US First Quarter GDP Revision Preview: The dollar wins

- First quarter GDP expected to be little changed after initial revision

- Consumer and business sentiment at odds with Q1 growth

- Second quarter growth predicted to decline sharply

The Bureau of Economic Analysis (BEA) of the US Department of Commerce will release its revision of 1st quarter annualized GDP on Thursday May 30th at 8:30 am EDT, 12:30 pm GMT.

Forecast

Gross domestic product is projected to decline to a 3.1% annualized rate in the first quarter after the initial release at 3.2%. The Commerce Department issues three GDP figures, the initial estimate, called advance by the BEA, followed by two revisions at one month intervals.

US Economy

Growth in the first quarter exceeded expectations by a substantial amount. Prior to the April 26th advance release the median estimate was for a 2.0% run in the first three months of this year. It was thought that growth would continue to decline as it had for three quarters, from 4.2% in the second quarter to 3.4% in the third to 2.2 in the fourth.

The surprise temporarily arrested concerns that the global economic slowdown, the trade dispute with China and various Brexit outcomes would inhibit the long-running US expansion. What was restrained in April has returned, particularly after the breakdown in US/China negotiations in early May.

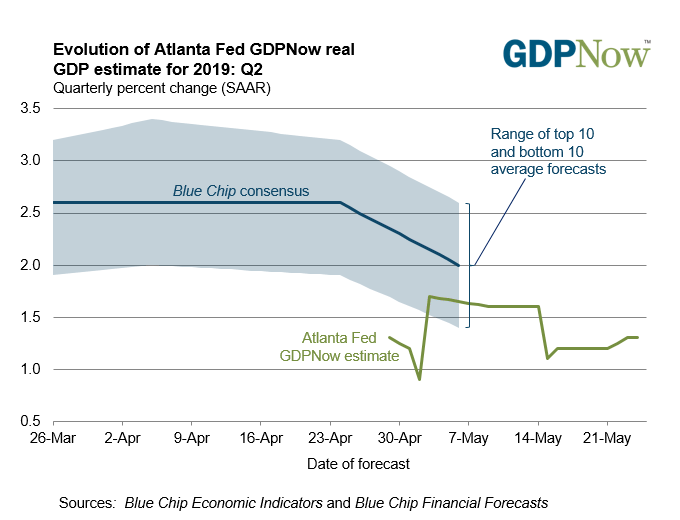

The latest estimats (May 24th) for 2nd quarter GDP from the Atlanta Fed GDPNow model is just 1.3%. The forecast will be updated on Friday May 31st following the release of April personal income and spending figures.

Consumer Sentiment, Retail Sales and Durable Goods

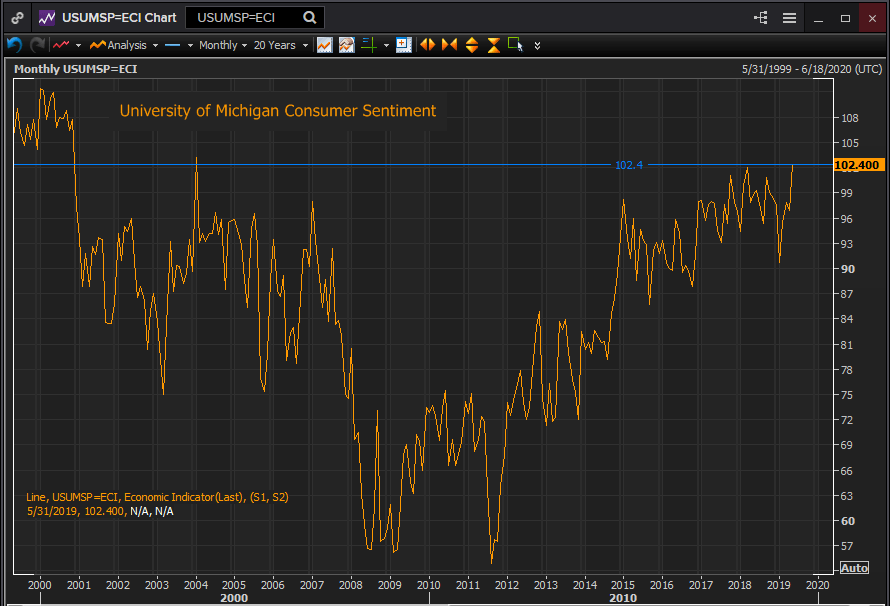

Optimism among US consumers in the second quarter has returned to some of its highest levels in two decades. The University of Michigan consumer sentiment index registered 102.4 in May its highest reading since January 2004 and its second highest since November 2000.

