US Consumer Price Index June Preview: Has inflation peaked?

- CPI expected at 0.5% in June, from 0.6%, annual at 4.9% from 5%.

- Core CPI forecast to gain 0.5% after 0.7% in May, yearly to 4% from 3.8%.

- Ebbing base effect will uncover shortage driven price gains.

- Markets will attend to CPI but not trade results.

Consumer prices in June are expected to provide the first proof that the recent sharp annual price gains are a temporary phenomenon.

Over the past six months the Consumer Price Index (CPI) has nearly tripled from 1.7% for the year in January to 5% in May. The core rate has gone from 1.4% to 3.8%.

In June, the monthly CPI increase is forecast to drop to 0.5% from 0.6% in May and 0.8% in April. The annual CPI rate is projected to slip to 4.9% from 5% in May. The April monthly increase and the May annual rate were the highest in over a decade.

Core inflation is expected to climb 0.5% in June, down from 0.7% prior and the annual rate is predicted to rise to 4% from 3.8%.

US CPI

Federal Reserve policy

Fed interest rate policy going back to the beginning of the pandemic, has been focused on restoring the job market and has been increasingly, and deliberately divorced from reaction to price increases.

The Federal Reserve began preparing for these unusually price steep increases last September when it adopted inflation averaging as a guide for policy. Under this system prices are permitted to run above target as long as necessary to bring the average into line with the 2% goal. The Fed has not set a period for inflation averaging.

However, even with the steep declines last year, the 12-month average for the annual core CPI rate was 1.84% in May. If the forecast of 4% for June is accurate the 12-month average will be 2.08%.

Lockdown prices and inflation

Last year's March and April lockdowns produced a collapse in consumer prices as households avoided all but essential purchases.That decline in the base index reversed as the economy reopened in the third and fourth quarters of 2020 and prices resumed their normal advances. The plunge in prices was most severe in April, May and June last year. Annual price gains of 0.3%, 0.1% and 0.6% respectively, resulted in the 4.2%, 5% and the expected 4.8% increases 12 months later.

The Fed’s assertion that this year’s exaggerated price gains are the product of the base effect was a mathematical certainty once price advances resumed. That part of the inflation equation has played out exactly as predicted.

This month's expected drop in the headline rate should be followed by further declines in the third and fourth quarters.

Labor and product shortages and inflation

Current inflation in the US is the product of more than base effect from last year’s price collapse.

The lockdowns wrecked havoc with supply chains and raw material production around the world. Almost all manufacturing is an assemblage of parts, material and labor from around the globe. Many of those components are in short supply, particularly the ubiquitous computer chips that are integral to so many consumer items. Shortages have driven consumer and producer prices higher and are not expected to relent until next year.

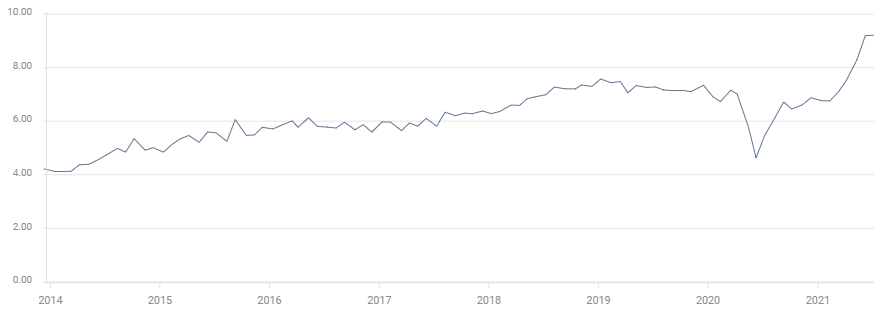

Labor is also in short supply in the US or at least the number of people willing to work is insufficient. The Job Openings and Labor Turnover Survey (JOLTS) had a record 9.2 million open positions in May. Help wanted signs are everywhere.

JOLTS

It is likely that for many lower wage jobs, the additional unemployment benefits enacted by the Biden administration are an incentive to postpone returning to work.

Employers are offering signing bonuses and wage increases to secure workers and these gains will remain once the labor shortage fades.

It is a matter of conjecture what portion of the current CPI rates are due to the base effect and what portion stems from the various shortages created by the economic closures. What is certain is that as the base effect wanes it will uncover higher residual inflation

Conclusion: Market response

The Federal Reserve has been successful over the last several months at reducing market sensitivity to inflation. The effort began with adoption of inflation averaging last September and has continued with the insistence that the current spike is temporary.

June is expected to be the first evidence that the Fed’s analysis is correct.

In a sense the Fed has been answering a question that the markets have never asked. There has never been any doubt that the rapid burst of inflation in the first half of was due primarily to the reversal of last year’s lockdown collapse.

The important and unanswered question is how much inflation has been created by the economic dislocation of the lockdowns? The answer to that query will not be known until the base effect is fully dissipated sometime in the fourth quarter.

Will core CPI return to its 2.3% average of the last quarter of 2019? Will the wage gains forced by labor shortages raise inflation expectations?

Market response to the June and subsequent CPI figures will be restrained until we begin to get an answer to those important questions.

Premium

You have reached your limit of 3 free articles for this month.

Start your subscription and get access to all our original articles.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.