US Conference Board Consumer Confidence May Preview: Can that be the turn? Behind us?

- Confidence forecast to rise from six year low in April.

- Michigan May consumer sentiment bounced from nine year low.

- Jobs losses continue in unemployment claims, total 38.615 million.

- May non-farm payrolls expected to shed 4.25 million jobs, unemployment to 19.8%.

- Rising consumer confidence could point to recovery markets and a stronger dollar.

The most devastating job losses in US history have sidelined almost 25% of the workforce but the speed of the plunge may have generated its own rebound as the second major consumer confidence gauge is set to reverse in May.

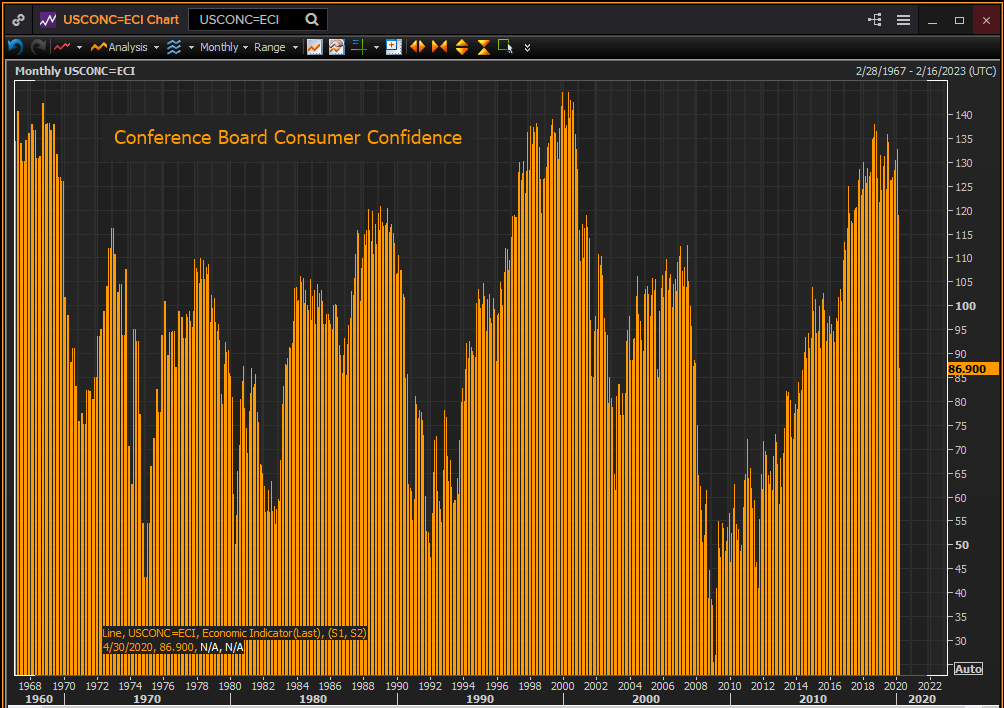

The Conference Board Consumer Confidence index is forecast to climb to 88 this month from 86.9 in April. If correct the May recovery, however slight, would come after April witnessed the steepest one month drop in the 53 year series history.

Reuters

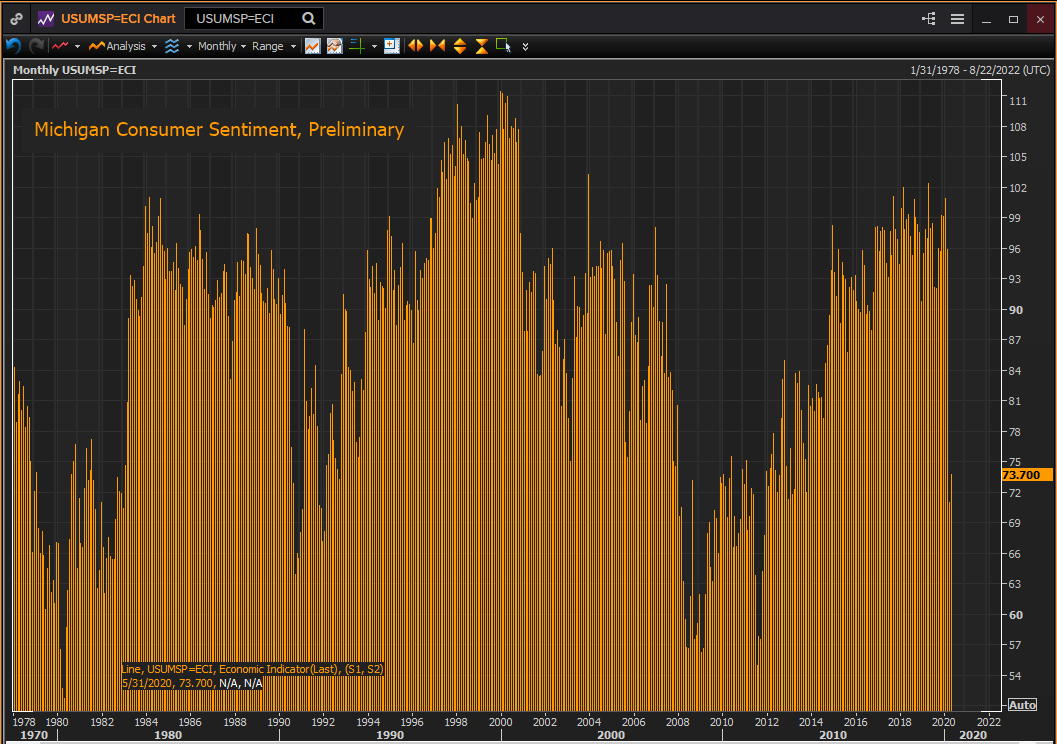

Earlier in the month the Michigan Survey reported that its consumer sentiment index for May came in at to 73.7, better than the 68 forecast and up from 71.8 in April. It is forecast to edge higher to 74 when the final figure is issued on May 29.This measure also saw its largest single month decline from March to April in its 42 year record.

