UK growth disappoints despite cautious reopening in some sectors

Despite the reopening of construction and manufacturing, the UK's May GDP figures were underwhelming to say the least. Admittedly this is 'old news' now, and we should see a sharper rebound in June and July. But it does serve as a reminder that economic recovery from Covid-19 is going to be very protracted

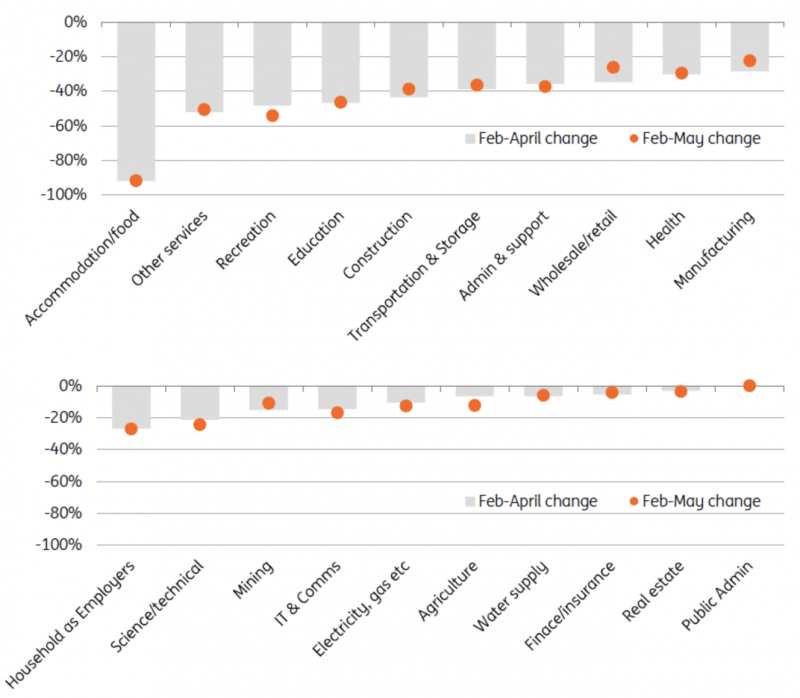

There's little doubt that the latest UK GDP figures for May are underwhelming. Output rebounded by a mere 1.8%, having shrunk by 25% during March and April.

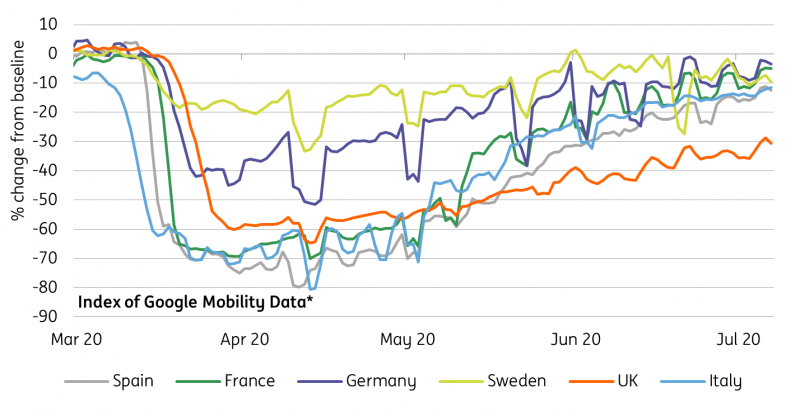

It's true though that the pick-up was never going to be spectacular, given that unlike some other European countries, the majority of the restrictions remained in place through May. Google's Mobility Index - which up until now has been a reasonable proxy for activity in this crisis - had only pointed to a rebound in activity in the region of 4%.

Like other economists however, we had thought that the reopening of construction and manufacturing might have contributed to a slightly sharper rebound. In the event, 30% of construction firms were still not operating in May, according to these latest figures.

