Week ahead – US NFP and CPI, BoE, ECB and BoJ mark a busy week

- After Fed decision, dollar traders lock gaze on NFP and CPI data.

- Will the BoE deliver a dovish interest rate cut?

- ECB expected to reiterate “good place” mantra.

- Will a BoJ rate hike help the yen recover some of its massive losses?

Less-hawkish-than-expected Fed hurts the Dollar

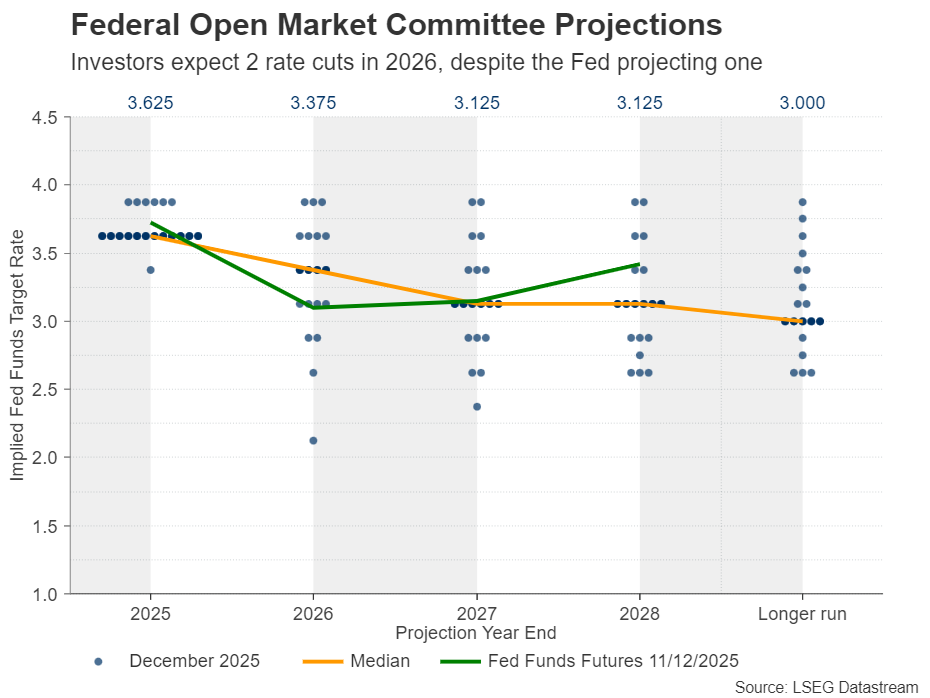

The highly anticipated December Fed decision is behind us, leaving a taste of extreme division among its members, and prompting investors to sell the US dollar. The Committee decided to cut interest rates by 25bps as was widely anticipated, but the updated dot plot pointed to only one single quarter-point reduction for next year.

At first glance this could be characterized as a hawkish cut, especially with two members voting for interest rates to remain on hold, and six officials placing their dot for this year to signal their preference for an unchanged rate.

That said, the dots for 2026 were widely and evenly spread, with four members advocating for no rate cuts in 2026, four favoring one prediction, and four wanting two. So, the median for 2026 did not represent a majority opinion; rather, it was the average of those three equally supported levels.

More importantly, the Committee announced that it will begin purchasing short-term Treasury bills as part of its reserve management operations, with the aim of supporting market liquidity and maintaining control over interest rates.

Combined with a less-hawkish-than-expected press conference by Fed Chair Powell, who highlighted slowing jobs growth and uncertainty about the labor market, this may have been the main reason behind the dollar’s slide, with investors remaining convinced that the Fed may need to cut twice next year.

