US Data Preview

USDindex, Daily

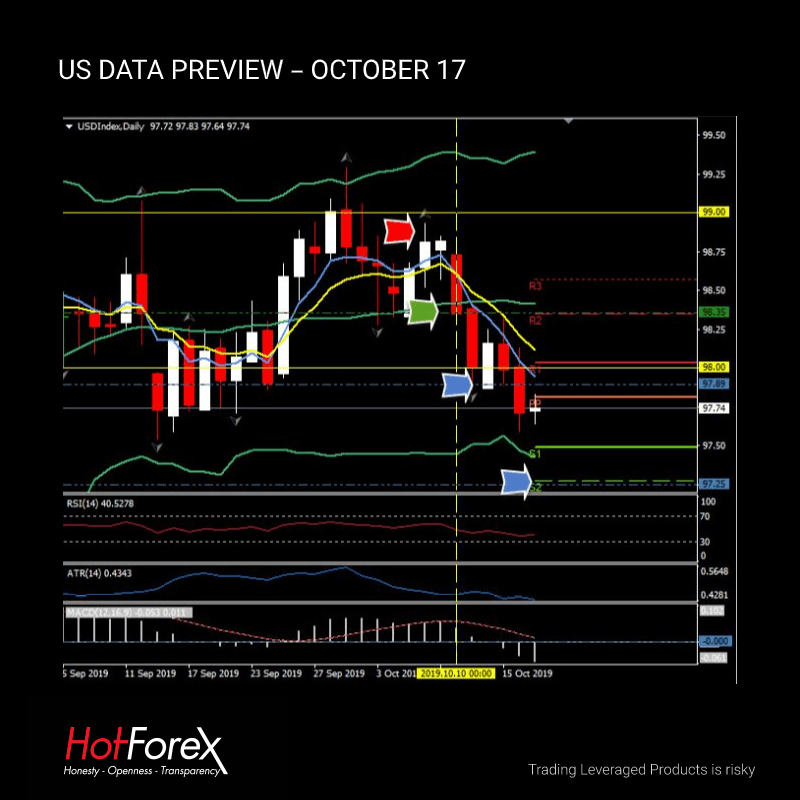

Four of the last five trading days have witnessed Dollar weakness, compounded yesterday by poor Retail Sales numbers, but supported by some strong corporate earnings (Bank of America & Netflix) in particular. So what economic data may move the USD today (save Brexit news for GBP & EUR)?

US Housing Starts & Permits: Starts should drop back to a 1.282 mln pace in September, after a sharp rise to a 1.364 mln clip in August. Permits similarly are expected to slow to 1.370 mln in September, after popping to 1.425 mln in September. Permits have shown a solid growth path into Q3 despite a July starts set-back, and expectations are for Q3 averages of 1.287 mln for starts and 1.371 mln for permits.

US Philly Fed Manufacturing Index: The October Philly Fed index is forecast to fall to 7.0 from 12.0. That’s down a 1-year high of 21.8 in July and a 33-month low of -4.1 in February. The late-September producer sentiment surveys deteriorated significantly after firmness in the early-September reports, and the early-October data will be closely scrutinized to see if this pull-back continued. The “soft data” surveys are at risk of a possible impact from the UAW-GM strike, alongside the ongoing headwind from troubles abroad.

September Industrial Production: Industrial production is projected to be unchanged in September, with a likely hit from 49k striking UAW workers at GM, but with a utility lift from warm weather. We saw a 0.6% August headline reading, with a 0.5% August increase for manufacturing and a 1.4% increase for mining, while utilities grew 0.6%. In September, we expect manufacturing to ease -0.3%, but with gains of 0.1% for mining and 2.0% for utilities. Capacity utilization should fall to 77.7% from 77.9% in August. Industrial production fell at a -2.1% clip in Q2, though we expect a positive 1.8% growth pace in Q3.

US Weekly jobless claims: Initial jobless claims for the week of October 12 are expected to rise to 219k, after decreasing 10k to a lean 210k in the week of October 5. Note the data coincide with the BLS survey week. The increase in claims through the last two weeks of September likely reflected some lift from the September 16 start of the UAW strike at GM that includes 49k workers. Strikers don’t qualify for benefits, but suppliers to GM do. We saw little apparent lift in the first week of October, but our assumption is that claims face upside risk until the strike is settled. We expect claims to average 217k in October after a lean 213k average in September despite the strike. We saw a 212k cycle-low average in July that was also seen last September. We saw prior claims averages of 216k in August, 222k in June, and 217k in May.

Technically, the USDIndex broke below the 20-day moving average last Friday (October 10) and has continued to track lower all week, breaching key support at 98.00 yesterday. Next support at S1 is 97.50 and below that is S2, the 200EMA and T2 from the crossing EMA Strategy at 97.25. RSI (40) and MACD have both also move lower. The Daily pivot and September lows at 97.75 may provide some initial support, a break back over 98.00 would bring in the 20-day moving average again at 98.40.

Author

With over 25 years experience working for a host of globally recognized organisations in the City of London, Stuart Cowell is a passionate advocate of keeping things simple, doing what is probable and understanding how the news, c