Most sectors barely recovered from April's low

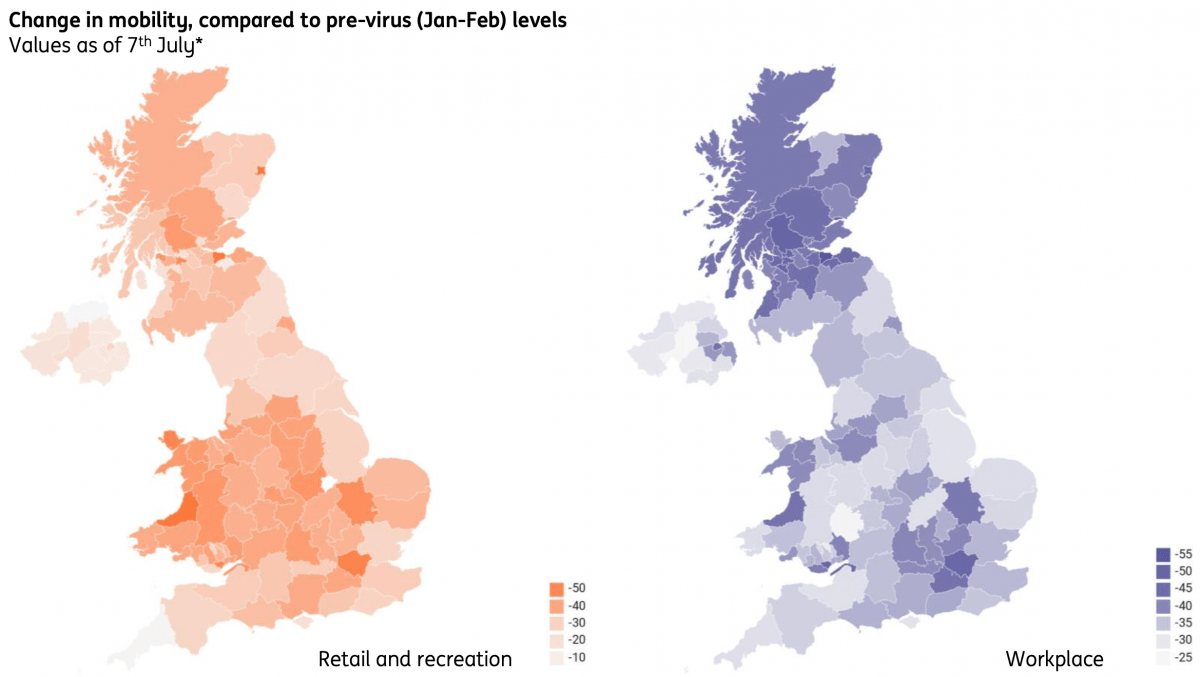

Of course, a lot has changed since then. The reopening of retail during June should have contributed to a sharper rise in output, and we suspect there will be some evidence of pent-up demand in forthcoming figures. According to Google's data, trips to retail/recreation have recovered to some degree in parts of England, outside of the major cities.

But with overall footfall numbers still well down on last year, we should be cautious in assuming that any rebound in retail activity will prove to be fully sustainable.

We suspect that when we get the June GDP figures, the economy will still have been around 20% smaller at the end of the second quarter than it was pre-virus. And while we should see some further recovery through the summer as more industries are allowed to open, it's clear that the economy is going to continue operating well below pre-virus levels for some time - probably a couple of years at the minimum.

There are mounting concerns about unemployment, as firms begin to make adjustments to their operations reflecting ongoing social distancing constraints and lower demand. That, combined with the ever-present risk of more-widespread local lockdowns, as well as the significant changes in UK-EU trade terms next year, all pose significant risks during the Covid-19 recovery phase.

The UK has been slower to getting moving again than other parts of Europe

Mobility index is an average of Retail and Recreation, Grocery and Pharmacy, and Workplaces, from Google's Mobility Report. Baseline is the median value for the corresponding day of the week between 3 Jan-5 Feb. Figures are a three-day moving-average

Retail/recreation trips have been slower to recover in major cities and Wales/Scotland

Read the original article: UK growth disappoints despite cautious reopening in some sectors

Author

James Smith

ING Economic and Financial Analysis

James is a Developed Market economist, with primary responsibility for coverage of the UK economy and the Bank of England. As part of the wider team in London, he also spends time looking at the US economy, the Fed, Brexit and Trump's policies.