NFP and CPI inflation to impact Fed rate bets

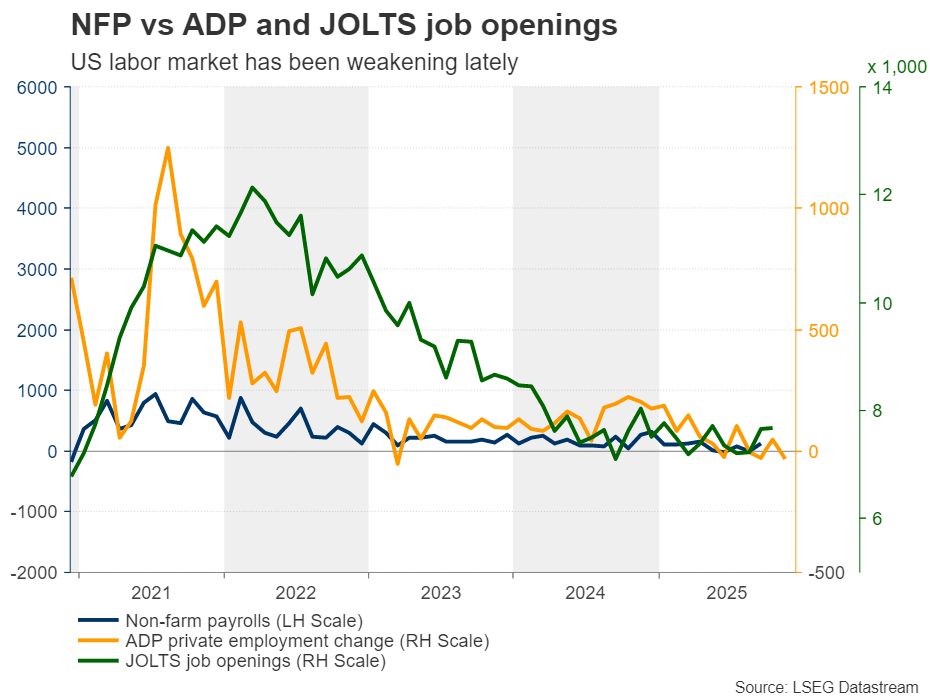

This week, the spotlight is likely to fall on the shutdown-delayed NFP report for November, due out on Tuesday and the CPI numbers for the same month, due out on Thursday. The ADP report for November revealed that the private sector lost 32k jobs, missing analysts’ estimate of a 5k gain, which tilts the risks to the NFP report to the downside.

Even if the CPI data reflects further stickiness in inflation, the Fed seems to be prioritizing the labor market for now, with Powell noting on Wednesday that the current overshooting of the 2% inflation goal is mostly due to tariffs and that it is likely to be a “one-time price increase.” Therefore, the inflation numbers are unlikely to fully reverse any dollar weakness ignited by Tuesday’s NFP report.

The preliminary S&P Global PMIs for December and the retail sales figures for November will also be released on Tuesday and Wednesday, respectively.

BoE to lower rates – Will it signal more cuts for 2026?

Besides the aftermath of the Fed and the key NFP and CPI data out of the US, investors will also have to digest three more central banks this week: The BoE and ECB on Thursday, and the BoJ on Friday.

Getting the ball rolling with the BoE, British policymakers kept rates unchanged in November but via a 5-4 vote, with the 4 dissenters favoring a rate cut and Governor Bailey being the only one of the five who supported the on-hold decision noting that overall inflation risks had moved down. This was probably interpreted as a signal by Bailey that he will join those wanting a rate cut at Thursday’s decision.

