US Conference Board Consumer Confidence March Preview: Three years vanish in an instant

- Markets focused on the virus effect on consumer attitudes and spending.

- Michigan sentiment shed 11.9 points in March to the lowest since October 2016.

- March CB Survey cutoff date mid-month may have missed the worst impact.

The Conference Board, a private non-profit business group, will release its March Consumer Confidence Index on Tuesday March 31 at 1:00 GMT, 10:00 EST.

Forecast

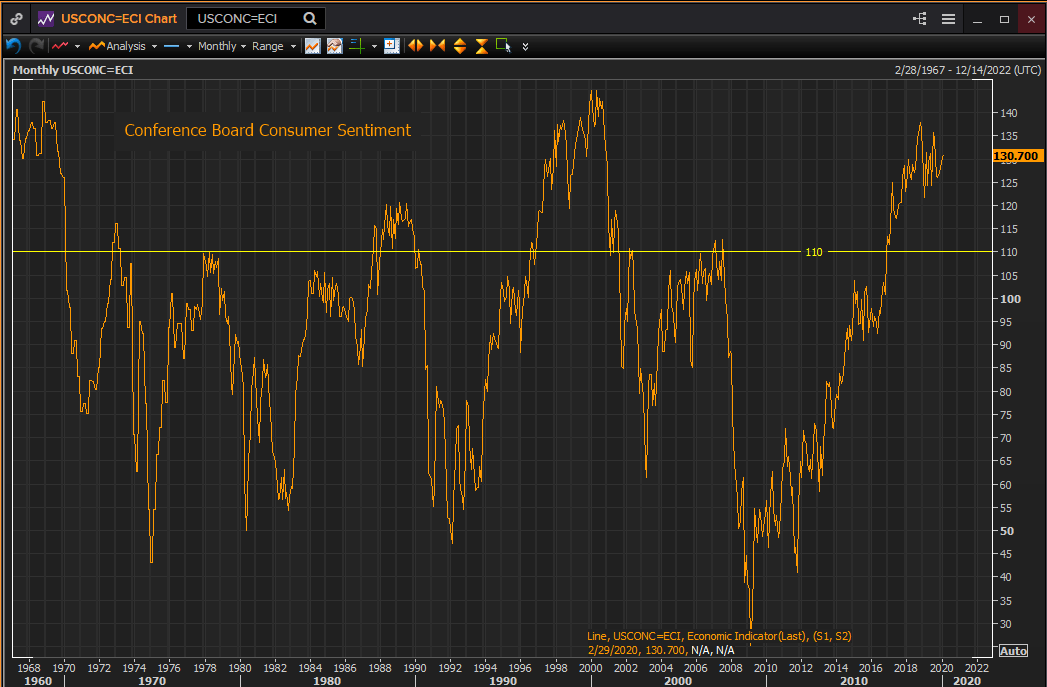

The Conference Board Consumer Confidence Index is expected to fall to 110.00 in March from 130.7 in February. The range of estimates in the Reuters survey 87.4 to 122.0

Conference Board and Michigan consumer scores

The fast accumulating damage to the US labor market from the viral shutdowns has begun to show up in consumer confidence. The Michigan survey for March dropped from its second highest post-recession reading of 101 in February to its lowest since October 2016, the month before the election of Donald Trump to the White House.

There is no reason to assume that the Conference Board accounting will be any different. The consensus estimate for March would bring it down to about the level of November 2016, 109.40.

That the Conference Board gauge would remain above almost all reading for the past two decades except those after the 2016 election and the Michigan survey above almost all post-financial crisis scores is small comfort when these are essentially preliminary reading on the virus impact.

US labor market

In the long history of US labor statistics there has been no comparable economic situation to the torrent of layoffs of the last two weeks. In less than a month initial jobless claims have gone from 211,000 to 283,000 to 3.283 million and they are expected to be three million again this Thursday. In comparison the previous high was 695,000 in October 1982. Even correcting for the 41% growth in population the theoretical 980,000 would still be less than one-third of last week’s total.

The stellar achievements of the last three years in jobs, wages and unemployment will not matter in the least if large numbers of furloughed workers cannot be restored to productive work.

Conclusion: Consumer sentiment

American consumer sentiment has responded effusively to the job market of the last three years rising to levels not seen in two decades and among the best periods in history. Over the past two years consumption, supported by job market optimism, has supported US GDP as business investment shrank to nothing paralyzed by the US-China trade war.

Much will now depend on whether consumers believe that the burgeoning job losses are permanent.

In this consideration they have very little informed opinion to consult. Economists do not know, their predictions are dire but essentially guesswork and their models have difficulty taking into account the powerful desires and needs of business owners to reconstitute their enterprises.

Consumers, especially the vast majority who remain employed, can be expected to pull back sharply on spending in the next few weeks. If nothing else their isolation will obviate a whole range of normal incidental and discretionary expenditures.

It is the period immediately following the shutdowns that will be crucial. Many small business will be on life-support and in need of cash flow. If people resume and are permitted to resume their normal lives then the possibility for a rapid return is greatly enhanced.

In this Americans’ natural optimism may be more accurate than the economic gloom of the professionals. The drive for a normal life is probably the economy’s strongest ally.

Author

Joseph Trevisani

FXStreet

Joseph Trevisani began his thirty-year career in the financial markets at Credit Suisse in New York and Singapore where he worked for 12 years as an interbank currency trader and trading desk manager.