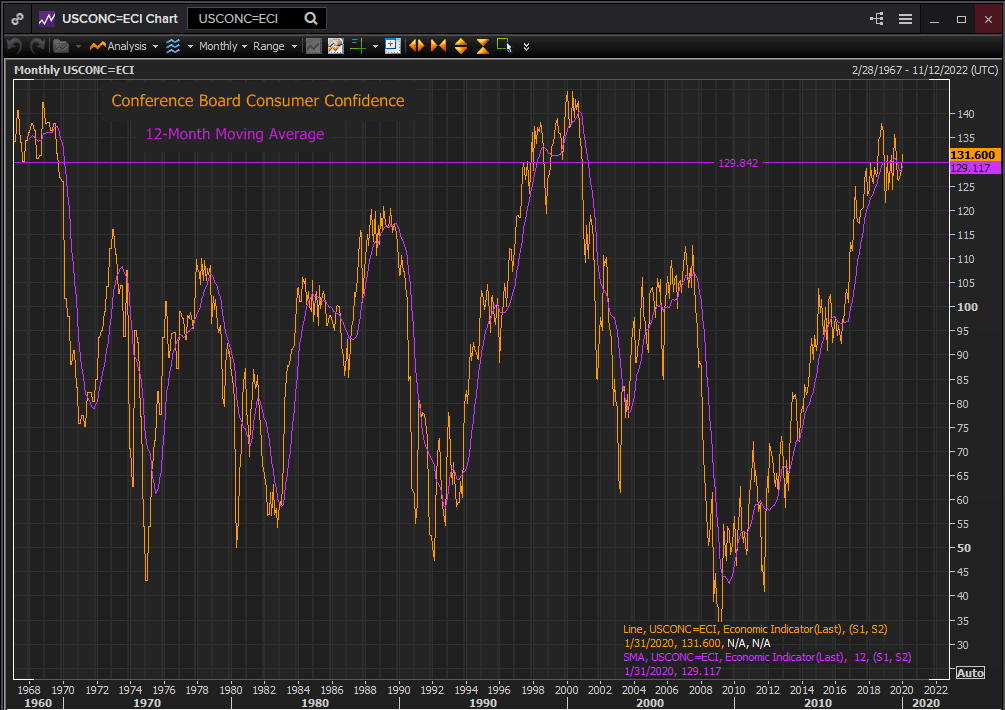

Consumer sentiment is strong with both the Michigan and Conference Board measures in the upper part of their three year ranges and among the best reading of the past twenty years.

Reuters

The labor economy story of the last three years is well known but its salutary effect on consumption and the economy giving both the depth to weather recent political storms from the US-China trade war to Brexit, impeachment and now coronavirus has been underappreciated.

It is because Americans are working that the world is a less baleful place than usual.

Conclusion

The end of the escalation phase of the US-China trade war will not deliver its benefit to either nation or their factories until the latest crisis is passed. That it is not economic in origin is unimportant, its effects will certainly be. The extent of the dislocation is unknown and will remain so until the spread of the illness is checked and reversed.

Chairman Powell alluded to the economic impact in his press conference on Wednesday and said the bank is ready to keep the US economy healthy.

The US dollar has seen some significant safe-haven gains over the past two weeks, Friday’s rise in the euro notwithstanding and excepting the yen which has its own safety status.

If the health crisis worsens concern will flow to the dollar whether or not US manufacturing sinks further into contraction.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.