US CPI Preview: Lower will get the Fed's attention

- US annual core CPI lower, near Fed target

- Overall inflation expected to drop sharply

- Falling prices undermine the need for Fed rate increases in the second half of the year

The Bureau of Labor Statistics, a division of the Department of Labor will publish its Consumer Price index for January on Wednesday February 13th at 8:30 am EST, 13:30 GMT

Forecast: Ebbing inflation

Core CPI, which excludes food and energy costs, is expected to rise 0.2% in January as it did in December with the annual rate slipping to 2.1% from 2.2%. Overall inflation is predicted to decline 0.1% in January the same as December with annual price changes dropping to 1.6% from 1.9% in December

Inflation and the Federal Reserve

The central bank has retreated from its aggressive rate tightening of last year. The December Projection Materials released after the FOMC meeting reduced the year end Fed Funds rate to 2.9% from 3.1% and thus the prospective 2019 rate increases from three to two. The economic growth assessment for the US was dropped to 2.3% from 2.5%.

The Fed’s caution was not primarily based on the American economy which is in good shape, expanding more than 3% in 2018, with a robust job market and rising wages. Risks came from overseas with the British exit from the EU, the Italian disputes with Brussels, slowing growth on the continent and in the global economy.

It is probable the equity swoon in December played a part in the considerations though the Fed is loath to admit it. One of the worries for equites was whether the central bank’s rate normalization increases would breach the neutral rate and begin to slow the US economy.

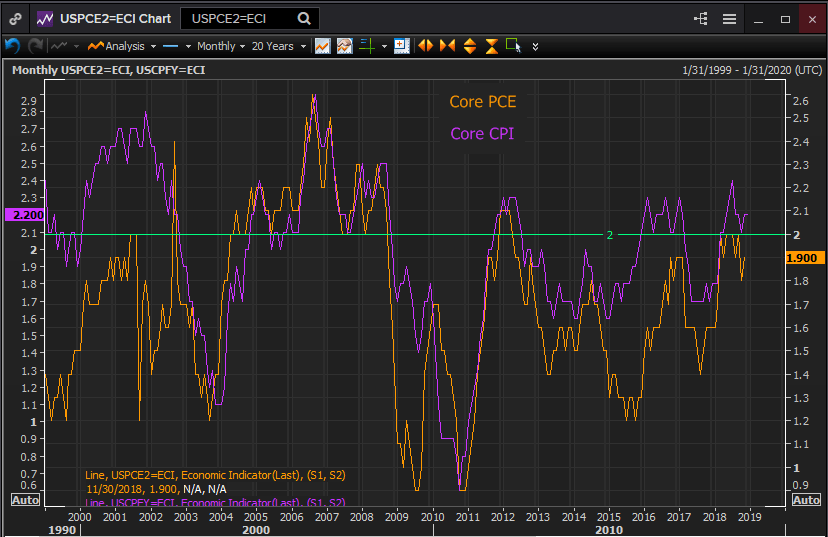

Core PCE versus Core CPI

The estimate for the Fed’s preferred inflation measure, the core personal consumption expenditures price index, core PCE for short, for 2019 was lowered in the Projection Materials to 2.0% from 2.1%. The overall PCE rate was adjusted down to 1.9% from 2.0%.

The oversight and control of inflation is one of the Fed’s two Congressionally mandated economic tasks. Historically the Fed sought to reduce inflation. Since the financial crisis and recession the central bank has sought to foster it. One of the chief aims of the several quantitative easing programs was to bring annual core PCE inflation to the Fed’s 2% target.

Core PCE is a more modern version of CPI. Its different composition results in a lower inflation rate.

Reuters

Prices proved to be less amenable to monetary manipulation in the aftermath of the financial crisis that the Fed governors had hoped. It took more than three years after the QE interventions for core CPI to return to the target rate. The core PCE rate finally reached 2% in middle of 2018, almost a decade after the great collapse in the inflation rate in late 2008 and 2009.

It is problematic whether the return of inflation to the target last year was a delayed function of the monetary largess earlier in the decade or a more basic response of prices to the economic expansion.

Core PCE, CPI and the shutdown

The core PCE rate dropped from 2% in September to 1.8% in October and then bounced back to 1.9% in November. The December and January PCE figures will not be released by the Bureau of Economic Analysis until March 1st.

In lieu of the missing PCE numbers the core CPI figures for January take on greater importance. The expected fall to 2.1% from 2.2% is an indicator of weakening price pressures particularly in light of the July peak at 2.4%. The same decline will be assumed of the PCE numbers.

Inflation, the Fed pause and the dollar

Inflation was not one of the Fed’s stated concerns in the December FOMC statement or the press conference comments of Chairman Powell.

If however, inflation retreats further from the 2% target the Fed’s pause will gain justification and the potential for second half rate hikes will become that much smaller.

The dollar has strengthened marginally since the Fed meeting on December 19th despite the change in rate outlook. The US central bank remains the sole practitioner of rate normalization among the major industrial nations. The US economy is the strongest and its monetary and financial authorities are best situated to help were a serious global slowdown or recession occur. Against that background the dollar will keep its margins even if inflation falls and adds one more click to the Fed's worry beads.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.