US ISM Manufacturing June Preview: Expansion to continue but how severe is the labor shortage?

- US manufacturing expected to maintain strong 2021 expansion.

- Employment and New Order Indexes will be the focus.

- Markets anticipate US economic growth will continue to support the dollar.

American factories are having their best year in a generation and the main question is will the labor shortage short-circuit the expansion?

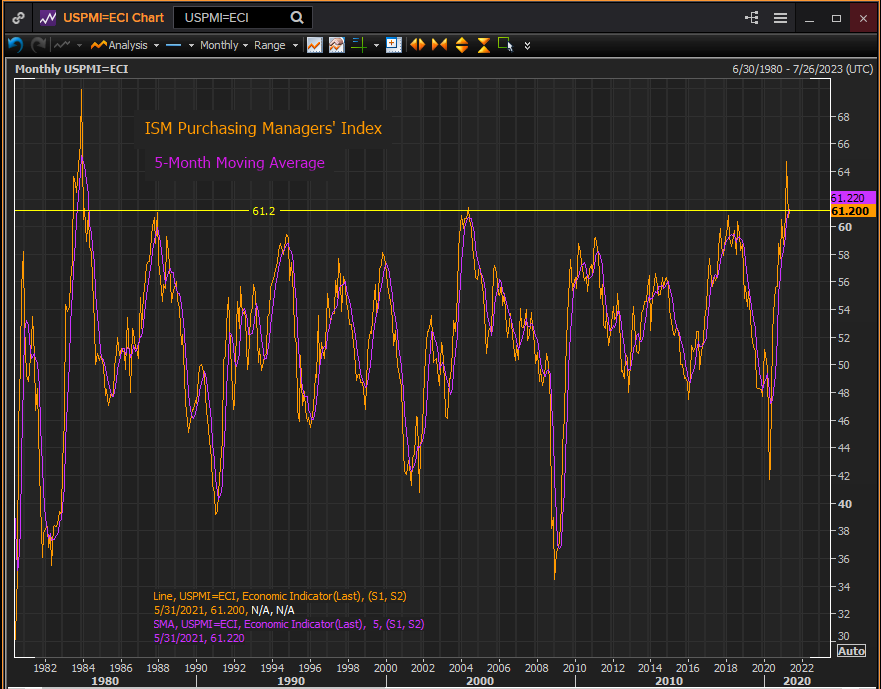

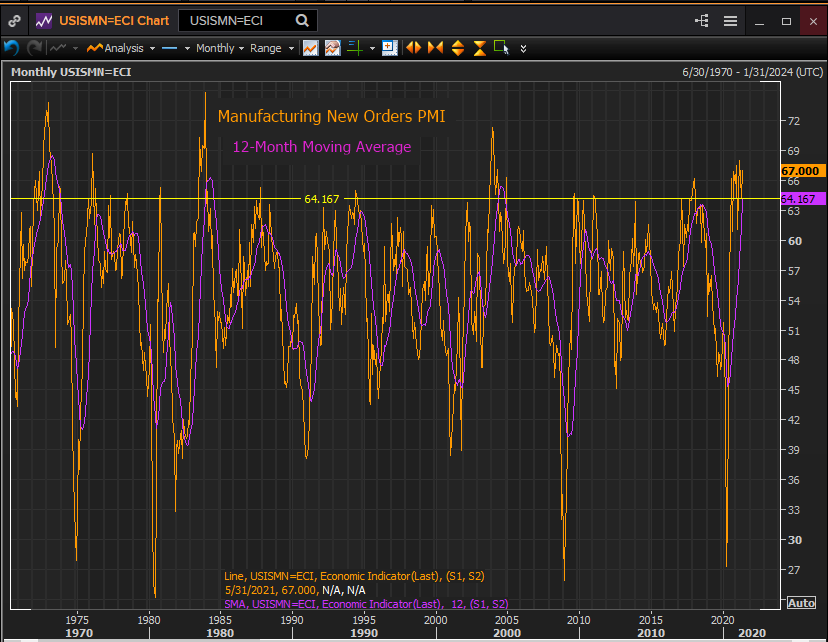

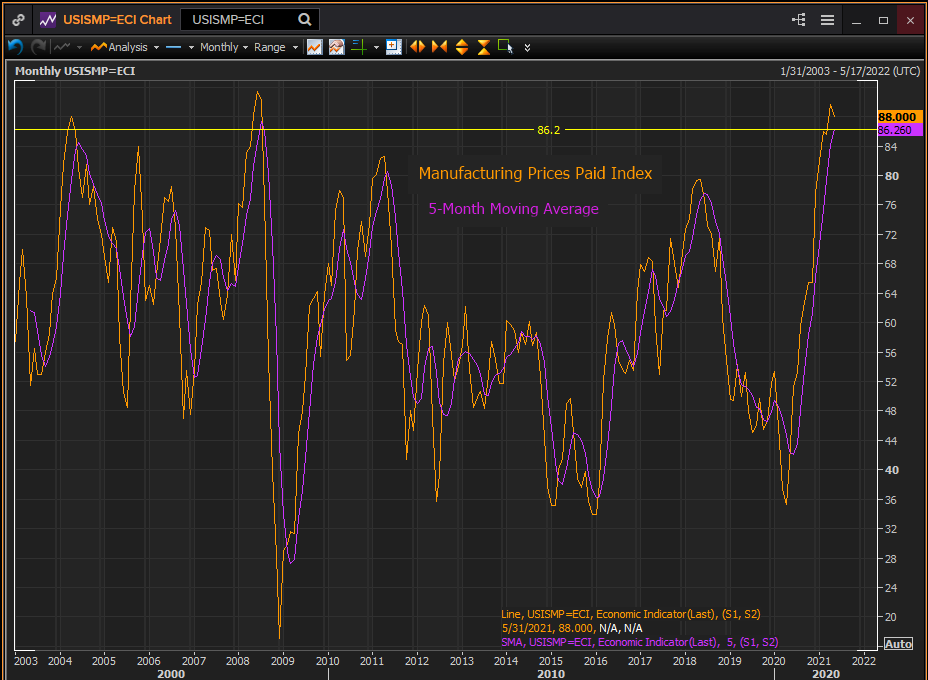

The Purchasing Managers’ Index (PMI) from the Institute for Supply Management is expected to show robust growth in June at 61, after registering 61.2 in May. The Prices Paid Index, which tracks the cost of manufacturing inputs, is forecast to slip to 87 from 89 in May. The New Orders Index was 67 in May and the Employment Index was 50.9.

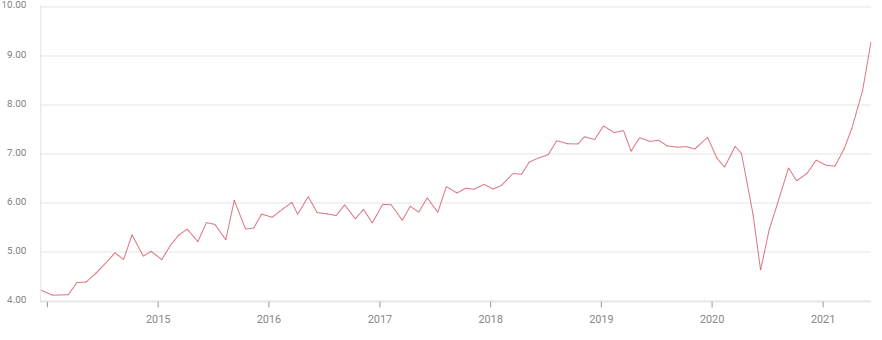

Manufacturing ISM

Sentiment in the US manufacturing sector hasn’t been this positive in 37 years. Overall PMI averaged 61.2 for the first five months of the year. You have to return to 1984 and the Reagan presidency to find comparable optimism.

Reuters

The business recovery that began last June has not slackened. The New Orders Index 12-month average of 64.17 has only been reached three times in 50 years, 2004, 1984 and 1973.

Reuters

Another near record is this year’s Prices Paid Index. At 86.2 it has only been equalled once before in the 18 years of this series, in 2008.

Reuters

The exception to the general manufacturing optimism has been employment. After soaring from 48.3 last November to 59.6 in March, the second highest reading in a decade, the Employment Index has fallen back to 50.9 in May. This is just above the 50 dividing line between expansion and contraction.

Reuters

The problem is not opportunity. The April Job Openings and Turnover Survey (JOLTS) had 9.3 million unfilled positions, up 1 million from March and the highest total in the 21 year history of the statistic.

Analysts have speculated the extended unemployment benefits that added $300 a month through September have made work at the lower end of the wage scale, especially in services, uncompetitive.