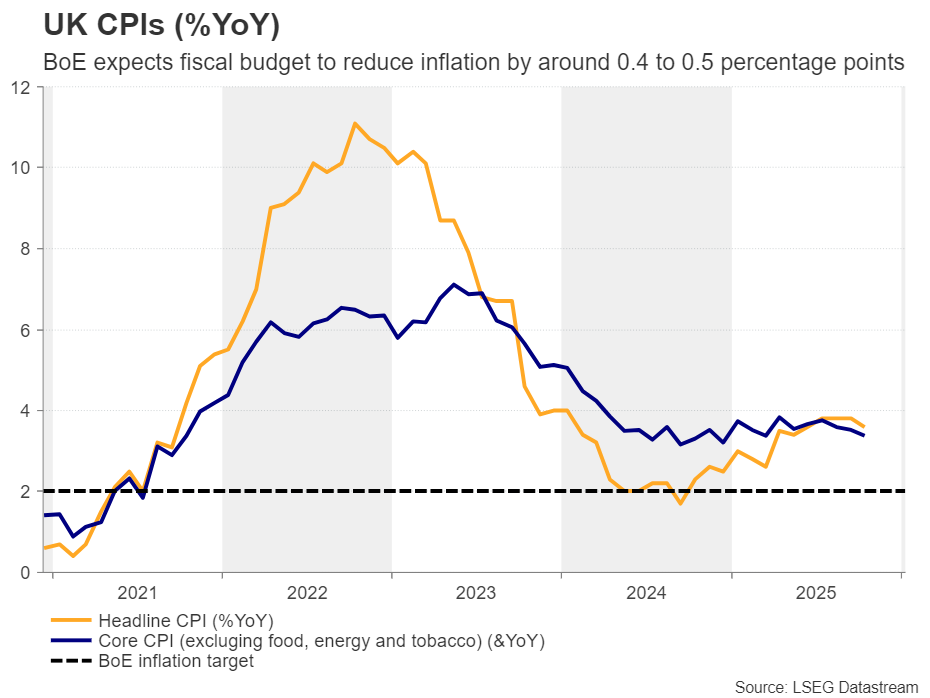

Since the prior meeting, data showed that the unemployment rate for September moved up to 5.0% from 4.8%, economic growth slowed to 0.1% in Q3 from 0.3%, and both the headline and core CPI rates moved slightly lower, although they both remain above 3%.

With all that in mind, investors are now assigning a 90% chance of a rate cut next week, while another quarter-point reduction is more-than-fully priced in by December 2026. It is also worth noting that the Bank of England projected that the latest budget plan announced by finance minister Reeves will reduce the annual inflation rate by around 0.4 to 0.5 percentage points from around the second quarter until the end of 2026.

Thus, a rate cut accompanied by a dovish message could prompt investors to bring forward the timing of the next rate cut and perhaps add some more basis points worth of reductions to their bets for next year. Such an outcome could weigh on the British pound.

Ahead of the decision, a barrage of UK data will be released. The employment report for October and the flash PMIs for December will come out on Tuesday, followed by the CPI and retail sales data on Wednesday and Friday, respectively. A back-to-back slowdown in inflation could solidify the notion of a dovish hold the next day and may trigger a pound slide, even ahead of the BoE decision announcement.

ECB to stay sidelined, upward GDP revisions likely

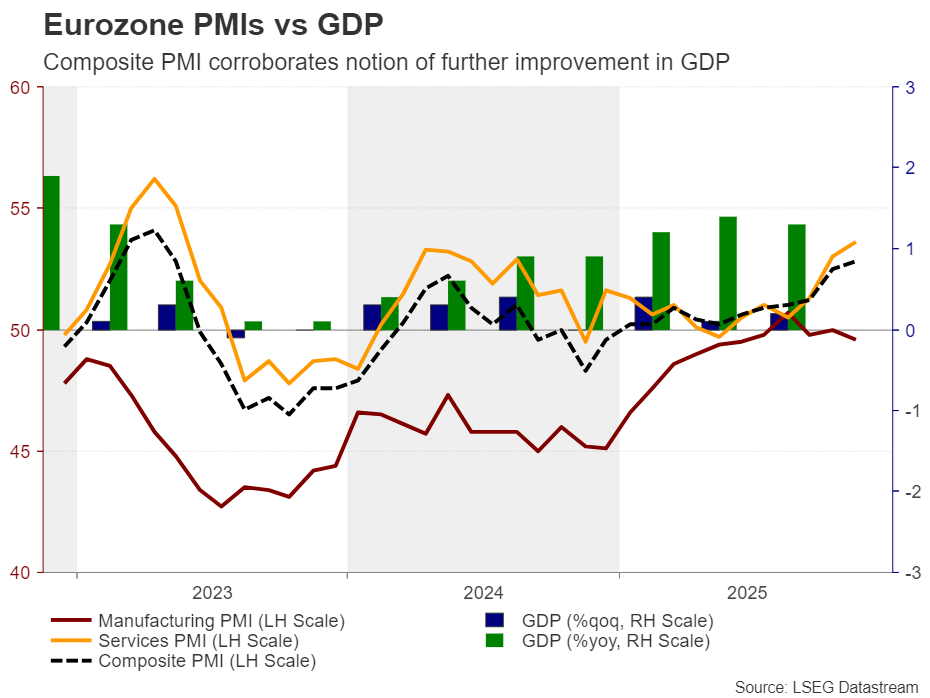

Around an hour or so after the BoE announcement, it will be the ECB’s turn to make its monetary policy decision public. At the prior meeting, ECB policymakers kept interest rates unchanged, reiterating the view that policy was in a “good place” as the economy was showing signs of health and inflation was close to target.

