Australian Dollar Price Forecast: Some consolidation in the offing?

- AUD/USD recedes from earlier tops past the 0.7100 barrier on Monday.

- The US Dollar remains on the defensive as traders assess the SCOTUS ruling.

- Next of note in Oz will be the inflation data on February 25.

AUD/USD has been struggling for direction again in the last few days, after reaching new highs of approximately 0.7150 earlier this month. In the meanwhile, the Reserve Bank of Australia's (RBA) hawkish posture, high inflation, and strong domestic fundamentals all support the optimistic outlook for the Aussie Dollar (AUD).

The Australian Dollar (AUD) has started the week without strong conviction. After briefly pushing beyond 0.7100 and printing fresh multi-day highs on Monday, AUD/USD has eased back slightly, drifting under mild selling pressure.

What makes that hesitation interesting is the backdrop. The US Dollar (USD) remains broadly soft, particularly after the Supreme

Court ruling against President Trump’s global tariffs last Friday, which took some policy premium out of the Greenback. And yet, the Aussie has not fully capitalised.

That tells you something. This is not a momentum chase. It feels measured.

Australia: cooling, but not cracking

Australia’s economic growth is moderating, yes. But it looks controlled rather than chaotic. This is not an economy losing its footing. It is one easing off the accelerator after running a little hot.

The February flash Purchasing Managers’ Index (PMI) surveys fit that narrative neatly. Manufacturing at 52.0 and Services at 52.2 remain in expansion territory. Not booming, but comfortably positive.

Retail spending is holding together, the trade surplus widened to A$3.373 billion at the end of 2025, and the Gross Domestic Product (GDP) expanded 0.4% QoQ in Q3, lifting annual growth to 2.1%. That is broadly in line with what the Reserve Bank of Australia (RBA) had projected.

The labour market remains steady rather than spectacular after the Employment Change rose by 17.8K in January, slightly below forecasts, while the Unemployment Rate held at 4.1%. That is consistent with a gradual cooling, not stress.

Inflation is where the real tension sits.

Inflation tracked by the Consumer Price Index (CPI) rose 3.8% YoY in December. The Trimmed Mean printed at 3.3% YoY and 3.4% QoQ in Q4, still above the midpoint of the RBA’s 2% to 3% target band. More strikingly, the Melbourne Institute’s Consumer Inflation Expectations survey jumped to 5.0% in February, the highest since August 2023. That is not a number policymakers ignore.

Credit growth reinforces the idea that policy is restrictive but not suffocating, as Home Loans rose 10.6% QoQ in Q4 and Investment Lending increased 7.9%, suggesting that financial conditions are tight enough to cool demand but not tight enough to stall it.

China: stabiliser, not accelerator

China continues to act as a steady anchor for the Australian currency, though it is hardly providing rocket fuel.

The economy expanded 4.5% YoY in Q4 and 1.2% QoQ as per the latest GDP prints, while Retail Sales rose 0.9% YoY in December. Respectable, but not transformative.

The January PMI split is telling: the official Manufacturing and Non-Manufacturing dipped into contraction at 49.3 and 49.4, respectively. Meanwhile, Caixin Manufacturing and Services remained above the expansion threshold at 50.3 and 52.3, respectively. Larger state-linked sectors appear softer, smaller private firms somewhat more resilient.

The trade surplus surged to $114.1 billion in December, yet inflation remains subdued, as the CPI rose just 0.2% YoY and Producer Prices fell 1.4% YoY. That is not reflation. It is lingering disinflation.

On the policy side, the People’s Bank of China (PBoC) kept the one year and five year Loan Prime Rate (LPR) unchanged at 3.00% and 3.50%, respectively. The message is calm and supportive rather than aggressive. Stability over stimulus. Markets expect more of the same at Tuesday’s meeting.

For the Aussie, that means China is not a headwind, but it is not providing ignition either.

RBA: restrictive, not reckless

Earlier this month, the RBA lifted the Official Cash Rate (OCR) to 3.85%, making it clear that inflation remains the priority.

Updated projections show price pressures staying above target for much of the forecast horizon. The Minutes were explicit. Without the latest hike, inflation would likely have remained above target for too long. Policymakers judged that risks had shifted enough to justify tightening.

But this is not an autopilot cycle. There is no pre-commitment. The path forward is data dependent.

Markets are pricing just over 37 basis points of additional tightening this year. Not aggressive, but enough to keep a yield floor under the Australian Dollar.

