US equity nerves, it's not just interest rates

- Is an Omicron slowdown spreading in the US economy?

- Hiring and spending have been weak in November and December.

- Interest rates and inflation are sharply higher in the New Year.

Stock traders are worried. The three major US equity averages are down significantly this year and the Nasdaq has corrected from its November high.

There are concerns in spate. Economic growth is threatened. Supply chains are creaking, consumers are unhappy, interest rates, oil and consumer prices are rising and a Russian invasion of the Ukraine and attendant sanctions could tip the global economy into recession.

The Dow is off 5.86% this year and 6.89% from its record finish on January 4. The S&P 500 has shed 8.35% year-to date and 8.69% from its all-time high on January 3. The NASDAQ is down 12.53% in the New Year and 14.25% from its record last November 19.

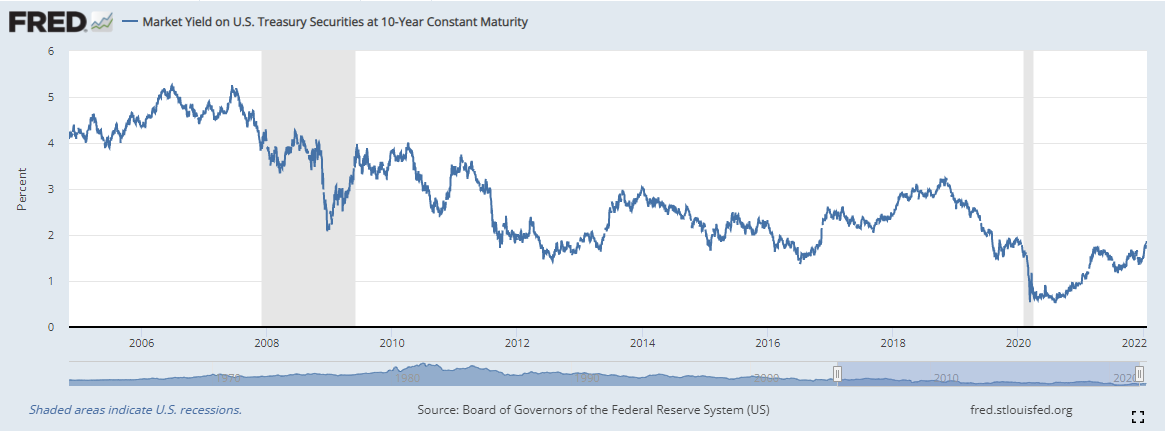

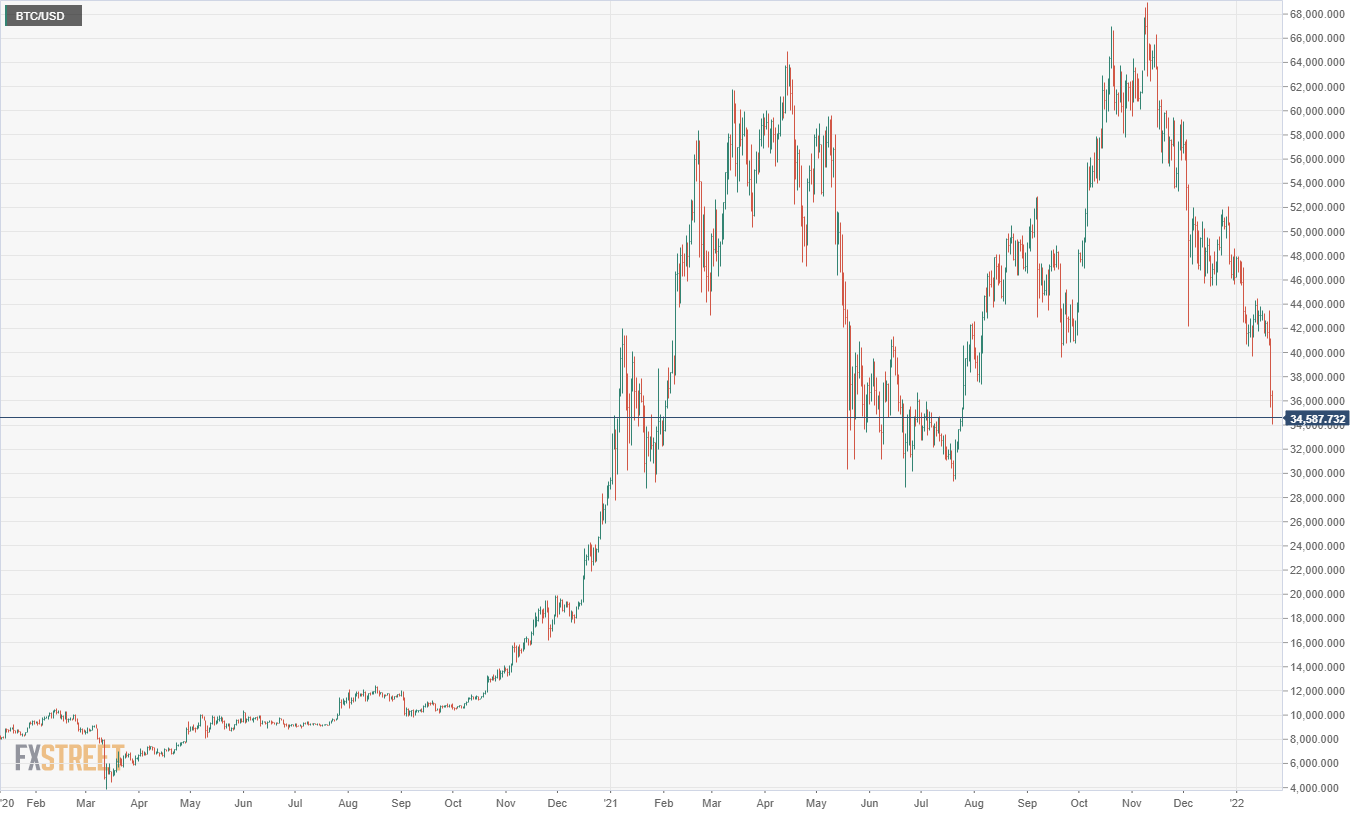

Treasury yields have pulled back from their midweek Federal Reserve inspired two-year highs but the 2-,10-, and 30-year Treasuries have jumped 28, 26 and 18 basis points respectively in the New Year. Even Bitcoin (BTC), that child of utopia and speculation, is riding to a mundane conclusion of its bubble excess.

NASDAQ

CNBC

