United States: The Federal Reserve, inflation data and markets

The data dependent nature of monetary policy has intensified the mutual influence between economic data, financial markets and central banks. Inflation releases play a dominant role given that central banks pursue an inflation target. In the United States, when CPI numbers are published, the change in the financial futures contracts on the federal funds rate has the highest correlation with the monthly change in core inflation. Going forward, Fed watching will consist of monitoring the inflation surprises -the difference between the published number and the consensus forecast- as well as the ensuing market reaction. Is the latter abnormally strong -like in early 2023- or in line with expectations? This will allow to gauge whether investors are still predominantly concerned about inflation or whether their focus is shifting to the employment data.

Major central banks have repeatedly insisted that future monetary policy decisions will be data dependent. They want to avoid easing too early or hiking rates too much. This stance is understandable considering the uncertainties about monetary transmission -how much of the effect of past tightening still needs to manifest itself, the question about the ‘last mile’ of disinflation will it be more difficult than the early part of the ‘race’-, the gradual improvement of survey data in the Eurozone and US growth that continues at a healthy pace. As a consequence, the mutual influence between data, financial markets and central banks has intensified. More than ever, everybody is scrutinizing data, and the market reaction, through its influence on interest rates, can impact the subsequent releases as well. Unsurprisingly, in this triangular relationship, inflation plays a dominant role given that central banks pursue an inflation target. News about inflation influences the pricing of fixed income and other instruments through the expected impact on future policy rates, on the growth outlook and investor risk appetite.

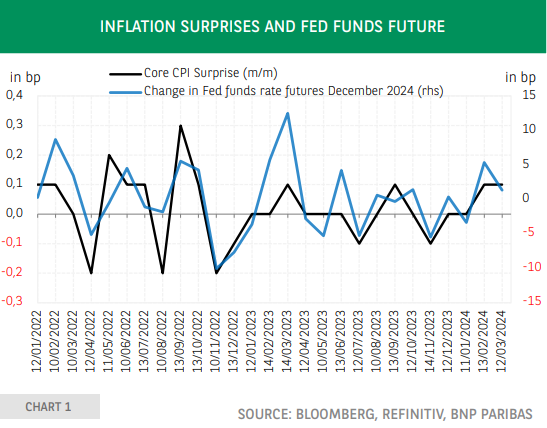

In the United States, several inflation data are published on a monthly or quarterly basis and their market impact depends on the timeliness of the data. The monthly core PCE numbers are published later in the month, after the CPI data have already been published. The latter are an input for the forecasts of the former and therefore data surprises -the difference between the published number and the consensus forecast- tend to be very small and often zero for the core PCE. Interestingly although the core PCE is the preferred inflation measure of the Federal Open Market Committee, the market reaction is larger for the consumer price data because they are published earlier. Consensus data are available for month-on-month and year-on-year headline and core inflation. This allows to calculate the inflation surprise -i.e. the difference between the actual number and the consensus forecast- and to see how it influences expectations of future monetary policy as reflected in the financial futures contracts on the federal funds rate. The table shows the results of a regression of the change -on the release day of CPI inflation data- in the federal funds future expiring in December 2024 as a function of the inflation surprise.

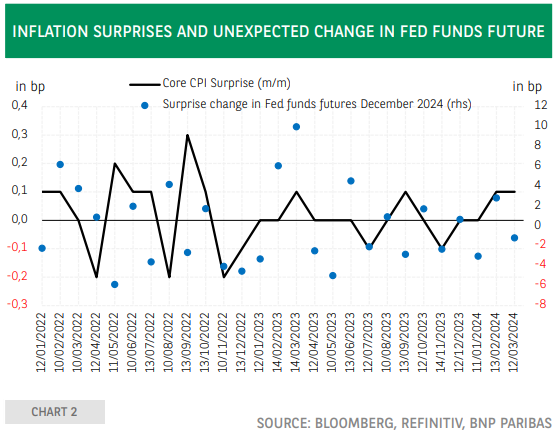

All four inflation measures are statistically significant but the monthly change in the core CPI is clearly superior. Its close correlation with the change in the Fed Funds future rate is illustrated in chart 1. The regressions mentioned in the table allow us to estimate the change in the federal funds rate future for a given inflation surprise and to calculate the difference with the observed change. We call this regression residual the unexpected change in the fed funds future rate. These results are shown in chart 2. Three phases can be distinguished. Firstly, in 2022, the unexpected changes both positive and negative- in the federal funds future rate were rather significant, possibly reflecting a period of heightened complexity in assessing the outlook for monetary policy considering that inflation was very high, and that the policy rate was still very low. Secondly, the inflation releases of February inflation as expected- and March 2023 -inflation 10 basis points higher than anticipated- saw unexpectedly large increases in the federal funds future rate. Thirdly, as of the second half of 2023, the market reaction was much more in line with expectations (rather small regression residuals). Changes in market pricing, including under- or overreactions, may be related to the level of the policy rate and the signals given by the Federal Reserve about its future evolution. The latter refer to the ‘dot plot’, the FOMC members’ projections for the federal funds rate.

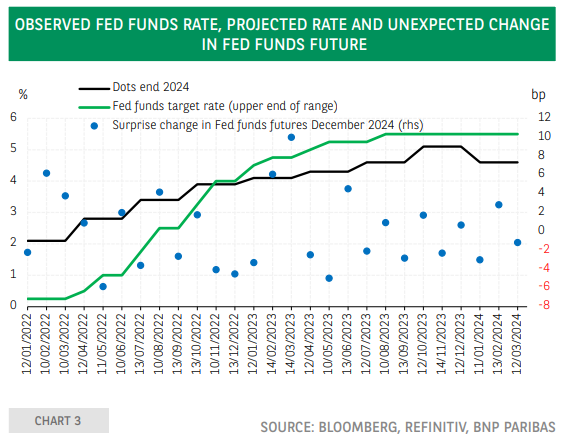

In chart 3, the projection for the end of 2024 has been used. Towards the end of 2022, the federal funds rate moved above the ‘dot plot’, implying that the FOMC members were anticipating a future policy easing. The heightened sensitivity of financial markets to inflation data early on in 2023 may reflect a discomfort about this message and hence concerns about premature easing. Subsequently, the additional rate hikes and the upward revisions of the ‘dot plot’ have probable assuaged these worries, leading to financial market reactions on the occasion of inflation data releases that were more in line with expectations. Going forward, Fed watching will consist of monitoring the inflation dynamics and surprises as well as the unexpected change in the federal funds future rate in reaction to these releases. This will allow to gauge whether investors are still predominantly concerned about inflation or whether their focus is shifting to the employment data, keeping in mind that the Federal Reserve has a dual mandate.

Author

BNP Paribas Team

BNP Paribas

BNP Paribas Economic Research Department is a worldwide function, part of Corporate and Investment Banking, at the service of both the Bank and its customers.