This week, on Wednesday, ECB President Lagarde said that the resilience of the Eurozone economy to trade tensions and its near-potential growth could prompt the Bank to proceed with upwardly revised GDP projections at next week’s gathering. Taking things a little bit further, ECB Board member Isabel Schnabel told Bloomberg News on Monday that the Bank’s next move may be a rate hike, though it will not happen in the near future.

With all that in mind, investors expect the ECB to stand pat next week, and they are factoring in a respectable 36% chance of a rate hike by the end of next year. Therefore, a reiteration of an upbeat message could help Euro/Dollar march higher, especially if the flash S&P Global PMIs on Tuesday corroborate the notion that the Euro area economy is faring well.

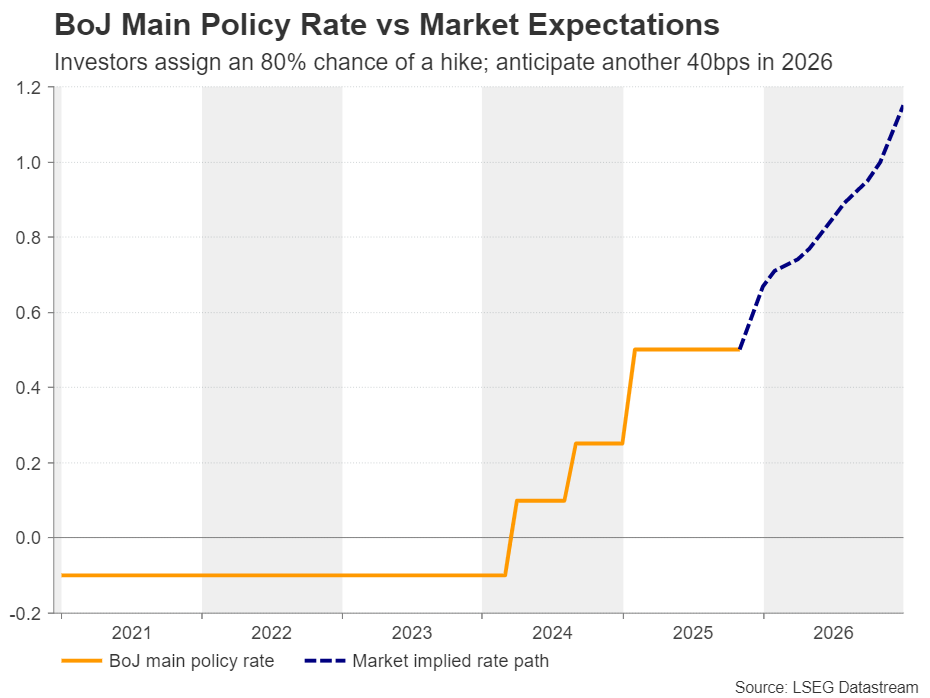

BoJ prepares to raise rates; forward guidance to be scrutinised

Last but not least, the BoJ is now seen raising interest rates with a chance of 75%. As for next year, investors are penciling in another 40 basis points worth of hikes, which translates into another quarter-point reduction and a 60% probability of a third.

Following the election of fiscal dove Sanae Takaichi as Japan’s new Prime Minister, investors scaled back their bets about a potential December hike, but recent remarks by Governor Ueda, as well as reports by Bloomberg and Reuters, revived speculation about action. Yet, the yen failed to massively capitalize on the increasing hawkish expectations.

Therefore, should the Bank press the hike button as largely anticipated, the focus will quickly shift to hints and clues about how the Bank is planning to proceed in 2026. If policymakers fail to match the market’s latest hawkish shift, the yen is likely to resume its prevailing downtrend. However, as dollar/yen moves closer to the psychological zone of 160.00, Finance Minister Katayama may become vocal again in expressing concerns about the yen’s slide and perhaps mention the probability of intervention. All this means that upside risks surrounding the yen are unlikely to vanish, even if the BoJ disappoints market participants on Friday.

Author

Charalampos joined Trading Point in August 2022 as a senior market analyst. He has extensive experience in analyzing financial markets, gained through a decade-long career, with his primary focus being on the currency market.