US Durable Goods Orders: Consumers, business hold steady in July

- Business orders stall after rising for four straight months and in 10 out of last 12.

- Overall Durable Goods Orders fall on commercial aircraft decline.

- Orders ex-transport gain more than forecast, alleviating some consumption concerns.

- Market response minimal with Federal Reserve symposium and Powell speech awaited.

The unexpected weakness in July Retail Sales did not carry over into Durable Goods Orders suggesting that the August collapse in Consumer Sentiment may not foretell a death knell for US consumption.

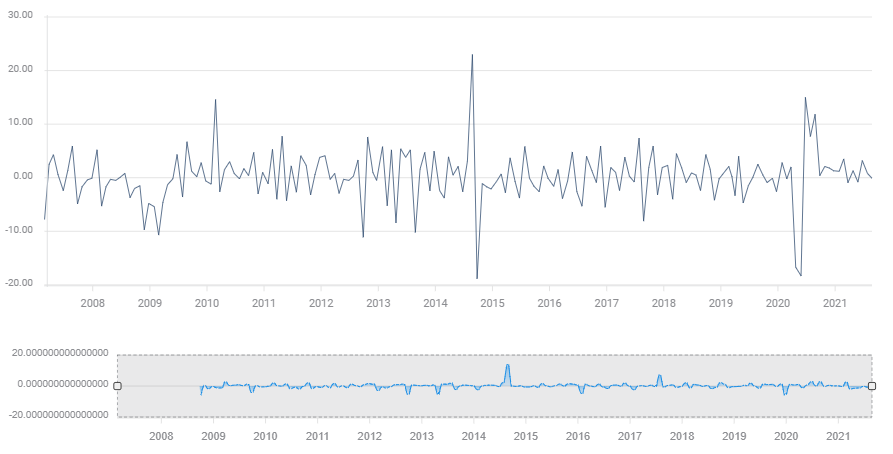

Durable Goods Orders dropped 0.1% in July, slightly better than the -0.3% forecast and the prior month was left unchanged at 0.8%. The decline was largely due to a 49% fall in commercial aircraft orders following a 4.7% gain in June and a 50.7% jump in May. Boeing Company of Chicago reported 31 new bookings in July, after receiving 219 in June.

Durable Goods Orders

Orders excluding the transportation sector, a better judge of consumer intent than the headline number because of the aircraft complication, rose 0.7%, beating their 0.5% prediction and June’s total was revised up to 0.6% from 0.3%.

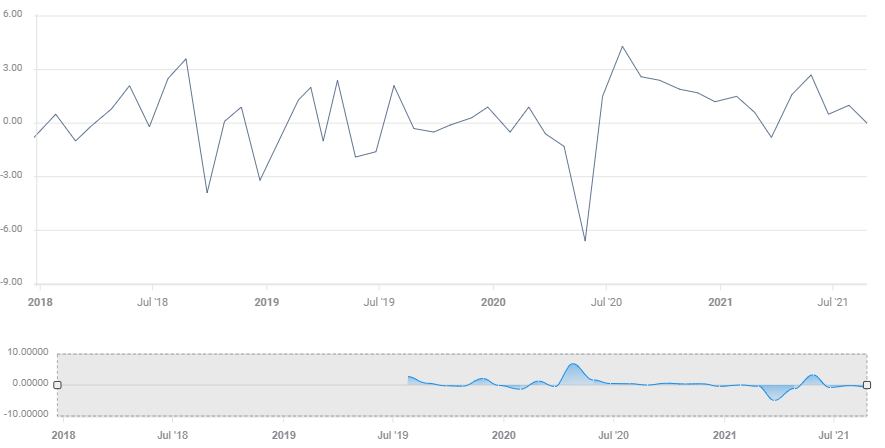

Nondefense Capital Goods Orders, the business investment proxy, were flat on the month, with June also doubling to 1% after adjustment.

Nondefense Capital Goods

FXStreet

Retail Sales for July, reported on August 17, had unexpectedly fallen 1.1%, more than three times their -0.3% projection, fomenting speculation that the subset of Durable Goods Orders would also falter.