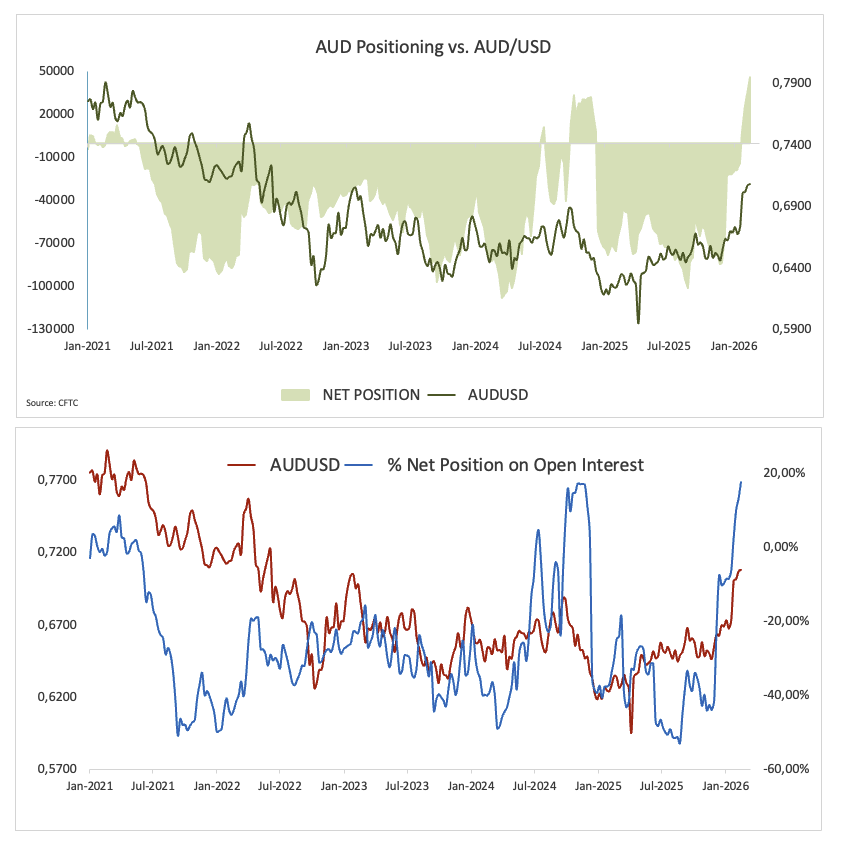

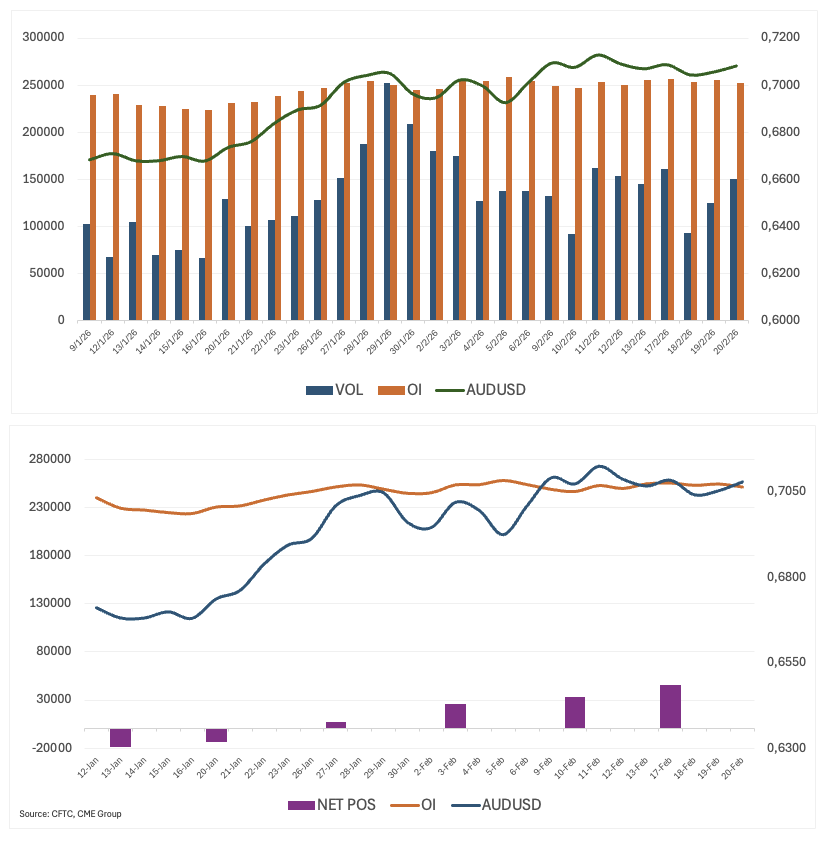

Positioning: rebuilding, quietly

Commodity Futures Trading Commission (CFTC) data show non-commercial traders lifted net longs to nearly 46K contracts, the strongest since late October 2017.