Reuters

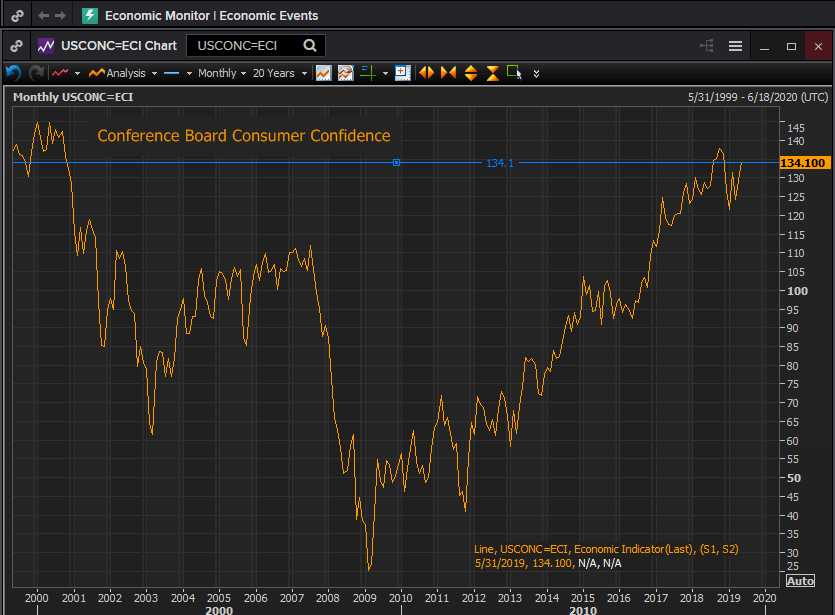

The Conference Board consumer confidence index was 134.1 in May. While not as outstanding as the Michigan Survey it is still among the highest scores of the past two decades.

Reuters

During the first quarter, however, things were not so sanguine. The Conference Board average in the first quarter was 125.8, the Michigan number 94.7, both scores being hard hit in January by the partial government shutdown.

The retail sales control group numbers, a proxy for the GDP contribution, were strong in the first quarter averaging an 0.8% monthly increase. But due to data reporting problems caused by the shuttering of part of the Commerce Department in January it is likely that the January sales numbers contained December receipts. December sales had fallen 2.2% the largest drop in 19 years and the largest December decrease on record.

Durable goods orders outside of the transportation sector, primarily the civilian aircraft business of Boeing Company of Chicago, were also lackluster in the first quarter averaging a 0.13% monthly gain..

Judging by the sentiment readings in the first quarter consumers saw reason to be cautious.

That makes the revisions to the March durable goods orders which fell from 2.6% to 1.7%, and the core capital goods business spending numbers down to 0.3% from 1.4% pertinent. Neither revised figures were included in the in original GDP estimate.

Business Sentiment

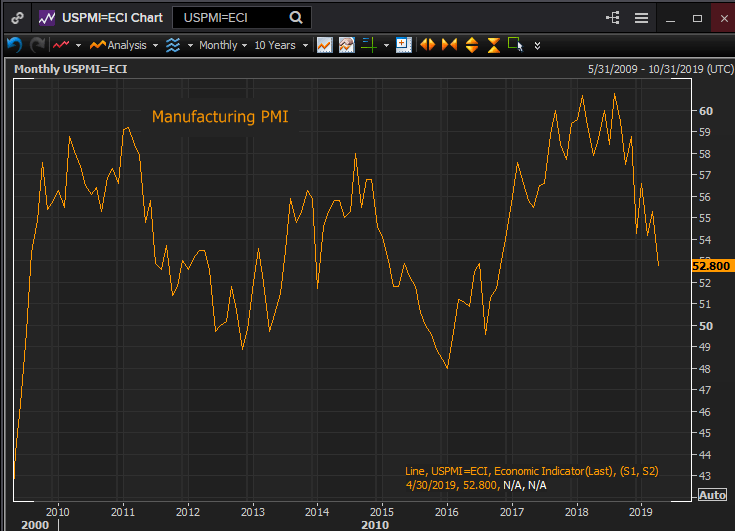

The purchasing managers’ surveys from the Institute for Supply Management in manufacturing in the first quarter saw some of their lowest reading to that point since the 2016 election. The new orders and employment indexes were stable in the first quarter but dropped sharply in April.

Reuters

Sentiment in the services sector held up better in the first quarter but in April it fell to its lowest level in almost two years.

Whether the cause of business hesitation is concern over the trade dispute with China, the global economic slowdown or simple cyclical caution after two excellent years its presence, coinciding with external conditions, means there is probably little upward adjustment coming from the business sector to add to GDP

Conclusion

Revisions to GDP are rarely large though the January shutdown and subsequent reporting confusion heightens the chance that something substantial was missed.

Given the depressed consumer sentiment numbers in the first quarter, the already declining business confidence figures, and the negative revisions to the March durable goods orders the risk is for a lower than expected GDP result.

