U.S Dollar Looking for a Toe Hole

Europe’s single currency and regional equities remain on firmer footing as Asian data lends the global growth story more momentum. U.S Treasury prices trade steady after yesterday’s drop, while gold prices are little changed.

The EUR (€1.2233) has somewhat dismissed the European Central Bank (ECB) attempts to talk the currency down this week, while the ‘big’ dollar continues its efforts to hold onto yesterday’s advance. The U.S 10-year Treasury yields remain steady atop +2.60% amid speculation Congress will avert a government shutdown.

Today’s agenda: Data stateside is expected to show that U.S housing starts probably slipped last month for the first time in three-months as frigid winter weather impeded work (08:30 am EDT). Elsewhere, central banks in Indonesia, Turkey and South Africa are all expected to keep policy unchanged.

1. Stocks record new records

In Japan, the Nikkei ended lower after hitting a new 26-year high overnight. The Nikkei dropped -0.4% as investors turned cautious. Both real estate stocks and financial firms underperformed.

Down-under, Aussie shares slid to a fresh five-week low, pressured by noted profit taking in heavyweight miners BHP Billiton and Rio Tinto. Faltering a second day running amid broad local weakness, the S&P/ASX 200 fell -0.5%. In S. Korea, the KOSPI traded effectively flat.

In Hong Kong, Hong Kong stocks rallied overnight to fresh new highs, led by telecommunications and financial firms. The China Enterprises index extended gains after data showed China’s Q4 economic growth beats expectations. At close of trade, the Hang Seng index was up +0.43%, while the Hang Seng China Enterprises index rose +1.76%.

Note: China’s economy grew +6.8% in Q4, helped by a rebound in the industrial sector, a resilient property market and strong export growth.

In China, banking and infrastructure firms power China stocks to a two-year high. The Shanghai Composite index was up +0.91%, while the blue-chip CSI300 index was up +0.58%.

In Europe, regional indices trade mixed with notable strength in DAX following on from a strong close yesterday stateside – the Dow settled above the psychological +26K for the first time.

U.S stock futures are expected to open in the ‘red’ (-0.1%).

Indices: Stoxx600 +0.1% at 398.5, FTSE -0.3 at 7702, DAX +0.4% at 13235, CAC-40 +0.2% at 5504, IBEX-35 -0.1% at 10463, FTSE MIB +0.3% at 23575, SMI flat at 9439, S&P 500 Futures -0.1%.

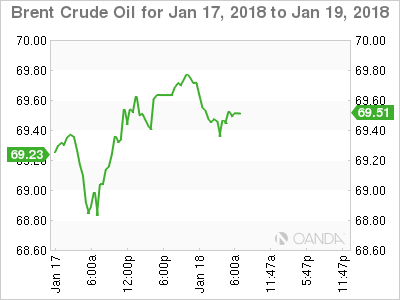

2. Oil holds near three-year highs, supported by threat of Nigeria attack

Oil prices are holding steady ahead of the U.S open, supported by falling inventories of crude and threats of an attack on Nigeria’s petroleum industry, despite a reported rise in U.S fuel supplies weighed.

Crude is within sight of its three year highs, supported by supply cuts led by the OPEC and on concerns that unrest in producer nations such as Nigeria could further curb output.

Note: Militant group Niger Delta Avengers (NDA) has threatened to attack Nigeria’s oil sector in the next few days, potentially hampering supplies in Africa’s largest exporter.

Brent crude futures have slipped -7c to +$69.31 barrel. On Monday it hit +$70.37, the highest since December 2014. U.S crude is up +2c at +$63.99 and reached it’s highest price in three-years on Tuesday.

Note: Yesterday’s API supply report presented a mixed picture, with inventories of gas and diesel rising and crude stocks falling.

Expect investors to take directional clues from today’s U.S government’s weekly supply data (10:30 am).