This does not look like froth. It looks like investors are quietly rebuilding exposure.

Furthermore, open interest increased to around 256.2K contracts, suggesting improving conviction without crowding. There is still room if sentiment continues to firm.

Investors are dipping their toes back into the Aussie, cautiously but deliberately.

What matters now

Near term: the US Dollar still dictates the tempo. Strong US data, renewed tariff rhetoric or geopolitical noise can quickly shift AUD/USD. At home, upcoming inflation figures will be key. If price pressures remain sticky, markets may need to reassess the extent of further RBA tightening.

Risks: the Aussie is a high beta currency. If global risk appetite deteriorates, if China wobbles again, or if the Greenback stages a meaningful rebound, the unwind could be swift.

Technical landscape

In the daily chart, AUD/USD trades at 0.7070. The 55-day Simple Moving Average (SMA) rises above the 100- and 200-day SMAs, reinforcing buyers’ control. The longer SMAs also slope higher, and the pair holds above them. The 55-day SMA stands at 0.6825, offering nearby dynamic support. The Relative Strength Index (RSI) at 61.68 remains above the midline, supporting bullish momentum.

Measured from the 0.6421 low to the 0.7147 high, the 23.6% retracement at 0.6976 offers initial support, while the 38.2% retracement at 0.6870 underpins the pullback area. Immediate resistance aligns at 0.7158, followed by 0.7283. A breakout above the first level could extend the advance toward the second, while a close beneath initial support would risk a deeper correction into the pullback zone.

(The technical analysis of this story was written with the help of an AI tool.)

Bottom line: constructive, but not complacent

Australia’s macro backdrop remains resilient. The RBA is restrictive. Positioning is improving. China is stable enough.

That keeps the broader bias tilted to the upside.

But this is not a defensive currency. It performs best when global sentiment is constructive and struggles when risk turns sour. For now, dips are likely to attract buyers as long as the US Dollar remains contained.

If that changes, so does the narrative.

Australian Dollar FAQs

One of the most significant factors for the Australian Dollar (AUD) is the level of interest rates set by the Reserve Bank of Australia (RBA). Because Australia is a resource-rich country another key driver is the price of its biggest export, Iron Ore. The health of the Chinese economy, its largest trading partner, is a factor, as well as inflation in Australia, its growth rate and Trade Balance. Market sentiment – whether investors are taking on more risky assets (risk-on) or seeking safe-havens (risk-off) – is also a factor, with risk-on positive for AUD.

The Reserve Bank of Australia (RBA) influences the Australian Dollar (AUD) by setting the level of interest rates that Australian banks can lend to each other. This influences the level of interest rates in the economy as a whole. The main goal of the RBA is to maintain a stable inflation rate of 2-3% by adjusting interest rates up or down. Relatively high interest rates compared to other major central banks support the AUD, and the opposite for relatively low. The RBA can also use quantitative easing and tightening to influence credit conditions, with the former AUD-negative and the latter AUD-positive.

China is Australia’s largest trading partner so the health of the Chinese economy is a major influence on the value of the Australian Dollar (AUD). When the Chinese economy is doing well it purchases more raw materials, goods and services from Australia, lifting demand for the AUD, and pushing up its value. The opposite is the case when the Chinese economy is not growing as fast as expected. Positive or negative surprises in Chinese growth data, therefore, often have a direct impact on the Australian Dollar and its pairs.

Iron Ore is Australia’s largest export, accounting for $118 billion a year according to data from 2021, with China as its primary destination. The price of Iron Ore, therefore, can be a driver of the Australian Dollar. Generally, if the price of Iron Ore rises, AUD also goes up, as aggregate demand for the currency increases. The opposite is the case if the price of Iron Ore falls. Higher Iron Ore prices also tend to result in a greater likelihood of a positive Trade Balance for Australia, which is also positive of the AUD.

The Trade Balance, which is the difference between what a country earns from its exports versus what it pays for its imports, is another factor that can influence the value of the Australian Dollar. If Australia produces highly sought after exports, then its currency will gain in value purely from the surplus demand created from foreign buyers seeking to purchase its exports versus what it spends to purchase imports. Therefore, a positive net Trade Balance strengthens the AUD, with the opposite effect if the Trade Balance is negative.

Author

Pablo Piovano

FXStreet

Born and bred in Argentina, Pablo has been carrying on with his passion for FX markets and trading since his first college years.