Treasury yields in the US touched a two-year high this week with the 10-year reaching 1.902% on Wednesday but closed at 1.827% and then dropped to 1.771% on Friday, down 13 basis points in two days. The 2-year traded to 1.059% on Tuesday finishing at 1.038% and by Friday’s conclusion at 1.016% had lost just over four points. The yield on the long bond (30-year) topped at 2.19% on Tuesday and at the end of the week was at 2.085%, a 10.5 basis point loss.

Bitcoin (BTC) has been falling since its high close of 67,529.05 on November 8. Since then it is down 45.64% overall and 20.54% in the three weeks of January trading, including a 9.83% loss on Friday.

BTC

US economic conditions

According to a Reuters poll of analysts, the US economy expanded at a 5.6% annualized rate in the fourth quarter of 2021, more than double the 2.3% pace of the prior three months. The Atlanta Fed GDPNow model predicts that the expansion was 5.1%. The first fourth quarter Gross Domestic Product (GDP) estimate from the Bureau of Labor Statistics will be released on Thursday, January 27.

The question for traders and investors is not about growth in the final quarter or whole of 2021, but the direction of the economy in the first half of 2022.

How much has the omnipresent pandemic, inflation, shortages of labor and manufacturing components and supply chain misery, damaged economic growth and the willingness of consumers to spend and keep the expansion afloat.

Omicron restrictions have been largely restricted to mask wearing and, in a few cities like New York, mandatory vaccine papers for restaurants, gyms and other indoor public spaces. There have been no business closures and any economic effects were expected to be limited to lower levels of customer traffic.