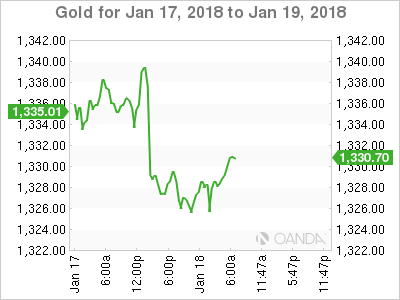

Gold prices trade a tad lower as the as dollar gains on stronger U.S. data. The ‘yellow’ metal has hit its lowest in nearly a week, as the dollar edged higher from three-year lows on stronger-than-expected U.S. economic data. Spot gold is down -0.1% at +$1,326.11 per ounce.

3. Sovereign bond yields climb

The U.S 10-year Treasury yield has hit its highest print since March 2017 at +2.60% in overnight trading. This rally higher has managed to drag along its European counterparts sovereign yield curves.

Note: The yield on the two-year U.S note, which is considered to be especially sensitive to expectations for interest-rate increases from the Fed, settled last week above +2% for the first time in a decade.

Investors will now get a look at data on U.S housing starts and jobless claims (08:30 am EDT), as well as comments from multiple Federal Reserve officials for further directional yield clues.

In Germany, the 10-year Bund yield is trading atop of its six-month high at +0.52%, while in the U.K, the 10-year Gilt yield has advanced +2 bps to +1.33%.

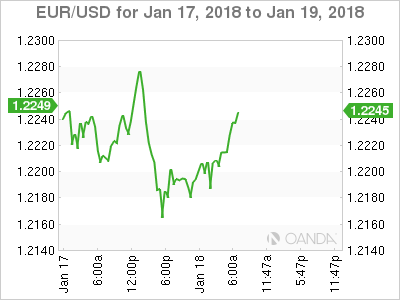

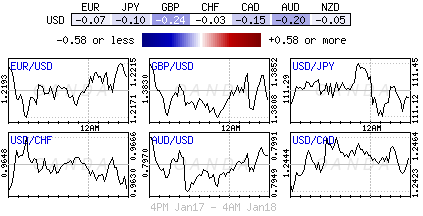

4. Dollar looking for a toe hole

The U.S dollar is a tad weaker versus G10 currency pairs despite higher Treasury yields – U.S 10-year yields have moved above the psychological +2.60% level to print a new 11-month high.

The EUR/USD (€1.2212) is hovering just above key support levels in a quiet European session as investors’ assesse the ECB’s recent rhetoric. The ‘single’ unit is off its recent three-year high print as market participants contemplated whether ECB’s Draghi would push back against EUR’s strength during his press conference next week following the ECB’s policy meeting.

Note: Several Governing Council members of the ECB are set to speak today.

Elsewhere, the sterling has rallied less than +0.05% to £1.3834, hitting the strongest in 19-months. The U.K’s House of Commons has approved the E.U Withdrawal Bill in its third reading (as expected) with vote at 324 to 295. The Bill will now be reviewed by the House of Lords, which could ask for more changes.

USD/JPY (¥111.28) is hovering above key support as some at BoJ officials are said to be seeking future normalization talks.

In South Africa, a sounder political backdrop has seen the rand surge – ZAR has climbed +0.4% to $12.2493, the strongest in more than two-years.

5. China’s 2017 GDP growth accelerates for first time in seven years

Data overnight indicated that China’s economy expanded by +6.9% in 2017, growing at a faster annual pace for the first time since 2010.

The country’s economy grew by +6.8% y/y in Q4 2017, beating a +6.7% consensus increase forecast.

Digging deeper, the GDP growth was largely helped by strong investment momentum, especially in infrastructure and real estate, and partly by improved trade performance.

Nevertheless, China’s domestic demand is expected to be the biggest factor that drags down economic growth this year while external demand may increase.

Note: Investment in infrastructure projects and the property sector – which helped fuel 2017 activity, is expected to experience a sharp slowdown in 2018.

Author

Dean Popplewell

MarketPulse