US Dollar: Looking for the next trend

The major currencies against the US Dollar have been without trend for nearly six months. Trading ranges have been shrinking and volatility falling.

Last year’s dollar ascendancy in the first three quarters was based on three pillars, the Federal Reserve's tightening policy, a strong American economy and an intermittent safety hedge. It is obsolescent. The Fed has paused its rate hikes, the US economy is showing signs of fatigue and the fears of a trans-Pacific trade war and a no-deal Brexit have subsided though they are not gone.

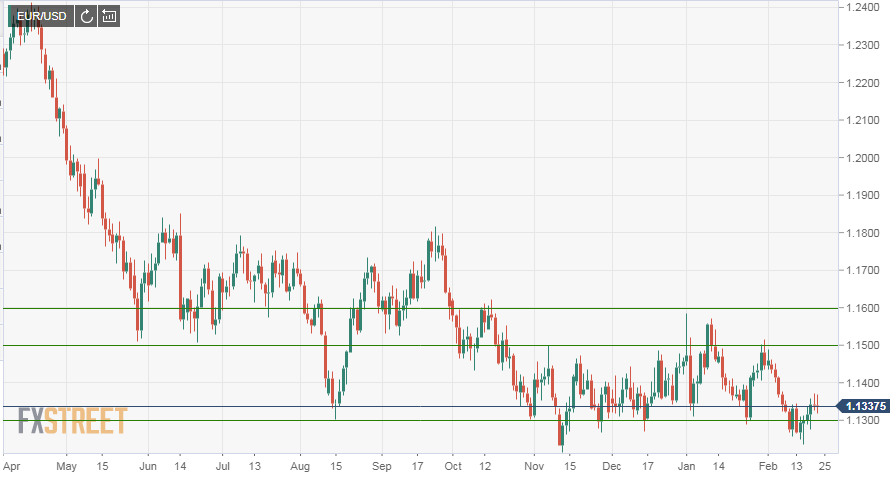

Since early October the euro has moved in a three figure range between 1.1600 and 1.1300. For most of that period the range was narrower, 1.1300 to 1.1500 with short-lived excursions outside. The 407 point absolute range point is about 3.5% of the mid-rate at 1.1450.

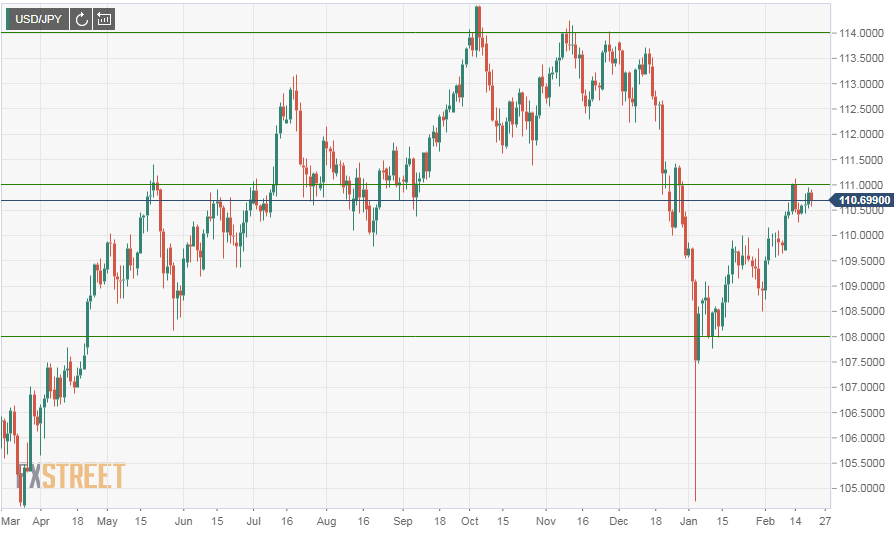

The yen has had a greater overall range 114.00 to 108.00 but the range is split neatly in half. From October to late December the distance was 114.00 to 112.00 and in the New Year 111.00 to 108.00. Even so the absolute range is about 6.4% of the 111.00 midpoint.