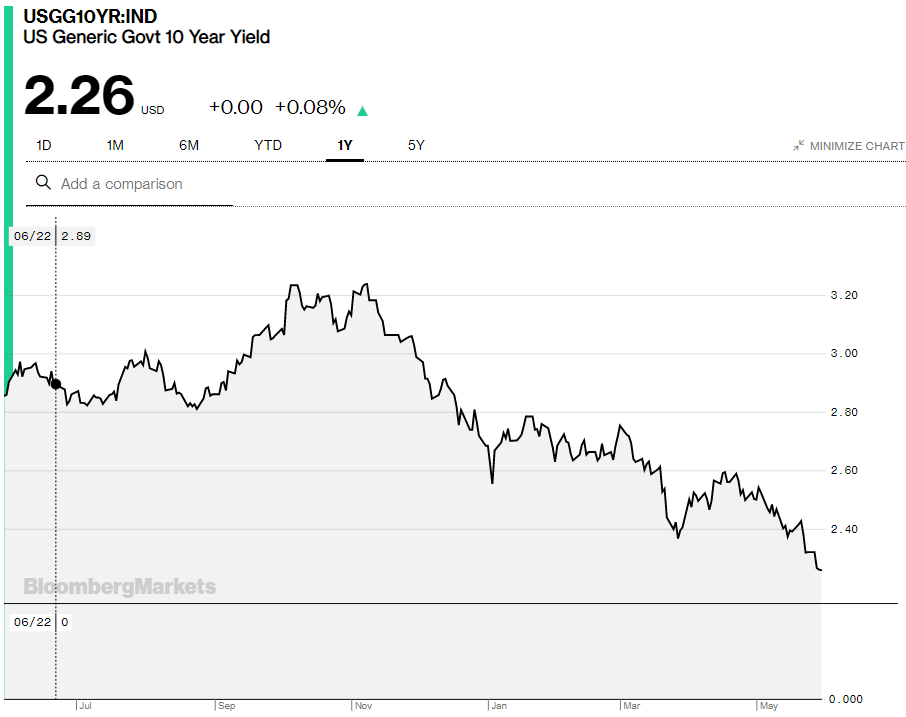

If such occurs US yields would continue their descent. The 10-year generic Treasury closed on Wednesday at 2.26%, five points from its 52 week low and 1% below its high last November. The 2-year finished at 2.11%, six points above its 12 month low and 86 below its high.

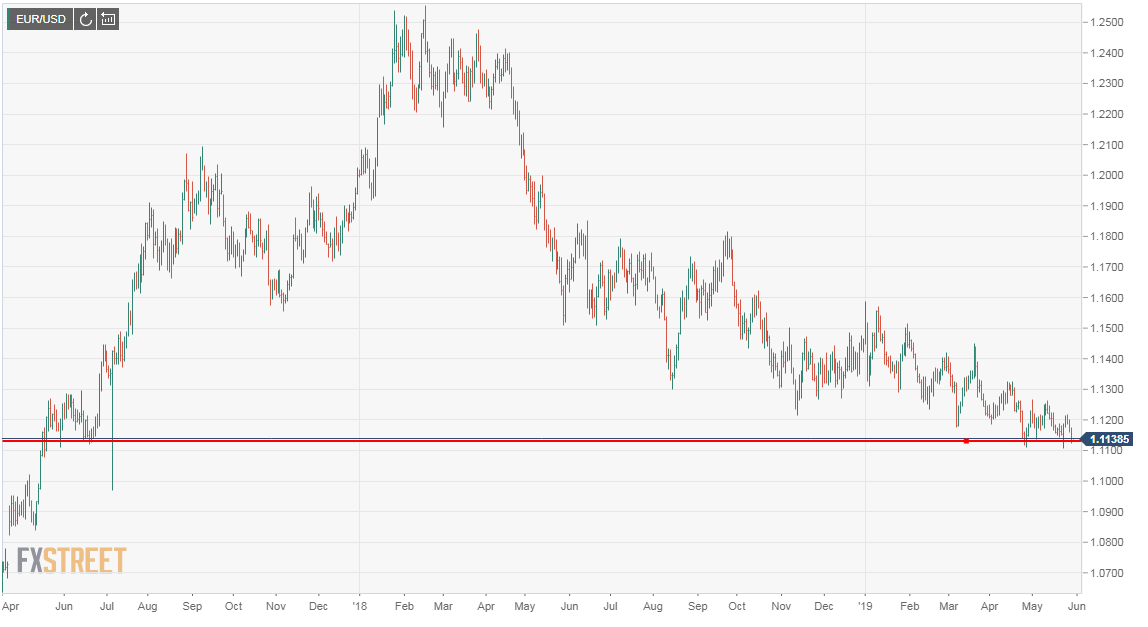

The dollar however would not. The US currency finished at 1.1131 against the euro on Wednesday, its highest versus the united currency in over two years.

The reason is simple. The dollar remains the preeminent safety destination. Yields are falling around the world. A weaker US brings global economic concerns to the fore. Markets are far more worried about a worldwide recession than competition in falling yields.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.