UK jobs market proves resilient in the face of employer tax rises

There's no shortage of surveys pointing to weaker hiring intentions in the face of next month's employer tax hikes. But for now, at least, the official data shows little sign of that translating into lower employment or higher redundancies.

The mood music surrounding the UK jobs market isn’t good. Survey after survey has pointed to weaker hiring appetite and in some cases, layoffs, ahead of a sharp rise in employer taxation next month.

But so far, that doesn’t seem to be having any material impact on the official data we’re getting on the labour market. Private sector employment is more-or-less flat, having gently fallen through 2024, if we look at the payroll-based numbers and exclude government-heavy sectors. Vacancy levels have flattened out too around pre-Covid levels, and that goes for sectors that you’d expect to be more sensitive to the tax hikes (hospitality and retail).

Redundancies similarly show little sign of change. Employers are required to notify the government if they are laying off more than 20 staff members at any given site, via a HR1 form. These notifications haven’t discernibly increased over recent weeks.

This picture could of course change, not least because neither the tax hike nor the near-7% rise in the National Living Wage have kicked in yet. But thinking about the Bank of England decision later today, there’s no clear impetus here for a greater number of officials to back a faster pace of rate cuts.

Back in February, Catherine Mann now-famously switched from the arch-hawk to arch-dove, suddenly favouring a more aggressive 50bp rate cut. She is likely to go against the committee again today and vote for another rate cut. At the time, she highlighted the risk of “non-linear” falls in employment as her catalyst for action. While she could still be proven right on that, for now, the data doesn’t appear to back up that line of thinking.

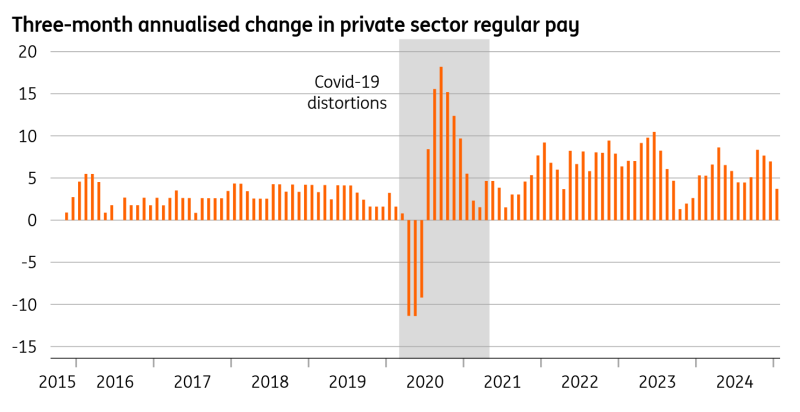

Private sector pay growth appears to be slowing

Source: Macrobond, ING calculations

While other officials might not join Mann’s camp just yet, there are still good reasons to expect the Bank to keep cutting rates once per quarter throughout this year and into 2026. Elevated wage growth is among the most commonly cited reasons at the Bank for its recent caution. But momentum appears to have slowed; the latest three-month annualised change in private sector pay slowed to 3.7% in January. That suggests the year-on-year rate, currently just above 6%, should start to fall back over the coming months.

If that happens, and services inflation also proves more benign than the BoE expects, we think that should see officials cut rates further than markets are currently pricing into 2026. We expect a terminal rate of 3.25%, versus market pricing of roughly 3.90%.

Read the original analysis: UK jobs market proves resilient in the face of employer tax rises

Author

ING Global Economics Team

ING Economic and Financial Analysis

From Trump to trade, FX to Brexit, ING’s global economists have it covered. Go to ING.com/THINK to stay a step ahead.