Nonetheless there are signs that the US economy is slowing.

Retail sales were dismal in December, falling 1.9% and the three-month holiday season was flat at 0.1%. The Control Group, which mimics the consumption component of the GDP calculation, was even worse, down 3.1% in December and off 1.8% for the holiday period.

Consumer inflation reached a four-decade high at 7% in December. With the Producer Price Index (PPI) at 9.7%, there is more pain for US households ahead.

The Consumer Price Index (CPI) has been over 5% since last May. Wages from Average Hourly Earnings (AHE) lost 2.3% to inflation in 2021. For many lower-income American families, the burgeoning difficulties from inflation are considerably worse than the headline CPI rate. The expense of many items, from gasoline to steaks and used cars, has risen much faster than the general inflation rate. A gallon of regular gas, an inflexible necessity for most Americans, is up 47% from January 2021 and 58% from November 2020. Inflation has outstripped wages gains for most people. With no end to price hikes in view, the inevitable contraction of spending may have already begun.

Hiring was much weaker at the end of the year than expected despite the record number of unfilled positions. Nonfarm Payrolls added just 488,000 workers in November and December, barely half the 950,000 forecast.

Nonfarm Payrolls

FXStreet

Initial Jobless Claims have begun to rise. Filings for unemployment insurance were 286,000 in the January 14 week, far more than the 231,000 prior and the third increase in a row. Jobless filings have climbed 43% from 200,000 on December 24. They are still low by historical standards, but the increases likely indicate that the Omicron wave has not been without economic impact.

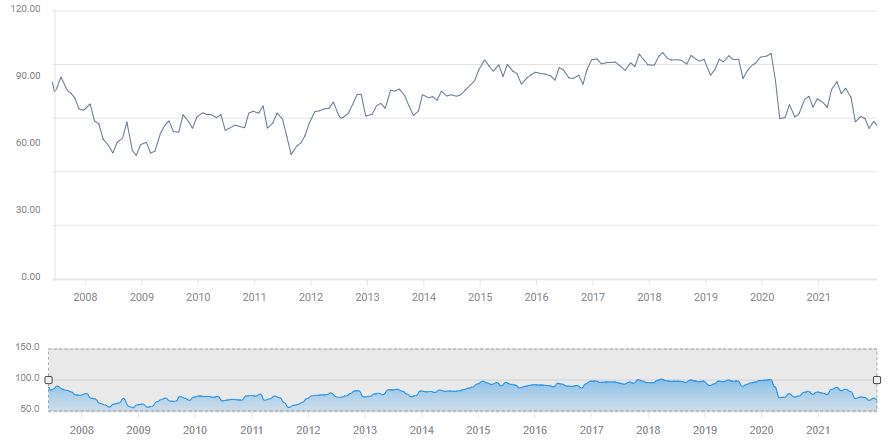

Consumer optimism has been mired at near-recession levels for six months. The Michigan Consumer Sentiment Index sank to 70.3 in August and has not recovered.

Michigan Consumer Sentiment

FXStreet

Fewer people working means less income generated for consumption. Unhappy consumers soon lose their incentive to bet on the future and spend. Inflation forces families into allocating more resources for the same or fewer goods. Real wages fell in 2021. If these trends are much prolonged the consumption basis of the US economy is threatened.

The economic keys are in the hands of US households. If consumers begin to restrict spending, the logic of the recovery quickly fades.

Conclusion

So far the equity decline has been largely about rising interest rates. The NASDAQ has fallen more than twice as much as the Dow and nearly as much compared to the S&P because its technology predominant makeup is heavily dependent on debt financing, the costs of which are suddenly much higher.

However, worries that the first signs of an economic slowdown have begun are rising fast.

A decline or halt in US economic growth, continuing weakness in job creation, rising inflation and layoffs, falling consumer spending, supply chain breakdowns, product shortages, the list of current problems is long. Any two of these are enough to undermine equities, all of them together are a formula for a market wide correction.

If the US economy falters in the first half, the equity sellers of the last two weeks will have been prescient.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.