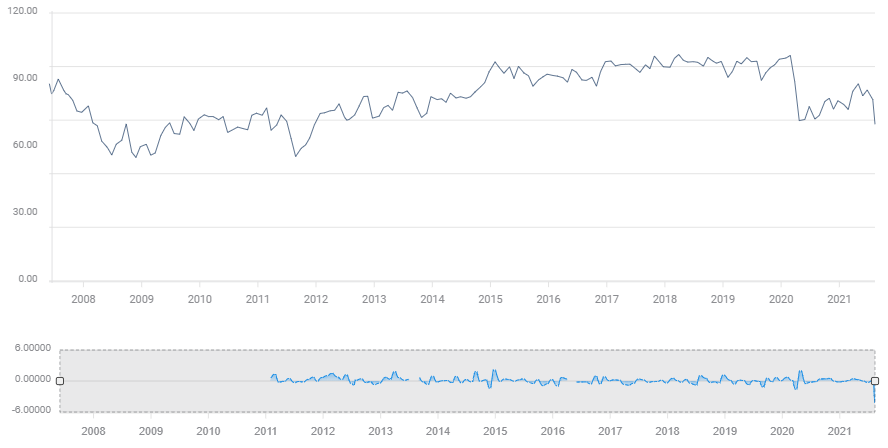

Consumer Sentiment

The precursor for both the consumption results had been the Michigan Consumer Sentiment Index for August, issued two days before the July Retail Sales figures. Consensus estimates had had the number unchanged at 81.2 from July.

Instead the index collapsed to 70.2, beneath than the prior pandemic low of 71.2 in April 2020. It was the weakest for this confidence index since December 2011 and one of the largest single-month declines on record.

Michigan Consumer Sentiment

FXStreet

Durable Goods vs Retail Sales

Going into the Durable Goods numbers the concern was that if the sharp drop in Retail Sales was confirmed by the Durable Goods Orders, items that necessarily force the consumer to take a longer economic view, with the Michigan Index at 81.2 in July, what might the plunge to 70.2 presage for August Retail Sales?

While the better than expected Durable Goods Orders ex-transport for July result does not wholly alleviate the possibility that August’s Retail Sales will drop sharply reflecting the sentiment numbers, it does mean that consumers were not averse to assuming new long-term financial commitments.

Durable Goods Orders track purchases meant to last three years or more in normal use. On the consumer side, many of these items are bought on time, involving credit arrangements lasting several years.

For example, because car loans usually last five years, car purchases are thought to provide an insight to how consumers view their long-term financial prospects.

This is a different equation than overall Retail Sales which mostly involve immediate payment.

Business investment

Business spending has been on the bright spots of the recovery remaining at a steady pace as firms large and small replace equipment and upgrade services in anticipation of a strong recovery.

Nondefense Capital Goods order may have been unexpectedly flat in July but they rose for the four straight months prior and have averaged a 0.4% monthly gain for the previous half-year and 0.6% since July 2020.

Nondefense Captial Goods

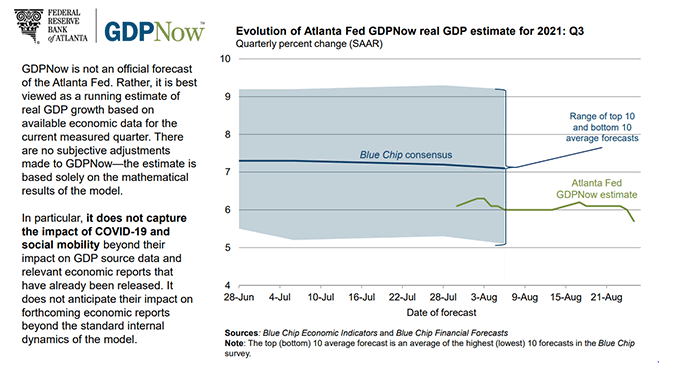

Gross Domestic Product (GDP) expanded 6.3% on an annualized basis in the first quarter and 6.5% in the second, making the first half of the year the strongest in a generation. The latest forecast from the Atlanta Fed GDPNow model is 5.7% for the third quarter.

For the US economy which is about 70% dependent on consumer spending, sentiment and sales are required ingredients for success.

Conclusion

Durable Goods Orders elicited no response from the credit, currency or equity markets.

Attention is firmly fixed on the latest instalment of the Federal Reserve’s long-running rate saga, the annual Jackson Hole symposium that begins on Thursday, and Chair Jerome Powell’s speech at 10:00 am on Friday.

Speculation is rife that the bank and its officials will use this non-policy event to hint at the timing for a reduction in the Fed’s $120 billion a month of bond purchases that have kept US interest rates near their historical lows since March 2020.

Some observers expect that the taper could be announced at the September 21-22 FOMC meeting, with broad hints in comments from Fed officials at the symposium and in Mr. Powell’s remarks, perhaps contingent on the August Nonfarm Payrolls due on September 3.

Others anticipate that rising covid case loads, the hesitation evident in the August plunge in consumer sentiment and the global impact of the botched Afghanistan evacuation may incline the governors to several more months of caution.

Either way, the July consumption figures were decidedly old hat.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.