JOLTS

Another possibility is that skilled factory workers are in short supply after a generation of outsourcing manufacturing overseas.

US economic growth

All indications are that the US economy continues to accelerate as the country leaves the lockdowns behind and resumes normal activity.

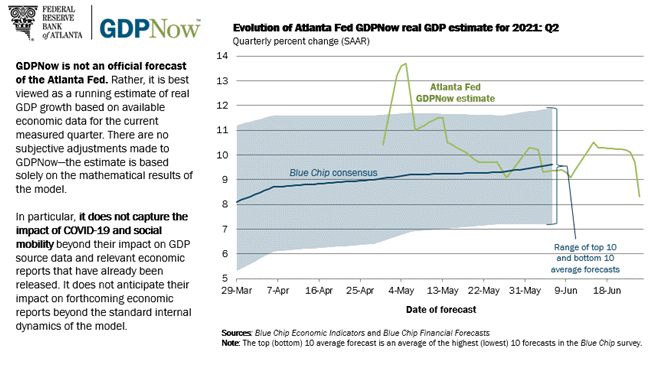

After expanding at a 6.4% annualized rate in the first quarter, estimates for second from the Atlanta Fed GDPNow model have ranged from 13.7% to the current 8.3%.

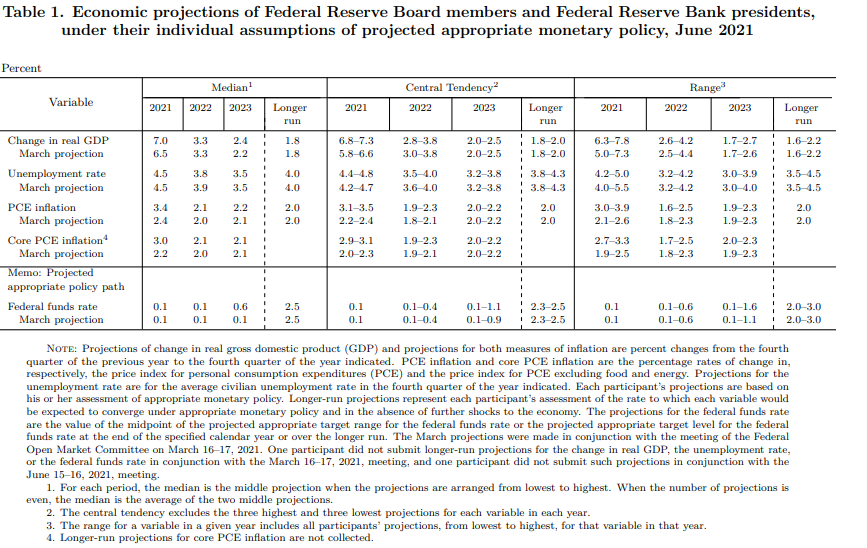

The Fed’s own projections, released at the June Federal Open Market committee (FOMC) meeting, posited 7% growth for the year up from 6.5% in March. If accurate it would be the highest rate of economic expansion since the 1980s.

Market view

Manufacturing is considered a leading indicator for the economy as a whole even though it is only about 12%-15% of US activity. Longer lead times for most production processes mean that factory managers must plan farther ahead than just deciding to hire an extra cashier.

Orders to the productive sector began to rise last June and have remained elevated as consumers catch up on defrayed spending and businesses attempt to stock for future expansion.

Market expectation is that the PMI figures will confirm the US economic expansion remains on track.

Employment is less important for future growth than New Orders.

As long as new business remains strong, employment will eventually catch up, even if it takes until the early fall after the expiration of the extended jobless benefits.

However, weak employment figures will add inflation pressures to the economy as firms compete for the few available workers. The Prices Paid Index is already at a 12-year high and just points below the all-time record of 87.38 from July 2008.

Conclusion

The expected June results with strong overall figures, weak employment numbers and high but contained price gains will be supportive of current market views of a rapidly expanding US economy with the dollar aided by rising or potentially rising Treasury yields and equities inhibited by the same.

Weaker than expected employment statistics and a higher than forecast price index are the main risks.

Labor shortages and climbing production costs tend to go together, employees are the largest cost item for most businesses, and they will exacerbate the fears of an earlier Fed bond program taper.

The dollar and Treasury yields could rise with inflation prospects but the market impact will be limited as PMI numbers are sentiment readings rather than actual economic data.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.