Reuters

US labor market

The collapse of American employment under the business closures and social restrictions of the coronavirus pandemic is a well-rehearsed fact.

Over 38 million people have filed for unemployment insurance in the last nine weeks. Non-farm payrolls shed 20 million workers in April and are expected to drop by another 4.25 million in May. The unemployment rate vaulted from 4.4% in March to 14.7% in April. In the worst years of the Depression it took 13 months for the unemployment rate to rise 10% and the rate is forecast to climb to 19.8% in May.

Consumer spending and GDP

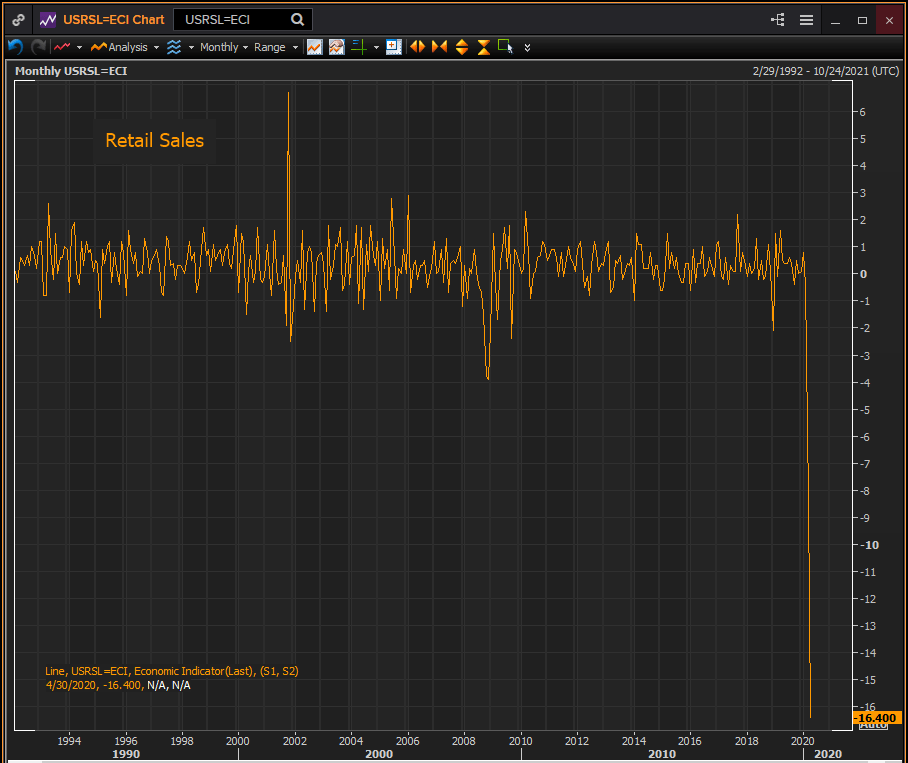

Retail sales tumbled 16.4% in April and 8.3% in March. Practically one-quarter of US consumer spending vanished in two months. Nothing like this has ever occurred before in an industrial economy. The control group category which provides the consumption component of the Bureau of Economic Analysis’ GDP calculation, crumbled 15.3% in April.

Reuters

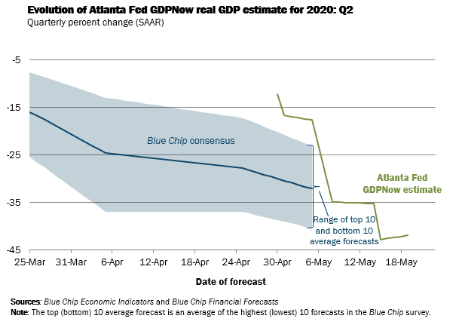

The second quarter growth estimate from the Atlanta Fed’s GDPNow model shows an unheard of 41.9% shrinkage in US economic activity.

Conclusion: Consumers, markets and the dollar

Almost wherever one looks in the statistical record the figures for April were the worst in modern American history and May’s figures are expected to be even grimmer.

Although viral pandemics of varying intensity have occurred repeatedly in the past century, including the deadly Spanish Flu in 1918, no government had ever shut down large sections of its economy as a defense.

The singular circumstances of this economic catastrophe, brought about by fiat, may offer a clue to the nascent turn in consumer sentiment and the future.

Consumers respond differently to normal business cycle recessions than they do to event fomented economic collapses.

In the early 1980s when the Volcker Fed pushed interest rates to nearly 20% to break two decades of inflation and instigated the deepest post-war recession, consumers understood that the precipitating factor was central bank policy. Once it became clear that the rate policy had reversed, consumer sentiment recovered very quickly, even before the economy had resumed strong growth. That optimism and spending helped in no small fashion to accelerate the recovery.

The contrast to the 2008 financial crash and recession is instructive. The cause and remedies in that crisis were far more diffuse and widespread and the structural problems and their remedies much less obvious and immediately successful. Consumer sentiment took more than twice as long to recover to its pre-crash levels than it did from the even deeper drop in Reagan’s first term. One consequence was that the recovery was far slower and prolonged.

Which model will consumers follow as the pandemic and its fears wind down?

Equity markets are clearly placing their bets on the American consumer. Currency markets will shortly follow suit.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.