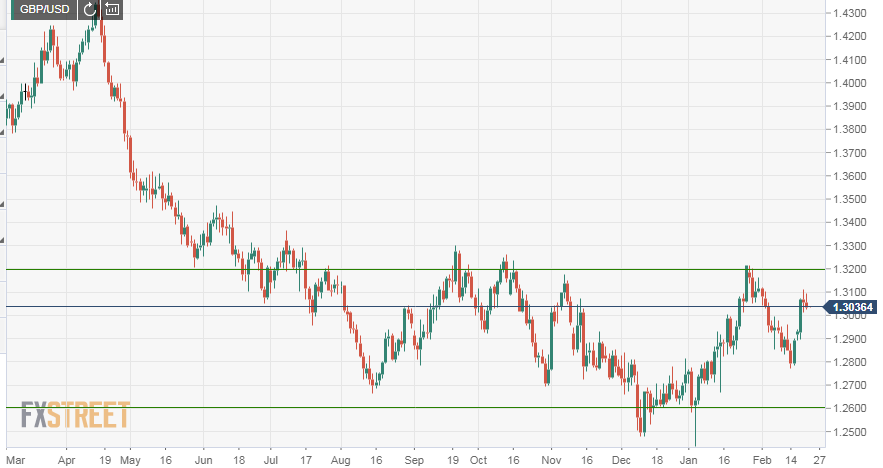

Sterling traded between 1.3200 and 1.2600 for the bulk of the period with the rise and fall largely determined by the vagaries of the Brexit negotiations.

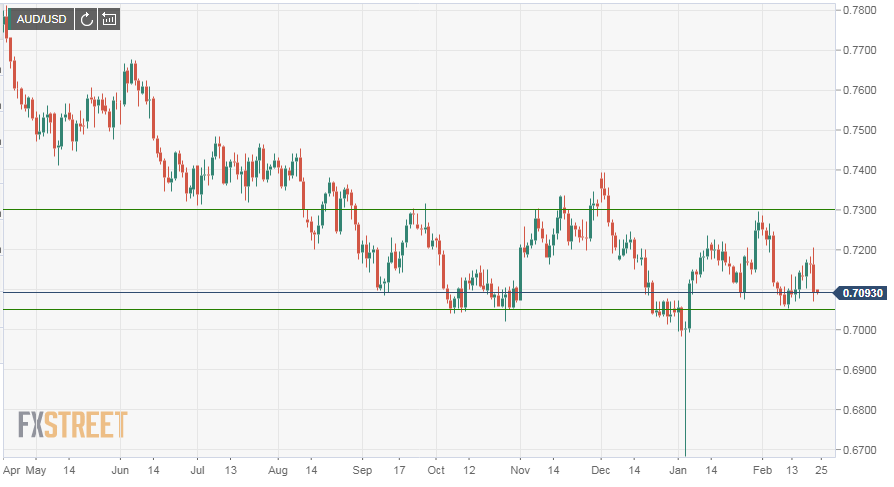

The Australian Dollar and the New Zealand Dollar have been even more restricted. The aussie shifting between 0.7300 and 0.7050 and the kiwi between 0.6900 and 0.6700.

The apparent weakening of the dollar’s supports has not produced a reversal for the US currency but only a pause. The evolution of Fed policy, the US-China dispute, Brexit and the expansion of the American economy may again provide solid reasons for buying the dollar. It depends on how these issues play out.

To quote the Federal Reserve, “In light of global economic and financial developments and muted inflation pressures, the Committee will be patient as it determines what future adjustments to the target range for the federal funds rate may be appropriate…”

Patience is not a change in policy. As the Fed noted its rate policy will be determined by the state of the US and the global economies. It is not inconceivable that a resurgent US expansion backed by a healthy world environment will elicit two rate increases in the second half of the year.

Such is not the current market assumption. It should be remembered that the Fed’s policy over the last three years was not based on forestalling inflation or economic excesses but on returning rates to a more historic level. The stated goal was normalization, to provide a cushion for reduction when the next recession arrives.

The governors have retreated from hikes whenever they might have threatened economic growth. They have also resumed increases when the economy has been judged strong enough to support them. There is no reason to assume that the governors will not want to augment their recession armory with higher rates if they can be safely obtained.

The comparison with the ECB’s rate policy, which just ended its bond program and liquidity support of the euro zone economy is instructive.

Mario Draghi and company know that when the next recession occurs their only option will be another bond program that will drive European rates even further into the negative, with unknown long term effects on economic growth and prosperity.

They did not withdraw support because the economic and political situation did not permit them to do so, not because the current rate structure is ideal. European rates are not at the neutral bound. Negative rates are not normal.

The key factor for all parties is the US-China trade dispute. The potential for a trade pact to drive expansion in both countries is great. Together the world’s two largest economies can promote sufficient global growth to make Brexit’s economic dislocations, if they occur, superfluous.

If a substantial agreement is signed between the two nations the resulting surge in growth in the US and China and the accompanying rise in business and consumer sentiment could bring the Fed back to its original intentions.

Even without active acknowledgement from the governors a strengthening US economy will move market speculation to dollar promotion.

Like Fed policy the six month outcome for the dollar is reality based.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.