US Durable Goods Orders November Preview: Consumers have the final word

- Durable Goods Orders forecast to rise 1.5% in November.

- Orders ex-Transportation expected to climb 0.6% after 0.5% in October.

- November Retail Sales added 0.3% following October’s 1.8% gain.

- Markets focused on inflation and Federal Reserve policy.

Americans have proved resilient against recurring waves of the pandemic and sharply rising inflation but the importance of the consumer to the US economy makes any sign of weakness in consumer related data of overriding interest.

Retail Sales rose 0.3% in November, less than half of the consensus forecast, after a strong 1.8% increase in October. It is likely that prospective product shortages coupled with surging inflation induced many shoppers to buy their holiday presents early.

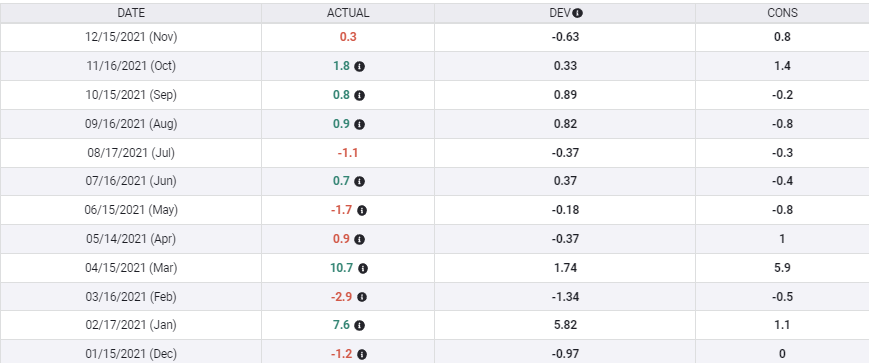

Durable Goods Orders are expected to climb 1.5% in November following a 0.4% drop in October and a 0.3% decline in September. Orders outside of the transportation sector are predicted to increase 0.6% after 0.5% and 0.7% gains in October and September. Nondefense Capital Goods Orders ex-Aircraft are forecast to rise 0.5% after October's revised 0.7% gain. Orders ex-Defense are projected to rise 0.1% following October’s 0.8% jump.

Nondefense Capital Goods

Durable Goods Orders and Retail Sales

Durable Goods are the Census Bureau's category of consumer and business products designed to last more than three years in normal use. Items range from commercial aircraft, to business software, automobiles and espresso machines. Purchases tend to be more expensive than everyday products and are considered by analysts to be a view into the long-term outlook of business managers and consumers.

Retail Sales have averaged 0.95% for the past four months. Except for the surges in January and March, artificially boosted by pandemic relief legislation, these are the best monthly figures since the original recovery immediately after the lockdowns last spring.

Retail Sales

FXStreet

That robust consumption should carry over into Durable Goods. The weakness in October and September Durable Goods Orders, -0.4% and -0.3% respectively, was largely due to the scarcity of new automobiles for purchase. Orders ex-Transportation rose 0.5% in October and 0.7% in September.

Nondefense Capital Goods

Nondefense Capital Goods Orders, the oft-used proxy for business investment spending, has been healthy averaging 0.83% for August, September and October and an identical 0.83% this year. Businesses appear to be preparing for a full-fledged recovery whenever it arrives, despite the vagaries of the pandemic and government policy.

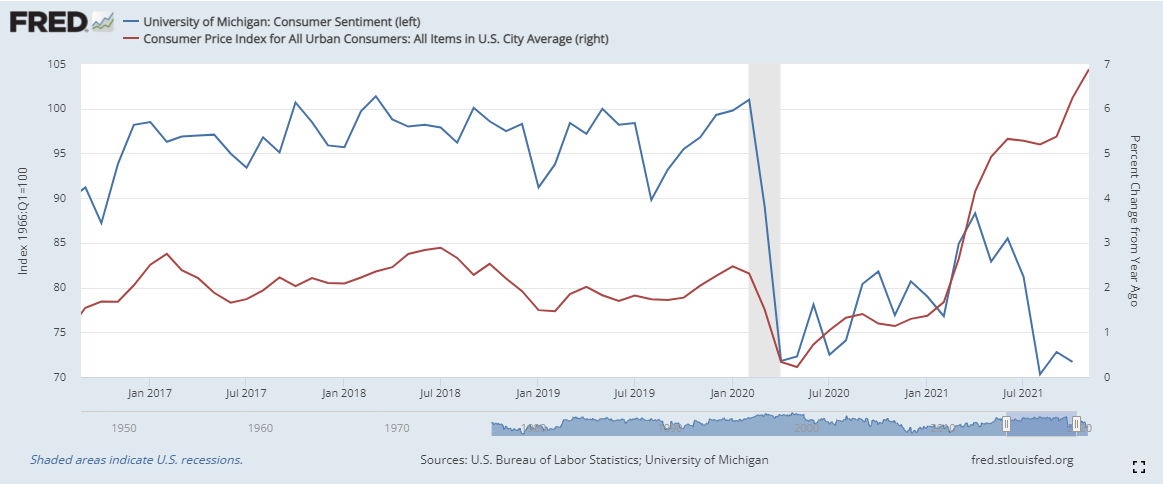

Consumer sentiment and inflation

Consumers are clearly upset by inflation but just as plainly that discontent has not been a drag on consumption.

One reason is that the job market remains exceptionally tight with over 11 million jobs on offer in October and record numbers of voluntary separations, meaning that people are leaving employment looking for better opportunities.

Michigan Consumer Sentiment registered 70.4 in December and has averaged 70.5 from August. Those are levels typical of 2009, 2010, and 2011 during the long recovery from the financial crisis.

There are no indications in the Michigan survey that US consumers are any closer to finding their good cheer.

Conclusion

As consumer discontent has not translated into weaker consumption, and Durable Goods orders are a subset of the already released larger retail category, markets will pay little attention to the November goods numbers.

The Federal Reserve balancing act, attempting to get control of inflation before rampant price increases damage consumer spending, will not be tested this month.

It will, however, be front and center in the New Year.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.