US Fourth Quarter GDP Preview: Variety is the spice of markets

- Annualized GDP in the fourth quarter expected to be 3.9% in the Reuters Survey.

- Dow Jones poll predicts 4.5%, Atlanta Fed GDPNow forecast at 7.5%.

- Retail Sales fell in fourth quarter, business spending increased.

- Fourth quarter indicates the strength of the economy entering the New Year.

- Dollar could see a boost from strong GDP numbers.

The possibility that the US economy could finish 2020 in the black, which would have seemed preposterous several months ago, is a distinct prospect when fourth quarter GDP figures are issued at 8:30 am EST on Thursday.

Predictions for the Commerce Department's advanced figures for annualized GDP range from 3.9% in the Reuters survey of economists to 7.5% from the Atlanta Fed GDPNow model.

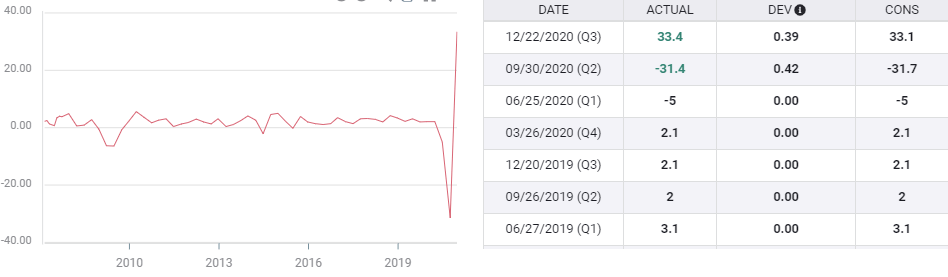

US Annualized GDP

If we use these forecasts as guides and average them with the three quarters released so far, Q1 -5%, Q2 -31.4%, Q3 33.4%, the rough estimates for last year's GDP range from from 0.225% to 1.125%. In a year of superlatives, this could add one more.

The final GDP figure for 2020 computed and revised by the Bureau of Economic Analysis is not just the average of the four quarters and will differ from that simple computation above. But if the fourth quarter is within said range, chances are at least reasonable that the year of COVID-19 will astonish yet again. Year-over-year the economy is expected to contract 3.5% in a poll of economists from CNBC/Moody Analytics.

Of more importance for markets is what the fourth quarter tells about the economy in 2021. Has the promise of vaccination given enough encouragement to business spending to sustain growth while the consumer recovers from the lockdown induced job losses and layoffs in November and December?

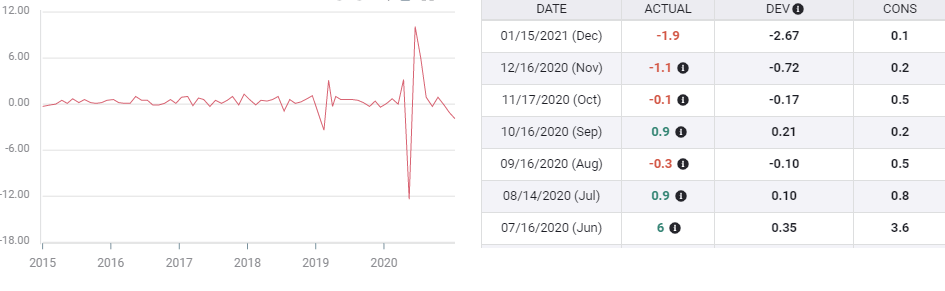

Retail Sales and Durable Goods

Consumer and business spending went in different directions in the fourth quarter. Consumption mirrored the declining fortunes of the job market.

Retail Sales dropped an average of 0.73% in the final three months of the year, the worst fourth quarter performance since the financial crisis, after rising 1.03% per in the third quarter.

Control Group Sales, which mimic the consumption component of the government's GDP calculation, declined 1.03% per month in the fourth quarter following a 0.5% gain in July, August and September.

Control Group

FXStreet

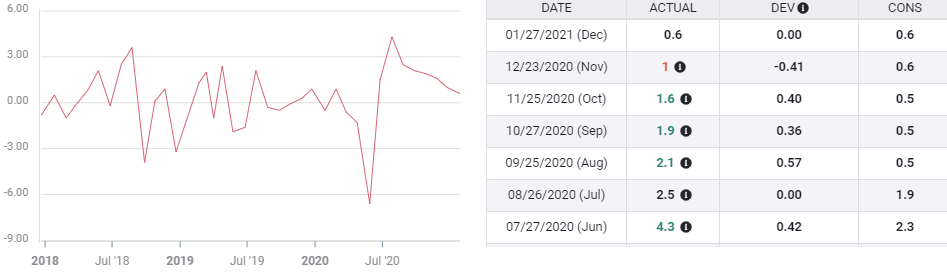

In contrast, businesses are gearing up for the recovery.

Nondefense Capital Goods, the Durable Goods category used as a proxy for business investment spending, rose 1.07% per month in the fourth quarter, less than half the 2.17% average in the prior three months but still a major addition to GDP. After falling a total of 8.5% in February, March and April business spending nearly doubled that at 15.5% in the next eight months.

Nondefense Capital Goods

FXStreet

US labor market

The labor market began to deteriorate in in the final two months of the year under the impact of a stringent lockdown in California, the largest state economy, and a partial closure s in New York, both now ended.

Initial Jobless claims in the first and last weeks of November were 711,000 and 716,000, the lowest of the pandemic. But the two middle weeks averaged 767,500 giving the month a run of 740,500. Even with weekly totals for half the month increasing sharply, November was still the seventh straight month of improvement and the average was 58,000 lower than October.

Claims has similar brief increases in July and in August that did not presage a rise in layoffs or a drop in hiring. At the end of November the health of the labor market was positive.

That changed in the first week of December when claims rose to 862,000. That was followed by 892,000, the most in two-and-a-half months. December's average jumped to 837,500, the highest in 12 weeks.

Nonfarm Payrolls reflected this deterioration in the labor market. Payrolls dropped to 336,000 in November from an average of 660,500 in September and October.

In December the market lost 140,000 positions, the first negative month since April and a reversal on the 71,000 forecast.

Claims have continued at a much higher pace in January averaging 870,000 for the three weeks through January 15 and are projected to be 878,000 on January 22 due on Thursday.

With layoffs continuing at a higher level in January than December, the current 68,000 estimate for this month's payrolls, to be issued on February 5, is optimistic.

Conclusion

Markets are looking ahead and if the fourth quarter presages a sturdy start to the year then the dislocations of 2020 will quickly fade. Strong business spending indicates continued faith in the recovery. The dollar's recent gains are positioning for better news from the US economy.

But as Fed Chairman Jerome Powell repeatedly observed on Wednesday after the decision to leave monetary policy unchanged, the main thing about the economy is getting the pandemic under control. That is the best growth policy.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.